- Move aims to stop low-priced competition

- Sectors with over-capacity may output cuts

Madhumita Mookerji

Chinese steel prices, spot and futures, have been rising for some now, on expectations of supply-side reforms. The much-awaited proposals were formalised and unveiled on 1 July, 2025, which mainly pivoted around an “anti-involution” movement that had a direct bearing on the steel sector, along with others like cement, photovoltaics etc.

What is the anti-involution movement?

On 1 July, an important meeting was held where the top leadership set the tone, of “rectifying low-price disorderly competition, promoting orderly withdrawal of backward production capacity and other requirements…”

Briefly, it indicates, the Chinese government does not want its steel industry to compete so fiercely that all players end up losing money. This means, mills will need to curb output and limit exports of raw materials such as billets, which, if exported, will only leave pollution and voluminous steel-making capacity inside China without getting added value from the products.

Thus, from 2 July itself, many industries nursing over-capacities, including steel and coking coal, saw significant position-building and surging prices.

In fact, anti-involution has become the watchword of Chinese industries at present and, recently, the China Iron & Steel Association (CISA) called for strengthening self-discipline to prevent “involutionary” vicious competition – read cut-throat price reductions. Simultaneously, CISA proposed research and promotion of prudent capacity management, improving economic efficiency and effectively achieving quality development.

In fact, anti-involution has become a consensus of the entire industry of late. Starting from 1 July, China’s BYD Auto in a bid to stop the price war, halted price reductions. Earlier, in expectation of such reforms, from around the second week of June, nearly 20 automobile companies, including BYD, FAW, GAC, NIO, Xiaomi, etc publicly promised to unify the payment period to within 60 days, which was regarded by the market as the first step of the auto companies towards an “anti-involution” compliance.

Steel production cuts in offing?

With the onset of anti-involution, many feel that industries saddled with over-capacity will soon effect production cuts similar in scale to that seen in 2015.

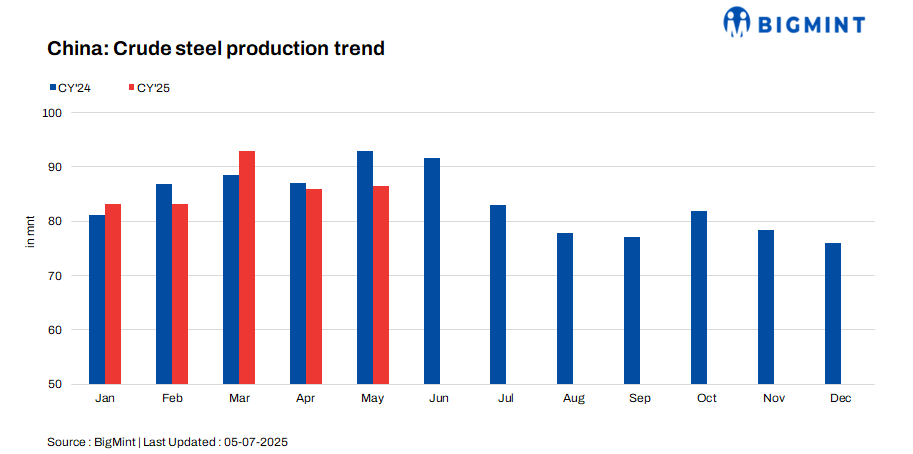

It may be recalled China’s crude steel production in May 2025 touched 86.55 million tonnes (mnt), an almost 7% y-o-y decline but a marginal 1% increase m-o-m compared to April 2025 while output over January-May, 2025 fell 1.7% y-o-y to 432 mnt.

There have been rumours that Tangshan’s sintering machine production could be cut by 30% over 4-15 July. About half of the mills reportedly said they had received the notice while the remaining 50% said the probability of their having received the notice was high. Mysteel sintering ore data on 25 June showed that if the production restriction policy is implemented as planned, mills’ capacity utilisation may drop to 70% and the daily output of sintering ore may decrease by 30,000 t.

It is also being said that till the 3 September military parade, steel mills in the Beijing-Tianjin-Hebei and surrounding regions may witness frequent environment-related production cut diktats.

Price trends

Data available with BigMint shows that hot rolled coils futures on the Shanghai Futures Exchange rose over 2% to RMB 3,145/tonne ($439/t) on 23 June against RMB 3,076/t ($429/t) on 3 June while rebar had also shown an upward trend, rising 2% to RMB 3,021/t ($422/t) from RMB 2,961/t ($413/t) on 2 June.

HRC prices, exw Tianjin, showed an uptrend from 23 June’s RMB 3,064/t ($428/t) to RMB 3,070/t ($429/t) on 30 June while CRCs remained flat at RMB 3,796/t ($530/t). Billets, ex-Tangshan, rose to RMB 2,928/t ($409/t) from RMB 2,914/t ($407/t) in this period.

Tangshan HRC prices, although they have fluctuated fairly steeply over the last one month, have not slipped below RMB 3,230/t ($451/t), touching a high of RMB 3,270/t ($457/t).

Outlook

The next focus of the market will be on whether the optimistic expectations sparked by the new movement will lead to a sustained upward movement in futures and spot markets.

Compared to previous months, supply-side disruptions have significantly increased. Thus, even after the speculative hype around the anti-involution movement dies down, prices are unlikely to experience a smooth uptrend because the on-ground demand scenario is weak whereas expectations are strong in terms of firming up of prices. Thus, sustained implementation of such reforms will be challenging.

“Many industries in China have reached a consensus that prices should not be so low. They want healthy competition. But, I doubt this trend can sustain,” a source from China told BigMint, especially since new home prices dipped 0.2% m-o-m in May, extending a two-year stagnation while the construction industry’s Purchasing Managers’ Index (PMI) for May stood at 51.0%, which indicated a slight decrease from April’s.

Leave a Reply