- Subdued demand, elevated inventories prompt price cuts

- Mills may seek more cuts as by-product prices rise amid US-Iran tensions

Mysteel Global: The latest reduction in China’s met coke prices took effect as scheduled, with price cuts from two leading steel producers on the same day primarily advancing the implementation. Market participants widely expect continuous downside risks going forward, citing a visible weakness in downstream demand.

Mysteel’s assessments for China’s quasi-first-grade met coke prices for wet- and dry-quenching types last Friday slid to RMB 1,382.8/tonne ($199.7/t) and RMB 1,516/t, including the 13% VAT, respectively, marking separate drops of RMB 45.1/t and RMB 53.8/t from the last session.

Sources revealed that a major steel firm in East China’s Shandong province cut its purchasing prices by RMB 50/t for wet-quenching met coke products and by RMB 55/t for dry-quenching cargoes. After the adjustments, prices of quasi-first-grade products (ash 13%, sulphur 0.75%, CSR 60%, CRI 30%) of wet- and dry-quenching types will be RMB 1,395/t and RMB 1,640/t, respectively, on a DDP basis with VAT included.

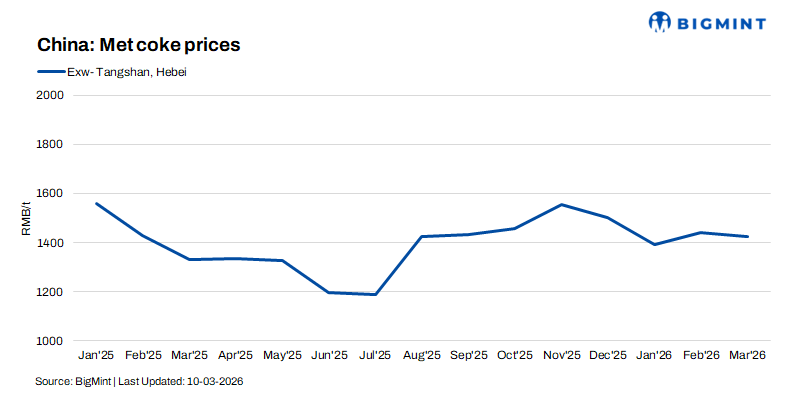

Meanwhile, coke buying prices of another leading steel producer in North China’s Hebei were pegged at RMB 1,560/t and RMB 1,920/t for wet- and dry-quenching first-grade met coke cargoes, DDP with VAT. These two mills’ moves generally marked a nationwide materialisation of the latest coke price cuts, the first bout following a successful RMB 50-55/t increase in end-January, while a few coke producers in Northeast China still held their prices steady due to their extremely low output and profits, Mysteel learnt.

Sources in Inner Mongolia, North China, shared that some coke firms had already offered discounts to their clients ahead of the recent price cuts, highlighting the selling pressures from high stockpiles at local coke plants. “At least one more round of (coke) price cuts is expected,” a source added.

This outlook is also supported by the fact that domestic coke producers may bear less severe losses than anticipated, as the ongoing tensions between the US and Iran have significantly elevated the prices of chemical products, helping offset coke firms’ financial pressures from lower met coke prices. This situation will likely encourage Chinese steelmakers to seek another round of profit reallocation within the industry chain, market insiders noted.

Coke plants were actively making shipments to their steelmaker customers in a continued attempt to lower existing stockpiles, while most of them have yet to lift operations. For steel mills, most only maintained essential coke purchases amid their existing ample inventories.

Some coke producers expect their scheduled maintenance in mid-March to offer slight relief to the downward risks, though the near-term market direction will eventually depend on market sentiment, hot metal production, mills’ profits, as well as coking coal price developments.

The portside coke market held steady on Friday, despite the fact that price reductions at major producing areas continued discouraging portside trading and dampening sentiment. The same day, the first-grade met coke (ash 12.5%, sulphur 0.65%, CSR 65%, MT 7%) traded at Qingdao port, Shandong province, stood flat on day at RMB 1,570/t, ex-stock with VAT, Mysteel’s assessment showed.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply