- Steel slowdown, coke price cuts pressure coal outlook

- Output unlikely to recover in Sep, may support prices

Mysteel Global: The Chinese metallurgical coal market is expected to remain in a tight balance in September, with weaknesses in both supply and demand struggling to steer a clear market direction, according to Mysteel’s monthly report of the commodity.

Some downward corrections are likely in the first half of this month, the report predicts, citing the rising sales pressure faced by coking coal mines due to end-users’ contracted demand.

The downstream steel market may show signs of weakening early this month, dragged by the still sluggish consumption, accumulating inventories and weaker exports. This could further erode steel mills’ profit margins and reduce their tolerance for high-priced raw materials including metallurgical coke and coking coal.

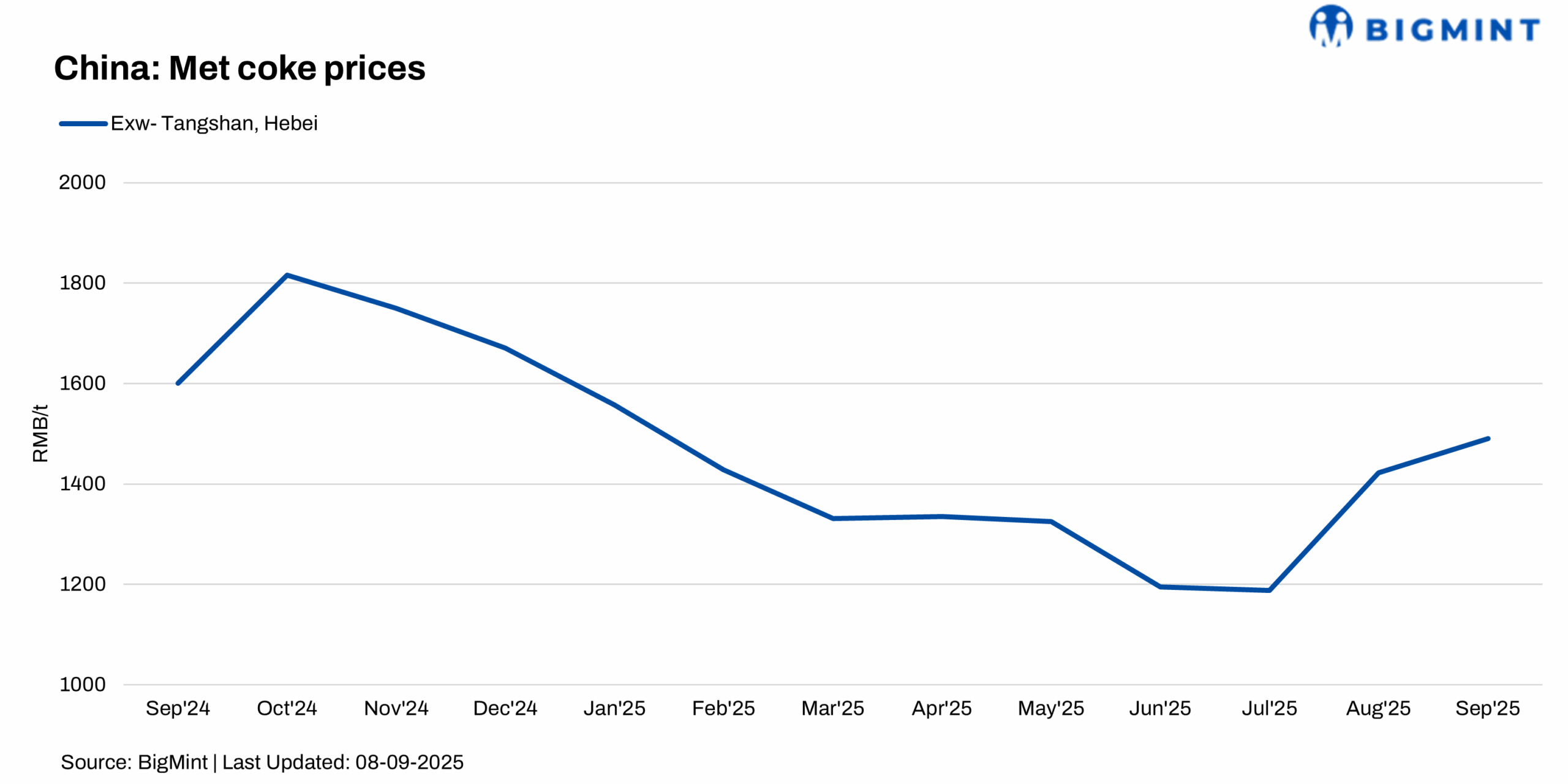

The downside pressure on met coke is already evident, as some steel mills in North China’s Hebei and Tianjin requested fresh coke price cuts of RMB 50-55/tonne (t) ($7-7.7/t) on Friday morning, and market players expect the met coke market to soften further in the short run.

Mysteel’s chief analyst Xiong Chao said domestic steel mills’ hot metal output may not return to previous high levels in September due to shrinking steel margins. The combined daily hot metal output of the 247 Chinese blast-furnace mills that Mysteel surveys retreated by a marked 4.7% w-o-w to average 2.29 million tonnes (mnt)/day over 29 August-4 September, falling below the 240-mnt threshold for the first time since early July.

On the supply side, a quick recovery in coking coal production also looks unlikely in September, although most halted mines in North China’s Shanxi province are scheduled to resume operations this week. Mysteel’s other survey found that the restarts may not add much supply as safety pressures linger.

Moreover, the possibility that Chinese authorities may release more specific measures to tame domestic coal overproduction going forward cannot be ruled out, following submissions of overproduction investigation results from eight major coal-producing provinces and regions in mid-August, Xiong added.

The daily raw coal production among the 523 Chinese coking coal mines under Mysteel’s regular tracking declined by 9.7% from a month prior to average 1.7 mnt/day over 28 August-3 September. The figure also presented a large 16.5% fall compared with the year-ago level.

The tight market balance could prevent China’s coking coal prices from steep retreats in the near term, but the longer-term outlook is still clouded by uncertainty over domestic steel output cuts, said Xiong. If steel mills decide to slash production in September, the coking coal market could take a heavy blow soon; otherwise, the anticipated recovery in steel consumption could give coal prices room to edge higher, he elaborated.

Mysteel’s assessment of the national composite coking coal price sat at RMB 1,189.5/t including the 13% VAT, on 4 September, down by RMB 19.7/t from a month earlier, and the price of the leading brand Anze low-sulphur primary coking coal in Linfen city of Shanxi province posted a RMB 70/t tumble m-o-m to RMB 1,430/t.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply