- Stocks of Fe 56.5% SSF jump 156% y-o-y at tracked Chinese ports

- Removal of BHP ore purchase ban boosts medium-grade demand

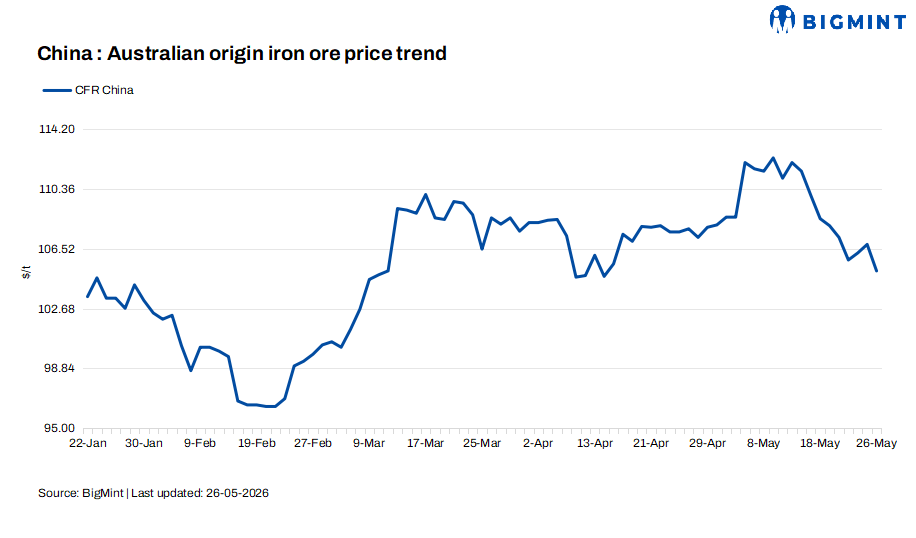

Mysteel Global: Although China’s imported iron ore prices have retreated over the past two weeks, the pace of decline has varied across different products. In particular, low-grade ore has come under greater pressure than medium-grade ore, causing the price spread between the two to widen rapidly, according to Mysteel’s new report.

As of 25 May, the spread between 61.5% Fe PB Fines and 56.5% Fe Super Special Fines (SSF) at Qingdao port under Mysteel’s assessment had expanded to RMB 147/wmt ($21.7/wmt), up 17.6% from a month earlier and the widest so far this year.

The widening gap was mainly driven by a sharper decline in SSF prices compared with PB Fines. On May 25, Mysteel assessed the price of 56.5% Fe SSF at RMB 620/wmt, down RMB 32/wmt or 5% on month, while the price of 61.5% Fe PB Fines fell by only RMB 10/wmt or 1% over the same period.

Low-grade ore has been more vulnerable during the recent downturn in iron ore prices due to a significant increase in supply, a Mysteel analyst explained. By 22 May, total inventories of low-grade ores, including SSF, Blend Fines, Indian Fines, and Silk Road Fines, at the 15 Chinese ports under Mysteel’s tracking had reached 13.89 million tonnes, surging 88% on year. In particular, SSF stocks jumped 156% from a year earlier to 7.79 million tonnes, accounting for 56% of the total.

The significant rise in low-grade ore inventories mainly reflected a substantial recovery in overall shipments from Australian miners in April after weather-related disruptions eased, Mysteel Global understood.

On the demand side, however, Chinese steelmakers’ appetite for low-grade ore gradually weakened as improving profit margins allowed them to use more higher-grade ores. According to Mysteel’s tracking of 247 Chinese blast-furnace (BF) steelmakers, more than half of the mills turned profitable on steel sales since May, compared with a lower proportion in April.

In addition, the purchase ban on BHP’s ore products — most of which are medium-grade ores — was lifted in late April after BHP concluded iron ore sales contract negotiations with China Mineral Resources Group, as reported. With the restrictions removed, Chinese BF mills have become more inclined to use medium-grade ores while cutting back on low-grade ore consumption, the analyst said.

In the near term, inventories of low-grade ore are likely to remain elevated as the peak shipment season in June will bring more cargoes to Chinese ports. While low-grade ore prices are still under downward pressure, the stronger cost-performance advantage of medium-grade ore is expected to support demand and underpin prices. As a result, the price spread between the two products may widen further.

Nevertheless, in the longer run, fundamentals for low-grade ore could improve and support a price rebound. On the supply side, India’s rainy season, which begins in June and Fortescue’s slower shipping season starting in July, are likely to reduce low-grade ore shipments to China over the next two months.

On the demand side, if falling steel prices during the looming seasonal slowdown in steel consumption squeeze mill margins, Chinese BF steelmakers may increase their use of low-grade ore to reduce production costs.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply