- Exports surge in Dec’25 ahead of new licensing policy implementation

- Weak domestic demand, competitive pricing keep steel exports robust

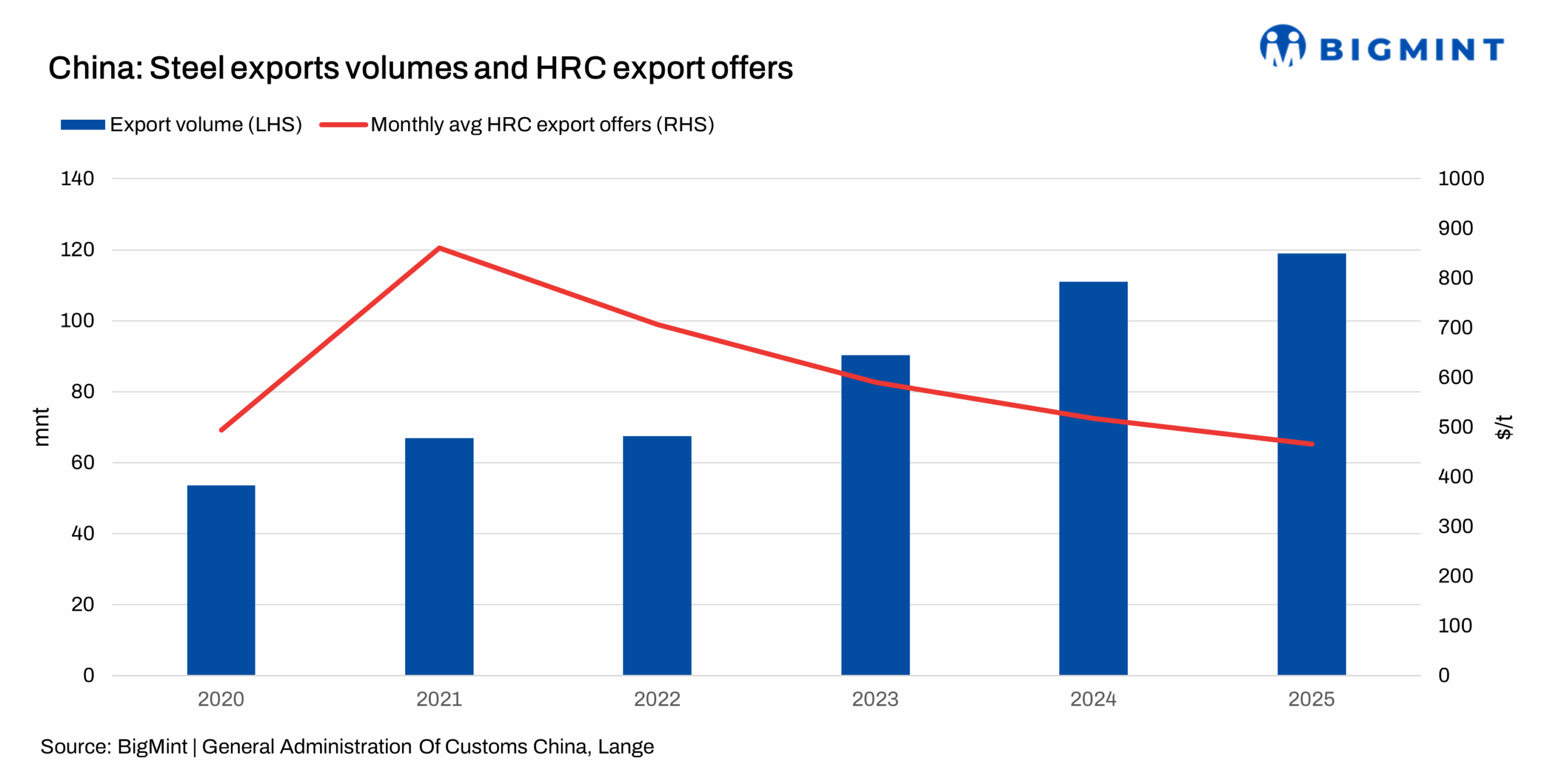

China’s steel exports reached an all-time high of 119.01 million tonnes (mnt) in 2025, up by 7.5% y-o-y from 111.01 mnt in the same period last year, according to the General Administration of Customs.

Moreover, in December 2025, steel exports stood at 11.30 mnt, marking the highest monthly volume of the year and an increase of 16.2% y-o-y from 9.72 mnt in December 2024. On a m-o-m basis as well, steel exports rose by 13.2% from 9.98 mnt in November 2025.

The year-end surge followed the government’s 12 December announcement of an export licensing requirement covering around 300 steel products, effective from January 2026, which prompted a last-minute rush in shipments ahead of the policy’s implementation.

Under the new system, an export licence and a quality certificate will be required at the time of application, and vessels will only be permitted to enter ports after receiving official approval. As a result, Chinese steel exports are likely to slow down in the short term.

Factors driving China’s steel exports

Weak domestic demand: China’s domestic steel demand remained subdued, with persistent weakness continuing to cap any upward momentum in prices. Consequently, oversupply in the domestic market prompted producers to divert more volumes to overseas markets to ease inventory pressure, resulting in a broader supply-demand imbalance.

Competitive pricing boosts steel exports: Chinese prices remained the most competitive throughout 2025, maintaining strong pressure on other exporters. For example, average hot-rolled coil (HRC) export offers fell by $52/t y-o-y to $466/t FOB in 2025 from $518/t in 2024. While Indian HRC export offers (destination ME and SE Asia) also declined sharply, by $89/t y-o-y to an average of $492/t FOB from $581/t in 2024, Indian offers were still higher than China’s.

Furthermore, Japanese HRC export offers declined by $73/t to $470/t FOB in 2025 from $543/t in 2024 and South Korean offers fell by $52/t to $493/t in 2025 as compared to $545/t a year earlier.

On a monthly basis, in December, Chinese HRC export offers stood at $468/t FOB, up by $4/t m-o-m from $464/t in November 2025. Meanwhile, Indian HRC export offers (destination ME and SE Asia) declined by $12/t m-o-m to around $468/t FOB in December from $480/t a month earlier, reflecting intensifying price competition in the export market.

Outlook

China’s weak domestic demand and elevated inventory levels are expected to continue pushing mills to divert larger volumes to overseas markets. Supported by competitive pricing, this trend is likely to persist into the first quarter of CY’26. However, the newly introduced export licensing system may temper shipment momentum in the short term. In the absence of a meaningful recovery in domestic end-user demand, China’s steel exports are expected to remain robust.

Leave a Reply