It is still too early for prices to bottom out as 1) there is no demand improvement signals. 2) the rebar maintenance schedule does not point to continued production cuts. 3) actual steel mills’ production margins are better than computed. Therefore, we view that SHFE rebar will continue to hover close to its offpeak EAF production costs of CNY 3,450/t; possibly dropping below if near-term imbalance becomes apparent.

Over the last week, the key theme for ferrous commodities would be whether the steel balance sheet can balance; either through a stronger demand or a production drop. However, as we all know, both have disappointed the market on the downside, causing a rapid decline in all ferrous commodities prices.

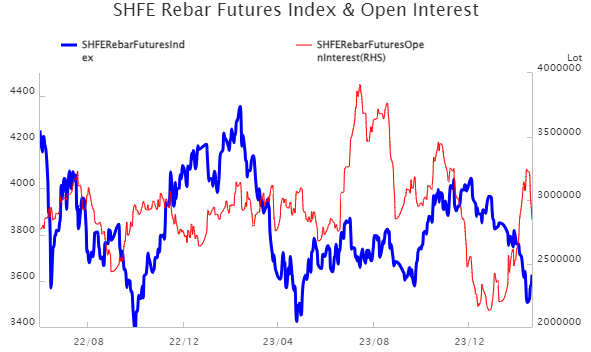

As fundamentals became the key focus, the rise in SHFE rebar open interest accelerated, reaching a four-year high last week. Consequently, the fall in rebar hastened.

SHFE rebar has seen the steepest drop in net buying positions – this is on the back of an extremely weak rebar consumption as it maintains a close to -20% y-o-y decline over the last few weeks. In contrast, HRC is supported by a resilient manufacturing and export demand logic while iron ore and coking coal have “tight supply” logic supporting them. From this perspective, it would suggest that for prices to stabilise, rebar fundamentals contradictions will need to be resolved first.

Written by: Jinshan, Xie

Note: This article has been written in accordance with an article exchange agreement between Horizon insights and BigMint.