- Demand forecast to fall by 10 mnt y-o-y in H2

- Market likely to be oversupplied by 20 mnt

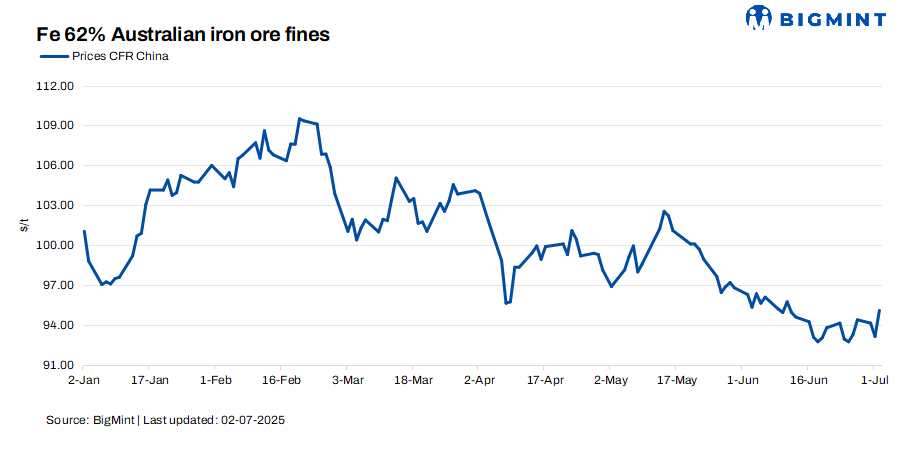

Mysteel Global: After recording declines during this year’s January-June half, Chinese prices of imported iron ore are expected to face more downside risks during the current July-December half, as fundamentals for the steelmaking staple are likely to gradually soften, Mysteel predicts in its latest market outlook for the commodity.

Ore prices track downward in H1 despite resilient demand

As fears of worsening trade friction against China-origin steel products led mills and traders to front-load shipments abroad during H1, the country’s steel export volume soared during the past half year, reflected in the record high of 48.5 million tonnes (mnt) of finished steel that China shipped overseas during January-May. Consequently, domestic integrated steelmakers had been motivated to maintain high hot metal output so far this year, which provided strong support for iron ore demand.

Mysteel’s tracking of the 247 Chinese steel mills it regularly checks showed that their total hot metal production during January-June reached 430 mnt, higher by 3% from H1 last year. Daily hot metal output during the same six months averaged 2.36 mnt/day, also higher by 3.5% y-o-y.

However, resilient demand for iron ore from mills failed to underpin the commodity’s prices. On 30 June, Mysteel SEADEX 62% Australian fines stood at $93.55/dry metric tonne (dmt) CFR Qingdao, lower by a large $7.35/dmt from 2 January. Similarly, the average price of the SEADEX 62% Australian Fines was $100/dmt over the first half this year, well below the $117/dmt average recorded during January-June 2024.

Prices of imported ore had gained some ground at the beginning of the year due to tightening supplies after ore shipments from Australia were disrupted by a series of cyclones. However, since then, the prices generally tracked downwards, under the pressure of recovered supplies, Sino-US-tariff tensions, and the weak outlook for domestic steel consumption.

Supply surplus to weigh on iron ore prices in H2

Iron ore shipments from miners worldwide to all destinations usually see a seasonal rise in the second half of the year, and the increase in H2 this year is expected to be larger. For one thing, iron ore shipments in H1 this year were suppressed by a marked decline in ore shipments from Australia due to adverse weather, as mentioned. For another, global iron ore production will also grow further during the current six months, with a potential gain of 60 mnt in supply from H1 following the launch of new projects, Mysteel estimates.

As the top destination of seaborne iron ore cargoes, China is expected to see its imported iron ore supply increase by 6 mnt y-o-y during H2, accompanied by an extra 7-mnt increase in concentrates output from domestic miners.

In contrast, China’s iron ore demand in H2 is forecast to fall by 10 mnt from the prior year, with hot metal production to decline in response to weaker steel demand, Mysteel predicts.

Specifically, the domestic steel market is unlikely to recover in the remainder of this year while the property sector still struggles and growth in the infrastructure and manufacturing sectors slows. In addition, after the record shipping volume achieved during H1, China’s steel exports are unlikely to maintain the same momentum this half, as challenges posed by higher tariffs and anti-dumping duties imposed by other countries will inhibit export growth.

China’s iron ore market is forecast to be 20 mnt oversupplied during July-December, while domestic mills will continue to keep their in-plant ore inventories at low levels to save costs and increase cash flow. This means most of the supply surplus will be stored at traders’ raw materials yards, a factor adding more downside risks to iron ore prices, as traders are prone to sell on negative signals.

For the current July-December half, Mysteel SEADEX 62% Australian Fines may hover in the $80-85/dmt range, with the average index price throughout this year estimated at $90-95/dmt.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply