- Slowing steel exports, consumption to curb iron ore demand

- High finished stocks may prompt blast furnace shutdowns

Mysteel Global: Strong shipping volumes over the past month are likely to cause supplies of imported iron ore in China to rise markedly this month, while demand for the raw material will decline steadily to reflect reduced hot metal production during the summer lull, according to Mysteel’s latest monthly report on the commodity. As a result, Chinese prices of foreign iron ore are forecast to slip further.

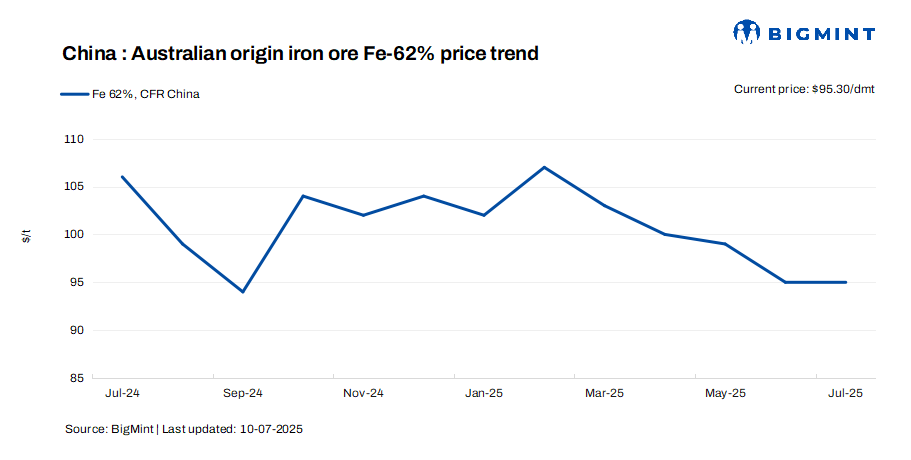

Last month, imported iron ore prices generally declined from May, with the Mysteel SEADEX 62% Australian Fines index falling by $3.2/dmt throughout the month to $93.55/dmt CFR Qingdao on 30 June. Just days earlier, on 25 June, the index had touched an intra-year low of $91.9/dmt before rallying later, Mysteel’s assessment showed.

The ore price slide in June was the combined result of weakening demand and rising supply, when the market was clouded by uncertainties sparked by the Trump administration’s changeable tariff policies.

Production among domestic mills was, in fact, resilient last month, given that June is traditionally a slow month for steel demand. “Mills have been active in production, seizing the tariff pause between China and the US to export steel products,” an iron ore analyst based in Shanghai explained. Starting 14 May, the two countries temporarily cut tariffs on each other’s goods for 90 days until 12 August.

Meanwhile, mills also wanted to reap the healthy profit margins from steel sales before any official notice is released by China’s central government mandating steel production cuts, the analyst added.

Nonetheless, hot metal production among integrated mills in June still dropped from May, albeit slightly, which led to lower demand for iron ore. Hot metal output among the 247 Chinese steelmakers monitored by Mysteel averaged 2.42 million tonnes (mnt)/day last month, lower by 0.8% from the daily average in May.

Looking ahead to July, iron ore demand is expected to decline further, as lacklustre domestic steel consumption and the slowdown in steel exports will lead mills to cut production more aggressively. Particularly, many mills are likely to be burdened with elevated stocks of finished steel products in the second half of the month, so they will probably halt some blast furnaces, the report predicts.

On the supply side, arrivals of iron ore at China’s 45 major ports tracked by Mysteel totalled 100.8 mnt in June, higher by 4.6% from May and by 5.8% from June last year.

The rise in imported iron ore supplies will continue this month, given that ore miners have also stepped up their shipments in recent weeks to polish their half-year or annual performance reports. Mysteel’s tracking of iron ore shipments dispatched from global ore miners in June showed these had risen by 3.9% m-o-m and 1.8% y-o-y to 147.7 mnt.

Given the worsening supply glut, the report predicts that the Mysteel SEADEX 62% Australian Fines index will average around $91/dmt in July, lower than the average of $94/dmt in June. Moreover, the low end this month could reach below $90/dmt, the report warns.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply