- MIIT may soon unveil plan on stricter output controls

- Raw materials, anti-involution to support steel prices

By MadhumitaMookerji

China’s steel sector is bracing for sharper policy intervention in the second half of 2025 with the Ministry of Industry and Information Technology (MIIT) set to unveil a “Steel Industry Growth Stabilization Work Plan” that could impose stricter output controls and target outdated capacity, according to industry experts.

A recent webinar jointly organised by Horizon Insights and MySteel indicated that MIIT had announced an imminent release of a work plan for stabilising growth in ten key industries,including steel. In addition to restructuring and optimizing supply, some industries will be involved in eliminating outdated capacity. In fact, targeted outdated capacity and their solutions was the most important point in this much-expected meeting to watch out for.

Raw materials support steel prices

Meanwhile, bearish expectations about external demand (exports) following tariff implementation in April-May have been corrected or even reversed. Both raw materials and steel have seen downstream restocking driven by improved expectations. “Until optimistic expectations are validated, prices will trend stronger. Coal and coke will perform stronger than steel and iron ore as their supply environment clearly shifts from loose to tight,” webinar sources said. Additionally, price volatility across all varieties will be significantly higher than in the first half of the year; and close monitoring is needed on how policy statements affect market sentiments.

High-level meetings on anti-involution

Several high-level meetings were held in relation to the anti-involution movement in steel and coal where cut-throat price competition was discouraged:

The Central Financial and Economic Affairs Commission’s Sixth Meeting emphasised on the development of a unified national market that should focus on key and challenging areas, regulate enterprises’ fierce low-price competition and enterprises should be guided towards improving product quality rather than volume, with an orderly exit of outdated production capacity.

President Xi’s inspection in Shanxi underscored that to ensure supply of adequate domestic thermal coal, efforts should be made to promote the coal industry from low-end to high-end, and there should be a shift from primary fuel to high-value products. The meeting also stressed that efforts must be made to continue with advanced energy-saving and carbon reduction strategies in key industries, while ecological restoration of mines should be diligently carried out for maintaining environmental balance and safety. Plans are afoot to strengthen safety measures to prevent and curb major accidents.

State Council Information Office held a press meet outlining plans for stabilising growth in ten key industries, including steel, metals, petrochemicals, and building material. It was also decided that the MIIT will promote efforts in key industries on restructuring, optimising supply, and eliminating outdated production capacity.

Emphasis on quality, not quantity

Based on the production cut rumours from the first half of the year, if implemented, these will still have a significant impact on the production of crude steel, pig iron, and hot metal. Current policy trends are clearly shifting towards improving production quality rather than increasing production quantity. Therefore, an important document to offer direction regarding this will be the “Steel Industry Growth Stabilization Work Plan,” which is expected to be released by the MIIT.

Three likely scenarios

The webinar also gave indications of three market paths that could emerge:

1) De-capacity policy: In such a scenario, spot profits will continue to improve, steel stocks would further rise, and long-term futures market profits will improve significantly.

2) Production control policy: This second scenario presupposes that spot profits will remain stable or moderately increase, and futures market profits recover to above spot profit levels. In these first two scenarios, the price of steel will be noticeably stronger than iron ore.

3) No further tightening of production limits: This scenario is divided into two stages. In the first stage, spot profits will initially shrink because of a sustained rise in iron ore and coking coal prices, while steel production continues to increase. In the second stage, a few weeks later, accumulated steel inventory will lead to the next stage’s conflict resolution through price reductions to clear inventory, with the futures market reacting early.

Outlook

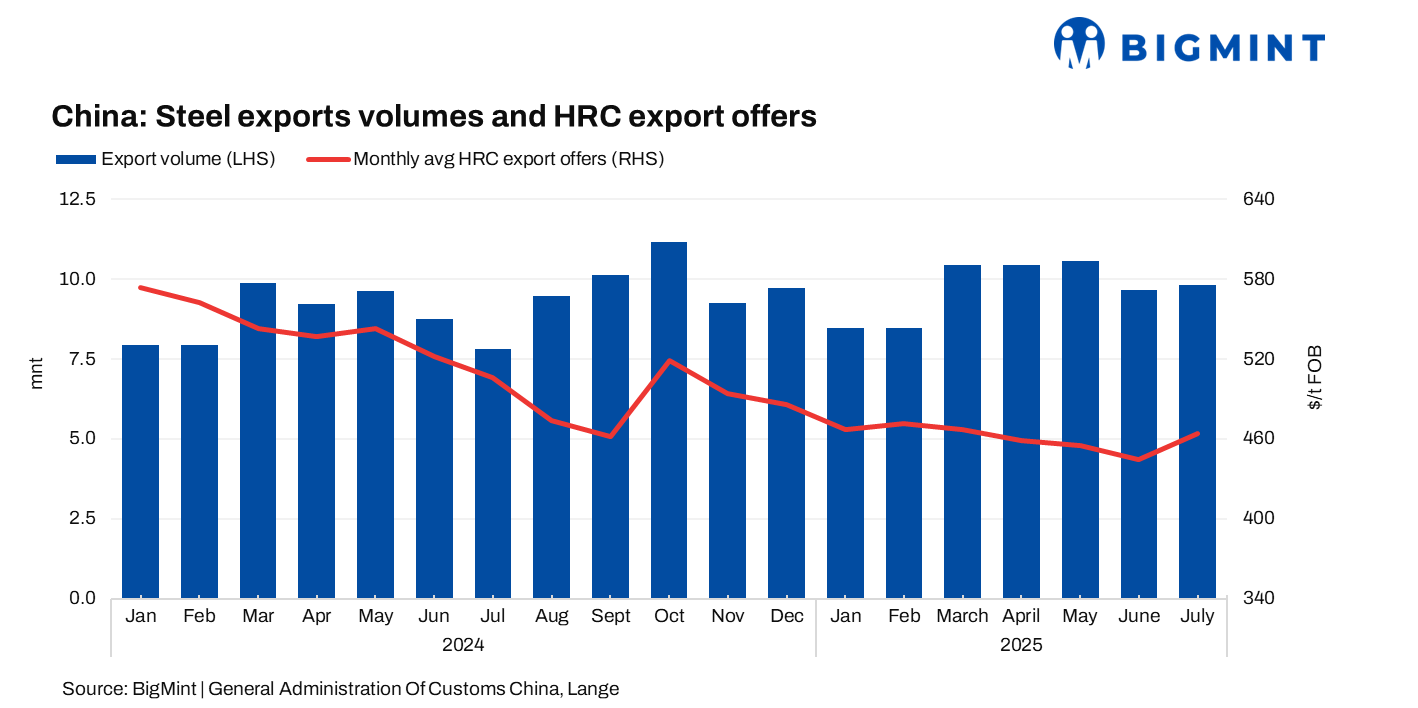

Domestic demand in the second half of the year is expected to be limited and may focus on overseas demand, particularly in relation to indirect exports. Direct steel exports are price-sensitive; and recent order intake has slowed after price increases, as per sources.

Direct steel exports are considerable with a total share that ranges from 4% to over 10%, primarily serving to balance domestic supply and demand. The main adjustment mechanism is the price differential between domestic and international markets. If the production limits in the second half of the year are not significant or measures are lax, export offers will continue to exert an upward pressure on steel prices. However, if production limits are strict, the export window will temporarily close, with some exports flowing back to supplement domestic shortages. Therefore, the volume of steel exports going forward will largely depend on whether strict production limit measures are implemented in the second half of the year.

Leave a Reply