- Thin liquidity, stable supply keep imports flat

- Higher costs and weak margins curb buying

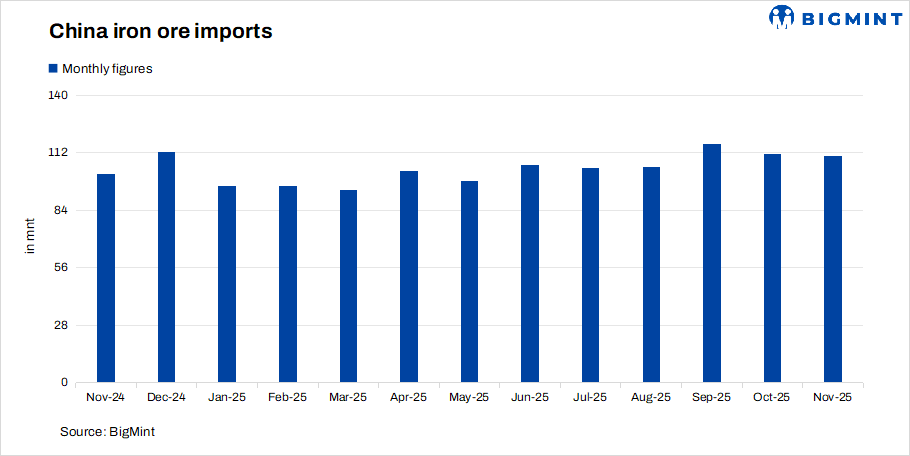

China’s iron ore imports stood at 110.54 million tonnes (mnt) in November 2025, slipping just 0.7% m-o-m from October’s record 111.3 mnt but rising 8.5% y-o-y. Despite the marginal dip, arrivals remained above the 100-mnt mark for the sixth consecutive month, underscoring sustained procurement needs from Chinese steelmakers. The near-steady m-o-m performance reflects a delicate balance between seasonal production slowdowns, cautious inventory management, and consistent seaborne supply, which collectively kept import volumes firm even as downstream steel demand remained soft.

Market sentiment

Fe 62% iron ore prices in China recorded a m-o-m marginal decline to $105/t CFR China through November as the steel market continued to weaken under persistent margin pressure and subdued end-user demand. Early in the month, prices dropped sharply due to sluggish trading activity, rising cost stress on mills, and deteriorating steel fundamentals particularly from the construction sector, where project delays and limited new starts continued to restrict rebar consumption. Mild winter production curbs, soft export orders, and a cautious stance from mills further depressed buying appetite.

Although prices registered small weekly upticks later in November, supported by restocking for January cargoes and mild improvements in macro sentiment, the rebounds were insufficient to offset earlier declines. Market liquidity remained thin, with mills focusing on cost optimisation rather than volume due to higher coke prices, tight cash flow, and overall weak profitability.

Adequate seaborne supply and narrowing mid-grade differentials also kept the market well-balanced, limiting upward momentum. As a result, even with short bursts of buying interest and modest sentiment boosts toward year-end policy expectations, Fe 62% prices remained lower on a m-o-m basis, reflecting the broader weakness in underlying steel demand and muted procurement intent.

Factors influencing Nov’25 imports

- Weak domestic steel demand: Demand across construction, manufacturing, and infrastructure remained subdued, keeping mill margins tight and restricting aggressive buying. With the property sector still struggling and downstream consumption failing to pick up, steelmakers prioritised cost control and maintained cautious procurement strategies. This restrained buying behaviour was a key factor in limiting iron ore import growth during November.

- High iron ore port inventories: Portside iron ore stocks hovered around 139 mnt in November, exerting clear downward pressure on fresh import appetite. Mills avoided accumulating additional inventories amid soft steel sales and uncertain near-term demand. The elevated stock environment encouraged planned, controlled procurement rather than replenishing volumes aggressively, helping keep imports relatively flat m-o-m.

- Winter restocking needs: Despite muted steel demand, controlled winter restocking by mills supported stable import momentum. Many producers secured material in preparation for potential logistics disruptions and production adjustments during the colder months. This moderate restocking helped maintain steady inflows of mainstream grades, preventing a sharper drop in imports despite softer end-user consumption.

- Need for consistent feedstock quality: Chinese mills rely heavily on consistent medium-grade fines for stable furnace performance. Domestic ore quality remains low and variable, prompting steelmakers to maintain regular imports despite weak margins. This structural dependence supported steady inflows even in a soft demand environment.

- Policy signals and market stability: Markets were cautiously optimistic ahead of China’s December policy meetings, expecting potential economic support measures. This sentiment prevented mills and traders from slashing imports aggressively, as buyers sought to keep inventories aligned with possible demand recovery cues.

Outlook

China’s iron ore imports are expected to remain largely stable supported by steady seaborne supply and ongoing winter restocking. However, weak steel demand, elevated port inventories, and seasonal production curbs will likely cap any significant upside. Mills may continue need-based procurement as margins stay tight. Overall, import momentum is expected to stay stable but slightly subdued heading into 2026.

Leave a Reply