- Steel export strength, policy support hopes keep imports high

- Periodic winter, pre-holiday restocking support base demand

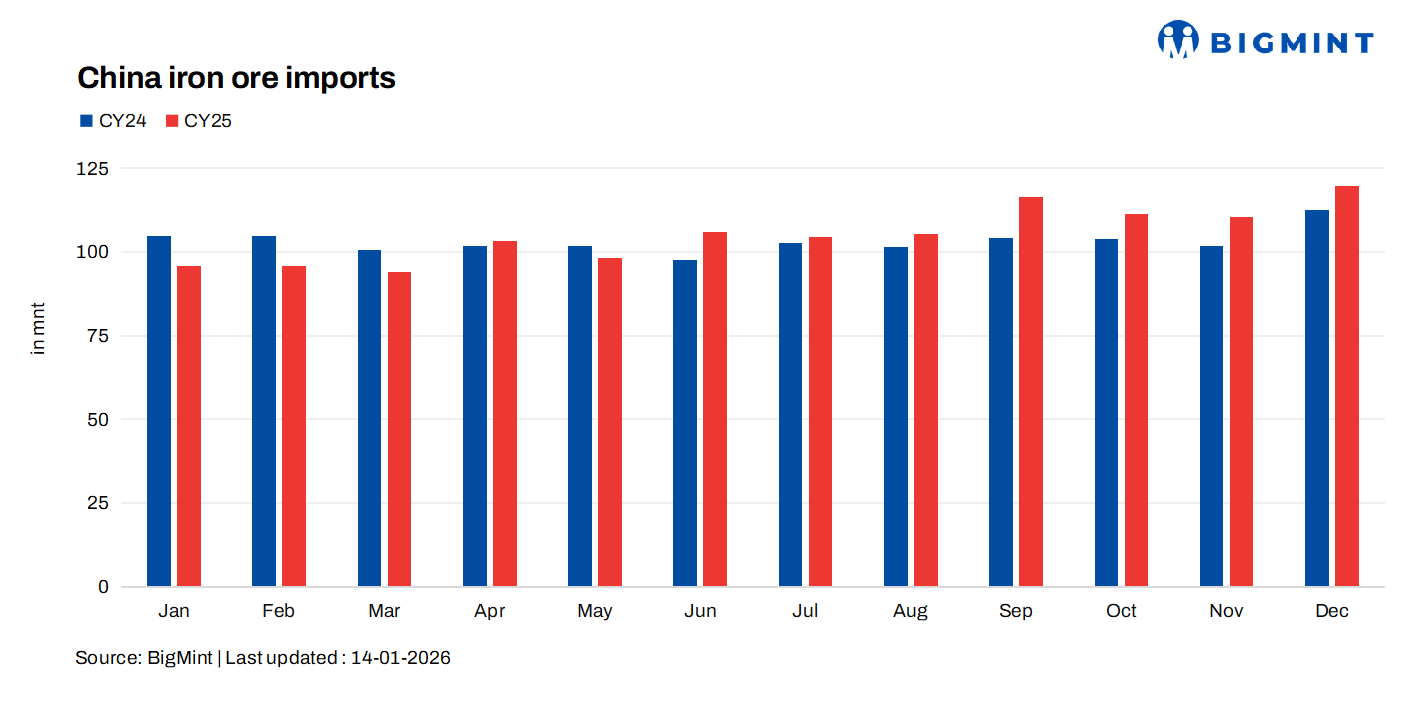

China’s iron ore imports remained resilient in CY’25 at 1,260 million tonnes (mnt), rising 1.8% y-o-y to an all-time high from around 1240 mnt in CY’24, despite weak steel demand and margin pressure. Monthly arrivals averaged 105 mnt, staying consistently above the 100-mnt mark through most of the year. Even with cautious mill buying, stable seaborne supply and structural dependence on imported medium-grade fines kept annual inflows firm rather than contractionary.

Fe 62% Australian fines averaged around $102/dmt CFR China in CY’25, down from $110/dmt CY’24 levels, as steel margins stayed compressed and construction demand remained weak. Prices struggled to sustain rallies despite brief restocking phases and export-driven steel production. Elevated coke costs, tight cash flow, and subdued end-use demand weighed on prices. Adequate global supply and narrowing mid-grade differentials reinforced a cost-focused buying environment throughout the year.

Key factors influencing iron ore imports in CY’25

- Weak domestic steel demand:

China’s steel demand is estimated to have fallen in 2025, weighing on margins and curbing aggressive raw material purchases despite strong exports. Mills stayed defensive, prioritising cash preservation over volume growth as the real estate market also avoided lending support. - High port inventories:

Iron ore port stocks averaged 135-140 mnt during the year, reducing urgency for spot buying and encouraging controlled procurement. Ample stocks kept buyers patient, limiting any panic-driven restocking. - Seasonal restocking cycles:

Periodic winter and pre-holiday restocking supported base demand but failed to lift annual volumes materially above trend. Buying was tactical rather than conviction-led, with mills avoiding inventory risk. - Structural reliance on imported ore:

With domestic ore remaining low-grade and inconsistent, mills continued sourcing imported fines for operational stability, keeping imports high despite weak profitability. Imports reflected necessity, not optimism about downstream demand. - Policy signals, steel export momentum:

Steel export strength (steel exports increased by 6% y-o-y to 101.33 mnt in 11MCY’25) and expectations of macro support led mills to refrain from sharp import cutbacks. However, sentiment stayed cautious as policy clarity remained limited.

Outlook

Global iron ore supply is most likely to grow in 2026 due to the operationalisation of the Simandou, and shipments to China are also expected to increase, adding downside pressure on prices.

Leave a Reply