- BF-BOF production share to fall to 55% from today’s 88%

- Tight scrap supply, nascent DRI scene may cap EAF growth

Mysteel Global: China’s transition towards low-carbon steelmaking is poised to significantly reduce the country’s iron ore demand in the long term, though meaningful declines are unlikely to materialise for at least several years, according to Su Buxin, deputy secretary general of the Metallurgical Council of the China Council for the Promotion of International Trade (MC-CCPIT).

Speaking at the 4th High-Quality Development Conference of the Steel and Mining Industry Chain currently held in Rizhao in East China’s Shandong province, Su noted that global headwinds – including trade tensions, tariff disputes, and geopolitical instability – are accelerating the shift towards greener steel production worldwide, with China playing a central role.

“The global demand for green steel is projected to reach 330 million tonnes (mnt) by 2035, accounting for approximately 17% of total steel demand,” Su said, citing data from McKinsey Global Institute.

Green steel refers to steel produced with carbon dioxide emissions of less than 0.6 tonnes (t) per tonne of steel, Mysteel Global understands.

Of the estimated 330 mnt of green steel demand, China is expected to account for 90 mnt, or nearly 30% of the total. Within China, the construction and transportation sectors will drive demand, with projected consumption reaching 60 mnt by 2035.

To meet this demand, China is expected to significantly expand its green steel production capacity. “By 2035, China will contribute 130 mnt of green steel capacity to the global total of 400 mnt,” Su stated.

Su also highlighted that China has implemented a series of policy and regulatory innovations over the years to decarbonise the steel sector. The most recent initiative includes the integration of the steel industry into the national carbon emissions trading market in March.

From a production perspective, Su emphasised that China’s steelmaking will gradually shift away from the traditional blast furnace-basic oxygen furnace (BF-BOF) route. He projected that by 2035, the share of BF-BOF steel production will fall to 55.4%, a sharp decline from today’s 87.6%.

In contrast, steel production via the electric-arc-furnace (EAF) route will gain prominence, with its share rising from 11.9% currently to 39.6% by 2035. Meanwhile, China’s direct reduced iron (DRI) production, though still limited, is expected to achieve initial breakthroughs, contributing about 5% of total steel output by 2035.

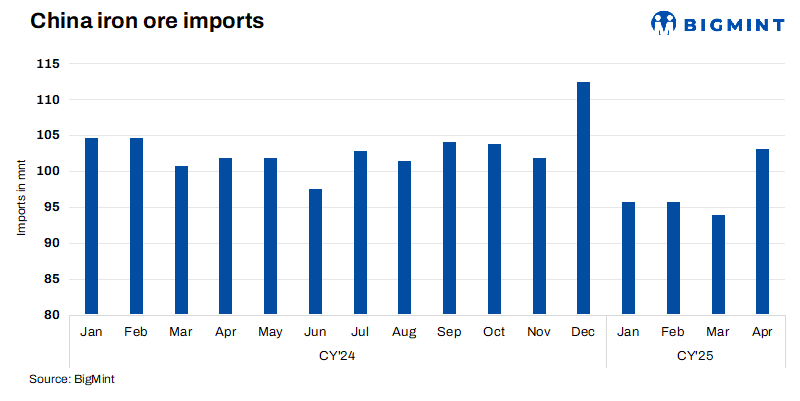

Despite this transition, Su believed that China’s iron ore demand will remain robust in the short term, particularly over the next five years.

“Most BFs in China are expected to remain operational until at least 2040, so the BF-BOF route will retain its dominance for decades,” he explained. “In addition, China’s steel scrap supply remains tight, constraining the development of EAF capacity, while DRI production is still in its infancy.”

Su concluded by stating that a more notable decline in China’s iron ore demand is expected only after the country reaches its peak carbon emissions around 2040.

“By then, EAF-based steelmaking is expected to become mainstream in China, accounting for 56.1% of total steel output,” he said.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply