- China aims for boosting blending capacity

- Value-added copper exports reshape China’s trade

China’s copper market continued to reinforce its dominance in the global value chain during the 4MCY’26, as higher domestic refined output, changing raw material sourcing patterns, and stronger exports of processed copper products signaled a structural shift in trade dynamics.

Accounting for nearly 58% of global copper consumption, China remains the single largest driver of global copper flows, with annual demand estimated at over 16 mnt. Against this, the country’s refined copper production reached 14.96 mnt in CY’25 and continued its upward trajectory in 2026, rising to 5.07 mnt in 4MCY’26 from 4.80 mnt in the same period of last year.

China’s refined copper production growth was driven by aggressive smelting expansion despite severe concentrate tightness, mining disruptions, and a sharp collapse in TC/RCs, with benchmark charges falling to $0/t, while spot charges dropped to negative levels. Despite margin pressure, Chinese smelters sustained output through long-term supply contracts, increased secondary copper usage, and diversified feedstock sourcing, prioritizing throughput over profitability.

Processing lower-grade feedstock reduces import reliance

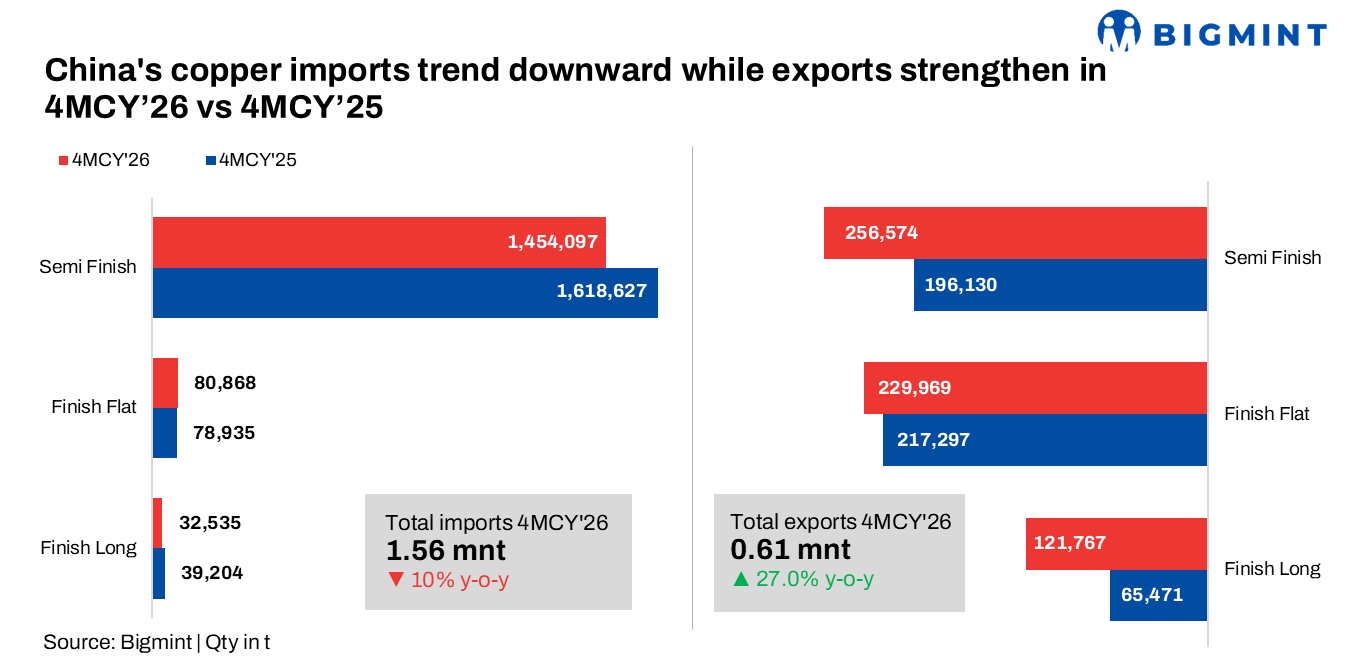

The impact of this changing production structure is clearly visible in China’s import profile. Total copper imports in 4MCY’26 declined 1.8% y-o-y to 12.32 mnt, while April’26 imports fell 7.9% m-o-m to 3 mnt, reflecting reduced dependence on imported refined metal as domestic output strengthened. Refined copper cathode imports recorded one of the sharpest declines, falling 21.6% y-o-y to 0.86 mnt, although April’26 arrivals rose 15.5% m-o-m to 0.27 mnt, likely supported by short-term arbitrage opportunities and tactical restocking.

Imports of finished long products also weakened, with 4MCY’26 volumes down 17.0% y-o-y to 32,535 t, while April imports declined 13.9% m-o-m to 8,316 t, indicating softer dependence on downstream finished copper inflows. In contrast, finished flat product imports remained relatively resilient, rising 2.4% y-o-y to 80,868 t, though April arrivals eased 9.8% m-o-m to 21,026 t.

The major exporting countries are DRC which remained the largest supplier at 0.47 mnt, followed by Zambia (0.17 mnt), Chile (0.12 mnt), and Russia (0.11 mnt). Decline in China’s copper imports mainly supported by the smelting of wider range of lower-grade and complex concentrates domestically, reducing reliance on imported refined copper and overseas blending facilities.

The scrap angle becomes stronger too, as copper scrap imports increased 8.3% y-o-y to 0.84 mnt, despite a 7% m-o-m drop in April’26, as China is structurally shifting toward alternative feedstock strategies to manage concentrate shortages and weak smelter margins. Meanwhile, copper ore and concentrate imports remained broadly stable at 9.92 mnt (-1.2% y-o-y) in 4MCY’26.

Bonded blending hubs fuels the export growth

China’s export profile pointed to a clear strengthening in downstream fabrication activity, with total copper exports surging 27% y-o-y to 0.61 mnt in 4MCY’26, although April’26 shipments declined 16.5% m-o-m to 0.12 mnt following strong March dispatches. The growth was led by value-added copper products, particularly wire exports, which nearly doubled, rising 96% y-o-y to 0.11 mnt, and refined copper cathode exports, which climbed 30.8% to 0.26 mnt.

According to reports, with only around 20% of globally mined copper concentrates directly complying with China’s stringent import quality standards, the development of bonded blending hubs across key ports such as Yantai, Qingdao, Fang Chenggang, Ningde, Zhoushan, and Dongfang has enabled feedstock flexibility for smelters and downstream processors and strengthening raw material accessibility.

Outlook

China’s copper market is expected to remain firm as sustained high smelter operating rates and steady downstream demand continue to keep concentrate requirements elevated, despite persistent pressure from weak TC/RCs. However, Supply-side risks including uncertainties around the Cobre Panama mine restart, Indonesian export permit developments, and potential mining labor disruptions could further tighten global concentrate availability, reinforcing China’s reliance on alternative feedstocks and supporting firm copper market sentiment.

At the same time, the gradual overseas expansion of Chinese copper processors, such as Zhejiang Hailiang’s planned 150,000 t/yr copper processing facility in Saudi Arabia, Tongling Nonferrous, which commissioned 800,000 t/yr of new capacity and the Phase-II Mirador Copper Mine project in Ecuador, may signal a longer-term strategic shift toward globalizing downstream manufacturing capacity and improving supply chain diversification.

Leave a Reply