- Global iron ore shipments expected to surge in Aug’25

- Demand lull, production curbs may cap hot metal output

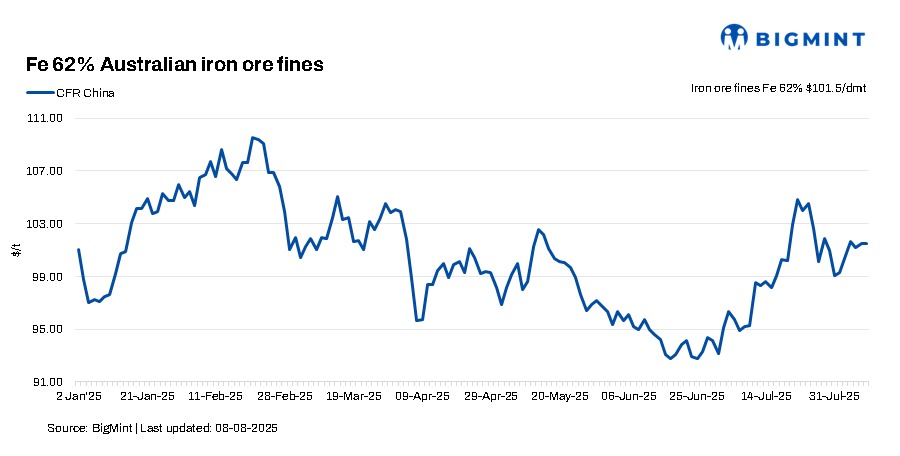

Mysteel Global: Chinese prices of imported iron ore will likely be subject to downward pressure this month, as the bullish market sentiment that strengthened ore prices in July will give way to weakening fundamentals, according to Mysteel’s latest monthly report on the commodity.

The past month saw China’s imported iron ore prices rebound sharply in sync with the broader ferrous market. The catalyst was several developments seen favourable to the steel industry, which lifted market sentiment, including Beijing’s campaign to reduce unproductive competition and address overcapacity issues across vital sectors of the economy, as well as the launch of a massive hydropower project in Southwest China.

Mysteel’s SEADEX 62% Australian Fines index peaked at $104.35/dry metric tonne (dmt) CFR Qingdao on 22 July, its highest level since March this year, before retreating afterwards under the pressure of waning steel consumption from end-users. Despite the pullback, the index still logged a $4.7/dmt rise from end-June to settle at $98.25/dmt on 31 July, Mysteel’s assessment showed.

For this month, however, the report suggests that with market sentiment cooling, imported iron ore prices will be more influenced by fundamentals, which are expected to soften.

On the supply side, global iron ore shipments are projected to rise significantly this month, with some miners having completed maintenance stoppages. In addition, major iron ore miners in Australia posted record-high output during the April-June quarter, which created an “unprecedented” gap between their output and sales, their quarterly reports released last month showed.

“The widening gap between iron ore output and sales points to mounting ore stocks at miners,” the report notes, adding that this will likely prompt them to accelerate shipments in the coming months to reduce stockpiles.

In contrast to the expected rise in iron ore supply, all indications are that demand for the steelmaking material in China will decline this month. The ongoing summer lull in steel consumption in the domestic steel market, together with potential environmental protection-driven production restrictions, will take a toll on hot metal output at domestic mills.

In addition, China’s steel exports are expected to shrink in August, as rapid increases in steel prices last month dampened the buying appetite of some overseas buyers. The lower export orders could prompt mills to make additional production cuts, further depressing iron ore demand.

While weakening fundamentals will depress iron ore prices, the downside room is limited, given that mills still enjoy healthy profits on steel sales and are reluctant to reduce production — with their firm ore demand ensuring that traders will keep their offer prices high. The Mysteel SEADEX 62% Australian Fines index is expected to fluctuate between $92-100/dmt in August, with the average below July’s level of about $99/dmt.

Nonetheless, greater risks to iron ore prices will emerge should steel stocks begin mounting while no production cuts are mandated by central government authorities, causing the ferrous market to nosedive, the report warns.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply