- Healthy profits, short-term restocking support imports

- Steel output curbs, export slowdown pressure volumes

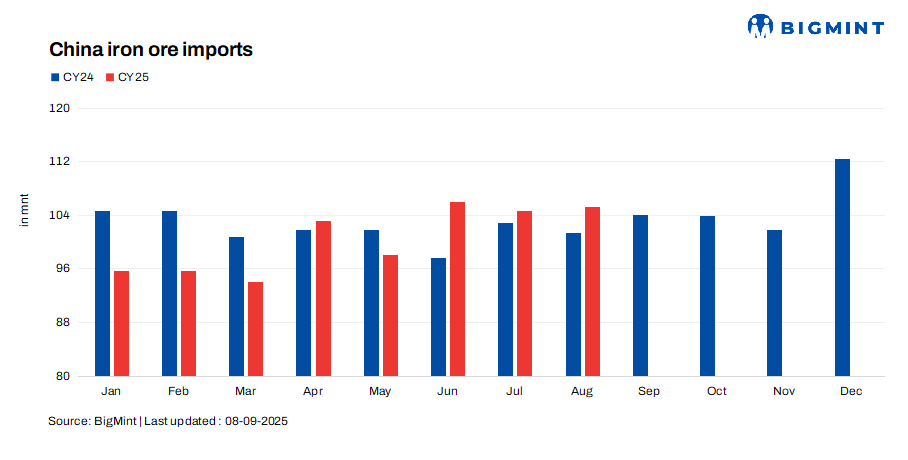

China imported 105.23 million tonnes (mnt) of iron ore in August 2025, reflecting a marginal 0.6% rise m-o-m against 104.62 mnt in July this year. Import volumes were above the 100-mnt mark for the fourth consecutive month. However, imports also stood 1.6% lower y-o-y against 102.81 mnt, largely reflecting the impact of reduced steel production. Cumulative imports in January-August 2025 reached 801.62 mnt, a 1.6% decrease y-o-y.

The August data indicates a delicate market balancing act. Cautious procurement was seen amid weak steel demand and geopolitical uncertainties despite structurally steady import needs. The marginal rise from July’s volumes was supported by temporary factors such as improved mill profitability and short-term restocking. This helped sustain overall import levels, even as domestic steel demand remained under pressure from slower construction activity and production curbs.

Factors influencing iron ore imports

- Supply surge from miners: Global shipments rose as Australian majors pushed record output into the market, narrowing the gap between output and sales. Ample seaborne availability meant China could maintain imports above 105 mnt, though the excess supply weighed on market sentiment and limited restocking urgency.

- Steel production curbs: Environmental inspections and controls imposed around Beijing’s military parade curtailed hot metal output at several mills. These measures, aimed at reducing emissions and ensuring air quality, directly reduced feedstock demand.

- Improved mill profitability: Despite such headwinds, steel mills maintained healthy profitability in August, supported by stronger domestic steel prices earlier in the month. Positive margins encouraged producers to sustain operations and helped prevent a sharper fall in raw material demand.

- Steel export slowdown: Adding to the pressure, China’s steel exports slowed in August as higher domestic prices in July eroded competitiveness overseas. Several buyers cut back on orders, prompting mills to trim output rather than risk stock build-up. This further limited iron ore consumption and contributed to softer imports compared to last year.

Outlook

China’s iron ore imports are likely to stay above 100 mnt in the near term, supported by strong supply and healthy mill margins. However, fragile momentum persists due to weak construction demand, slower steel exports, recurring output curbs, and geopolitical uncertainties, keeping overall fundamentals under pressure despite short-term resilience.

Leave a Reply