- May Day celebrations slow down buying

- EAF mills reduce output amid tight margins

- Global uncertainties keep prices in check

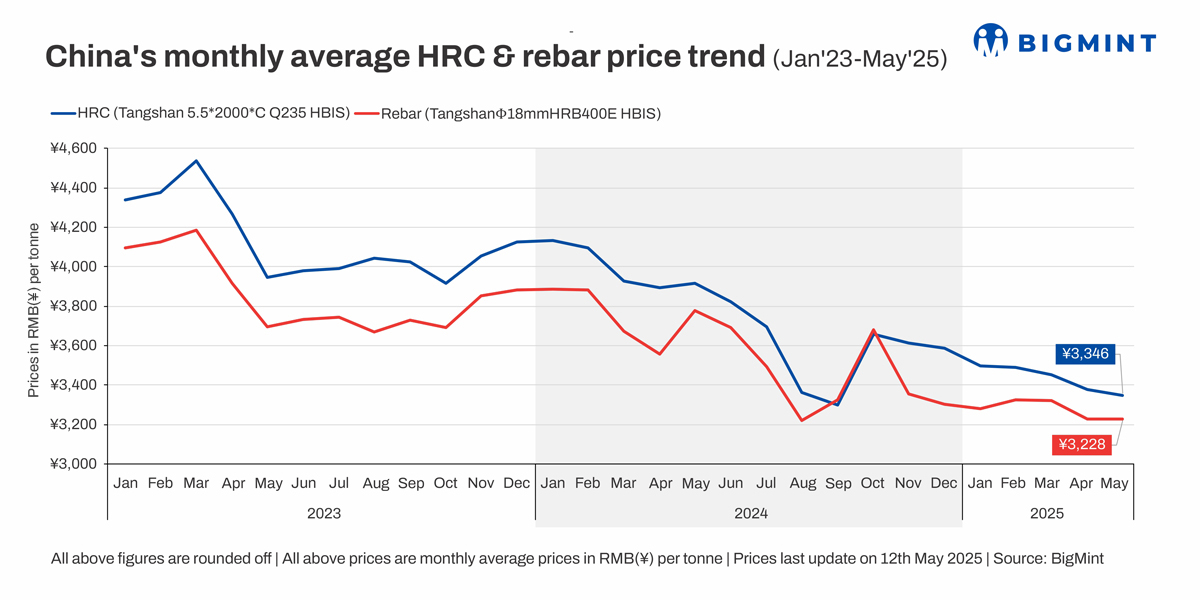

Morning Brief: Chinese steel prices, after a slight rebound in April, have been subdued so far in May. Tangshan’s benchmark hot rolled coils averaged RMB 3,346/tonne ($465/t) till mid-month, down from RMB 3,383/t ($470/t) seen around the same time in April. Rebars remained range-bound at RMB 3,228/t ($448/t) just RMB 6/t ($1/t) up from the same period in April. As per some reports, May prices fell back to the pre-holiday period.

The overall market sentiment had improved slightly with the US dollar on the weaker side, and some positive progress in the US-China trade negotiations. These factors helped the Chinese yuan strengthen notably at the start of May. Moreover, the People’s Bank of China had taken initiatives to support the economy by cutting key interest rates by 10 basis points and lowering the reserve ratio by 50 basis points. This shift in monetary policy signals a clear intention to stimulate the economy. But even with these macro support, the steel sector remains under pressure.

There are indications that prices will remain soft through the remaining part of May as well because of a few factors:

May Day, off-season lull slows buying: The May Day celebration over 1-5 May, 2025 slowed down whatever buying was happening in the market in the previous month. That apart, China is entering the traditionally dull steel demand season. The scorching summer, the core of which falls over June-August, along with frequent rains, reduces construction activity, and correspondingly, steel demand, which, in turn leads to production cutbacks and maintenance shutdowns by mills.

In the first week of May, China’s apparent steel demand reduced by 1.45 million tonnes, while total inventory went up by nearly 340,000 t. Rebar took the biggest hit in both demand and output, while production of HRCs kept climbing a bit.

EAF mills reduce output amid dull demand: EAF mills cut back production in May amid further eroding margins and dull demand. Over 1-8 May, capacity utilisation rate of the 90 independent EAF mills under Mysteel’s regular tracking decreased for the second straight week, albeit by a slower 0.4 percentage points, while their average operational rate also fell by 0.2 percentage points w-o-w.

Some mini-mills in Hubei and Sichuan provinces shut down their furnaces for regular maintenance this week, resulting in a decrease in the country’s output overall. Others in Yunnan and Fujian had completed maintenance and resumed operations, but production remained on the lower side.

Rising global uncertainties: Rising global trade friction, including tariffs and export restriction cases, are expected to continue weighing on the market in May. Combined with the seasonal demand slowdown and weaker cost support, these headwinds are likely to pressure China’s steel market further this month.

China’s National Development & Reforms Commission attributed April’s weaker-than-expected market performance to insufficient supply-side discipline and rising global trade friction, including tariffs and export restriction cases, which are expected to continue weighing on the market in May. Combined with the seasonal demand slowdown and weaker cost support, these headwinds are likely to pressure China’s steel market further this month.

Outlook

Mills outlook on steel consumption for May is dim, as the market is gradually entering the traditional slack season amid a potential supply surplus. Plus, the impact of mounting tariff barriers may lead to fiercer market competition. Under such circumstances, mills may cut back production further. These factors may continue to remain unsupportive of prices in the short term.

Leave a Reply