China’s iron ore market will witness a supply surplus this year as ore supply is seen growing overall while demand among steelmakers is likely to soften, according to Mysteel’s newly published report on iron ore market trends for 2023.

Domestic iron ore supply including both output from local mines and imports is forecast to increase by 23 million tonnes on year to reach 1.41 billion tonnes in 2023, while this year’s total demand will reach 1.39 billion tonnes, lower by 3.6 million tonnes from the estimate for 2022, the report suggests. This will result in an ore surplus of about 22.98 million tonnes, Mysteel predicts, more that reversing the supply-demand last year that showed a deficit of 3.6 million tonnes.

In terms of global supply for 2023, three out of the world’s four top iron ore miners expect to produce more ore this year and so contribute to the increase in ore supply worldwide, according to the report.

Specifically, iron ore production at Vale may reach around 315 million tonnes this year with an on-year rise of 5 million tonnes, Mysteel estimated, based on the Brazilian miner’s production target for 2023.

In addition, Rio Tinto will produce about 323 million tonnes of iron ore this year, rising by some 3 million tonnes on year thanks to the further ramp-up of its Gudai-Darri and Mesa A Wet Plant projects in Western Australia’s Pilbara, the report notes, while Fortescue Metals Group may also deliver an on-year gain of 3 million tonnes in its ore output to reach 193 million tonnes through the commissioning of its Iron Bridge project – also in Western Australia – sometime this quarter.

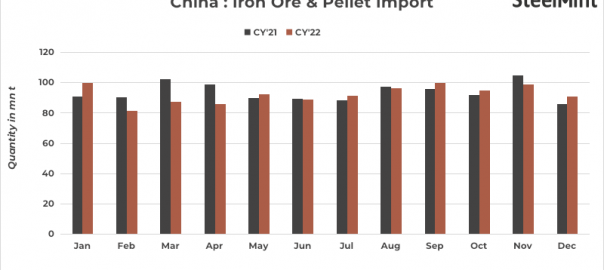

Among the non-mainstream suppliers of iron ore, India’s exports of ore to China will recover gradually to 4.5~5.5 million tonnes/month within this year, the average level until May 2022 when New Delhi hiked tariffs on exports of low-grade iron ore – a policy that was relaxed last November.

Despite this positive outlook for supply, uncertainties still remain in 2023 as some non-mainstream miners may have to halt production if they find that iron ore prices are persistently languishing below $80/dmt, the level generally regarded as their breakeven line, the report warns. The duration of the Russia-Ukraine conflict will also determine how quickly these two countries can recover their ore exports too.

As for China’s domestic iron ore supply, concentrates output will grow by 17 million tonnes from 2022 to top 297 million tonnes this year, Mysteel estimated.

Among the factors that could boost concentrates output include the absence of disruptions (the February 2022 Winter Olympic Games had impacted last year’s output), the effectiveness of China’s COVID-19 containment measures, the granting of approval for North China miners to finally resume production after last year’s mining accidents, and China’s efforts in lifting domestic ore output generally.

On the other hand, steelmakers’ actual demand for ore will ease in 2023, given the central government’s continuing determination to ensure that crude steel output remains flat or below the previous year’s total, the report notes. Another factor influencing iron ore usage will be the degree to which electric-arc-furnace mills can lift their share of China’s total crude steel output, given that Beijing has pledged to raise its self-reliance of Fe products including scrap.

Consequently, the supply-demand imbalance will bring the average price for 62% Fe iron ore down to $100-105/dmt during 2023, the report predicted.

In 2022, China’s prices of imported iron ore endured a roller-coaster ride, as Mysteel Global reported. During January-April for example, Mysteel’s SEADEX 62% Fe Australian Fines strengthened to as high as $160.85/dmt CFR Qingdao on tighter ore supply and after mills resumed operations. After this, the seaborne price fluctuated throughout the rest of the year, though the general direction was a decline due to weaker demand, with the SEADEX index at one point dropping to as low as $79.4/dmt in late October.

On the whole, Mysteel’s SEADEX 62% Fe Australian Fines averaged $120.1/dmt CFR Qingdao in 2022, slumping by 24% on year.

Written by Lea Li, liye@mysteel.com

This article has been published under an article exchange agreement between Mysteel Global and SteelMint.

Leave a Reply