- Tight supply and cost support underpin prices

- ZCE Feb’26 futures edge down by $4/t w-o-w

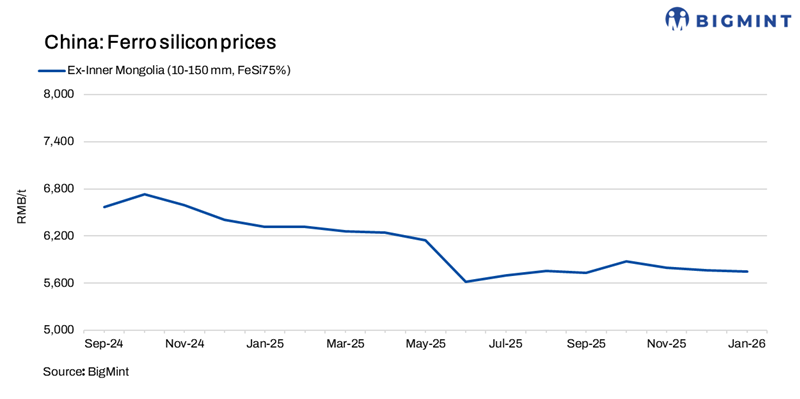

Prices of 72% silicon grade remained flat w-o-w at RMB 5,260-5,500/t ($751-786/t) ex-factory, inclusive of taxes, while prices of 75% silicon grade remained unchanged w-o-w at RMB 5,700-5,930/t ($815-848/t) ex-factory, inclusive of taxes.

Ferro silicon prices remained stable across grades last week, supported by supply-side tightening and firm cost support, while weak spot demand and year-end liquidity constraints kept trading activity muted and price movements limited.

Market recap

Subdued spot demand keeps market cautious: Domestic ferrosilicon prices remained stable last week, supported by supply-side tightening following factory shutdowns in some regions. Elevated production costs and anticipated demand from upcoming steel mill tenders reinforced producers reluctance to offer lower prices. As a result, low-priced material was limited in the market, providing firm support to prevailing prices.

Meanwhile, spot demand remained weak, and year-end liquidity tightening led to a cautious, wait-and-see sentiment. As a result, limited buyer-seller activity kept trading volumes low and prices largely stable.

ZCE futures hold firm w-o-w: Ferro silicon futures on China’s Zhengzhou Commodity Exchange (ZCE) for February 2026 delivery remained largely stable, edged down by RMB 30/t ($4/t) w-o-w to RMB 5,496/t ($785/t) on 31 December compared to RMB 5,526/t ($790/t) on 24 December .

Outlook

Domestic ferrosilicon prices are expected to remain range-bound in the near term, supported by supply constraints, with market direction driven by steel mill tenders in January.

(With inputs from CBC)

Leave a Reply