- Healthy mill margins, seasonal restocking sustain demand

- Supply surge, steady prices offset weak domestic fundamentals

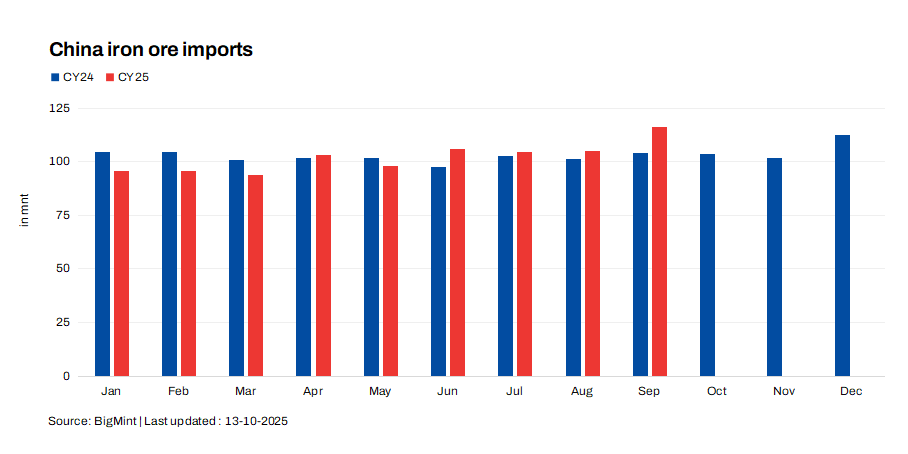

China’s iron ore imports reached a record 116.33 million tonnes (mnt) in September 2025, up 10.6% m-o-m from August, as improved mill profitability and seasonal restocking lifted seaborne demand. This marked the fourth consecutive month above the 100-mnt level, reinforcing short-term market strength.

On a cumulative basis, imports totalled 917.69 mnt during January-September 2025, broadly stable y-o-y (-0.06%). The stable 9MCY’25 performance highlights how strong global supply and resilient mill operations have balanced out domestic demand weakness and policy-driven output controls.

Factors influencing iron ore imports

- Global supply resurgence keeps seaborne flow steady: Major producers in Australia and Brazil maintained elevated export levels through Q3, capitalising on prices holding above $100/t since July. Ample mid-grade ore and softer freights ensured steady inflows, despite uneven steel demand.

- Seasonal demand expectations boost restocking: China’s mills stepped up purchases ahead of the traditional autumn construction period, aided by better margins and a modest rebound in infrastructure orders. The move aligned with Beijing’s supportive tone on industrial stability, which temporarily boosted confidence in steel output.

- Global trade tensions spur stockpiling: A weaker yuan raised import costs, but mills continued buying amid rising steel prices, while US-China trade tensions and tighter export controls prompted early stockpiling as a precaution.

- Exports help offset domestic demand weakness: Healthy mill margins in September enabled Chinese steel producers to maintain production momentum. When domestic demand slowed (due to weak property construction or energy curbs), mills diverted output towards exports, which increased by 9.2% in January-September 2025 at 87.96 mnt as against 80.55 mnt in the year-ago period.

Outlook

China’s iron ore imports are projected to remain above 100 mnt/month through Q4CY’25, supported by ample seaborne supply and seasonal restocking. However, cumulative growth into 2026 may be constrained as domestic demand softens amid a deepening property downturn and renewed US-China trade tensions, keeping prices largely range-bound.

Leave a Reply