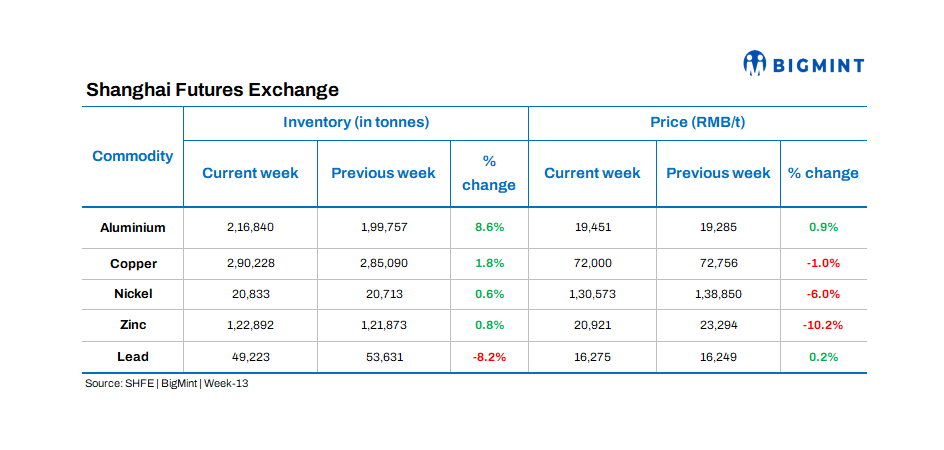

In the week ending Friday, 29 March, inventories of most deliverable base metals in Shanghai Futures Exchange (SHFE)-registered warehouses increased, with aluminum showing the highest percentage gain, while lead experienced the largest outflow.

China’s leading property firms confronted significant challenges with record profit declines and delayed earnings reports amidst the nation’s real estate crisis. Reflecting the broader economic slowdown and subdued consumer sentiment.

Additionally, Chalco voiced concern over Guinea’s bauxite supply risks, as 70% of China’s imports come from there. Plans include developing additional mines in Guinea’s north and exploring collaborations. With declining domestic production, reliance on Guinea may grow, posing challenges amid uncertain global economic conditions.

Commodity-wise stocks, prices

Copper

Copper stocks in SHFE warehouses witnessed a slight increase in inflows for the week. The stocks were up marginally by 1.8% to 290,228 t from the previous week’s 285,090 t. Meanwhile, futures were down by 1% to RMB 72,000/t ($10,064,/t).

Aluminium

Aluminium inventories in SHFE warehouses gained by 8.6% to 216,840 t recording the highest gain among all base metals, while futures prices witnessed a slight uptick to RMB 19,451/t ($2,693/t) for the week.

Aluminium prices inched up amid concerns over sluggish production recovery in China’s Yunnan province. Despite expectations of easier domestic monetary policy and a stronger dollar, investors remained cautious, awaiting signs of demand recovery from China.

Nickel

Nickel inventories saw a marginal rise of 0.6%, reaching 20,833 t, while nickel futures prices decreased by 6%, settling at RMB 130,573/t ($18,084/t) w-o-w.

Zinc

Zinc inventories inched up to 122,892 t, marking a 0.8% increase, while future prices dropped by 10.2% to RMB 20,921/t ($2,897/t) from RMB 23,294/t ($3,226/t) for the week.

Lead

Lead inventories recorded a 8.2% decrease, reaching 49,223 t. Concurrently, futures prices witnessed a rise for the week by 0.2% to RMB 16,275/t ($2,254/t) from the previous week’s RMR 16,249/t ($2,250/t).