- Falling crude steel output, slow demand weigh on sentiment

- Steady restocking, strong miner output keep imports elevated

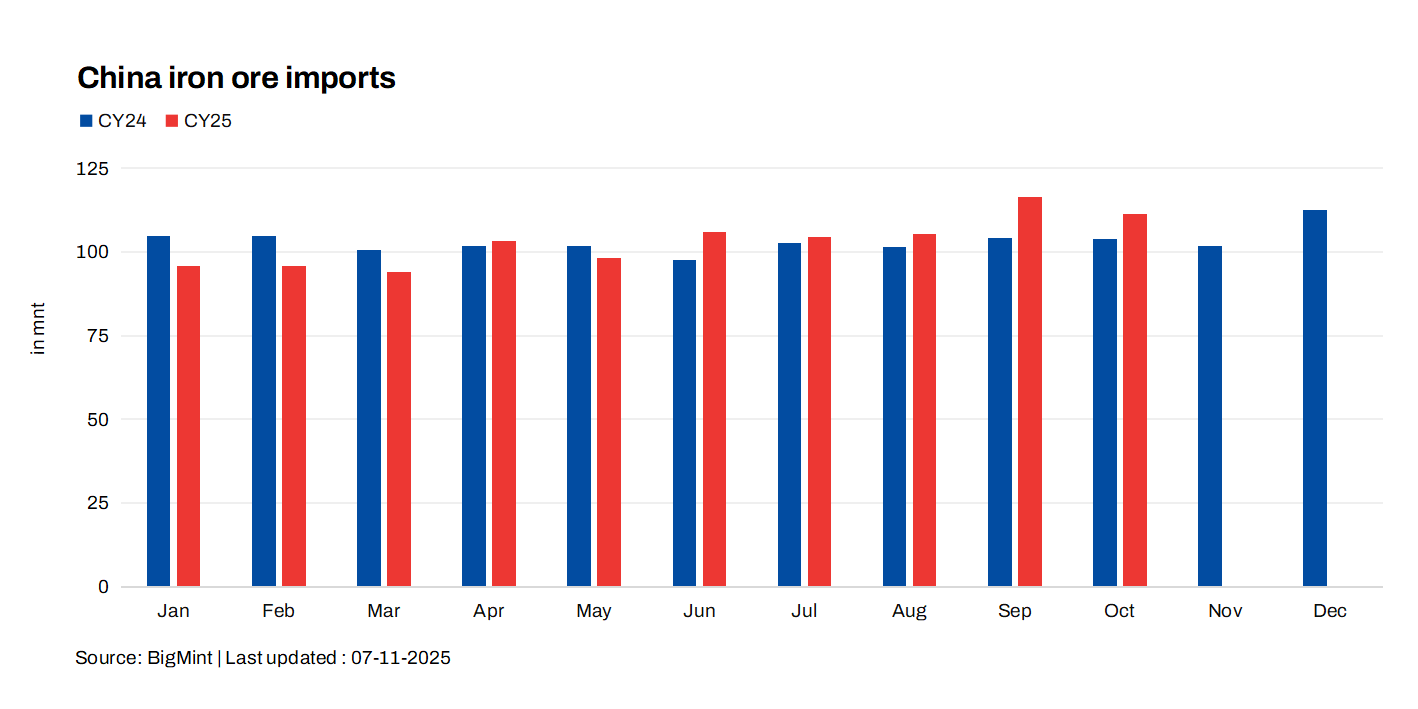

China’s iron ore imports stood at 111.3 million tonnes (mnt) in October 2025, easing 4.3% m-o-m from September’s record 116.33 mnt but up 7.2% y-o-y. This marked the fifth consecutive month above the 100-mnt mark, underscoring steady restocking momentum even as the finished and semi-finished steel markets remained weak.

Market sentiment

Initially, Fe62% iron ore fines prices in China rose to $109/t CFR due to post-holiday restocking. Concerns over sintering and production cuts eased, but uncertainty around talks between an Australian miner and CMRG kept traders divided. Sentiments improved post the US-ASEAN Summit and easing US-China trade tensions. Monthly average prices held largely steady in October, with Fe 62% Australian Fines index averaging $105.7/dmt CFR Qingdao, up marginally by $0.29/dmt m-o-m.

Traders remain watchful as early November activity reflects continued restocking but limited aggressive procurement, keeping price movement subdued.

Key factors influencing October imports

- CISA-affiliated mills’ crude steel output drops: The average daily crude steel output of CISA-affiliated mills stood at 1.817 mnt in late-October 2025, representing a drop of 9.8% from 2.014 mnt in mid-October 2025. Furthermore, output declined by 13.2% y-o-y against 2.09 mnt in late-October 2024.

- Weak domestic demand limits buying appetite: Activity in the finished and semi-finished steel segments stayed sluggish amid slower construction and muted infrastructure orders. Mills maintained cautious procurement, focusing mainly on blending and cost optimisation rather than volume expansion, as margins continued to thin.

- Inventory build-up pressures sentiment: Persistent inflows pushed portside stocks up by 4% m-o-m to 145.42 mnt by end-October, according to Mysteel data. Rising inventories have weighed on early November sentiment, with traders expecting stocks to touch 150 mnt by year-end.

- Iron ore market sees active shipments by miners: China’s iron ore imports remained elevated, as major miners and exporters accelerated shipments to meet year-end targets, supported by seaborne prices staying well above the $100/t mark. This supply strength offset weaker fundamentals in the downstream steel sector, keeping overall import levels stable.

Cumulatively, imports during January-October 2025 reached 1,030.9 mnt, up 0.7% y-o-y. The modest rise highlights how strong global supply and miner output have sustained inflows despite tepid end-user demand and seasonal production curbs in China.

Outlook

China’s iron ore imports are likely to stay near 100 mnt/month through the remainder of 2025, driven by steady supply and stock management. However, low steel demand and high inventories may cap further gains, keeping price sentiment range-bound to slightly soft heading into early 2026.

Leave a Reply