- Prices likely to bottom out around Aug’26

- Ferro chrome output up 33% y-o-y in Jan-June

Mysteel Global: China’s high-carbon ferro chrome (FeCr) market is expected to face downside pressure during H2CY’26, as supply outpaces demand, Mysteel’s new report on the commodity suggests. This supply pressure stems from rising domestic output, resurgent overseas shipments and upcoming capacity additions, the report notes.

Spot prices

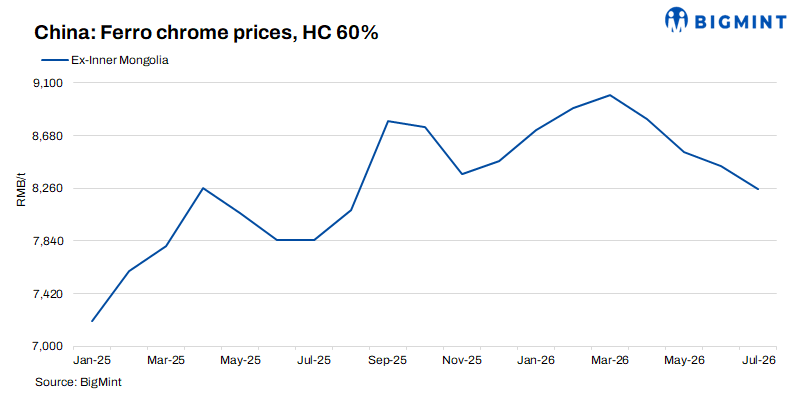

Spot ferro chrome prices in China are expected to extend their declines in July. The rainy season in southern China is set to fill hydroelectric dams and prompt utilities to trim electricity tariffs, allowing smelters in the region to gradually lift operating rates. This, combined with subdued demand, is weighing on prices, the report forecasts.

Prices are likely to bottom out for the year around August, in line with historical seasonal patterns. A modest rebound may follow in September-October, bolstered by the traditional peak-demand period in autumn and rising power costs from the approaching dry season in South China, a period when hydropower output declines. However, any recovery is expected to be short-lived, with prices gradually retreating after the autumn demand boost fades.

Domestic output, South African supply

China’s ferro chrome production continues to climb and is expected to hit multi-year highs in 2026, with output in this year’s January-June half estimated at around 5.34 million tonnes, up 33% from the same period last year, the report notes.

In addition to robust domestic supply growth, South African production is set to recover in H2. The country’s largest ferro chrome smelter, Glencore Merafe Chrome Venture, is expected to soon restart its Boshoek and Wonderkop smelters in South Africa’s North West Province where operations were suspended in May and June last year, respectively. The restart follows a negotiated pricing agreement reached late last month with state-owned utility Eskom, which gives effect to the previously approved Rand 0.62/kWh ($0.038/kWh) preferential tariff scheme for the domestic ferro chrome industry, as reported.

The resultant increase in South African ferro chrome output will likely see a fresh wave of shipments entering the Chinese market, placing further pressure on domestic prices.

Stainless sector demand

China’s crude stainless steel output reached nearly 40 million tonnes last year and already topped 21.12 million tonnes in this year’s January-June half, according to the latest Mysteel survey of 43 Chinese mills. Total output in 2026 is projected to grow by around 5% from last year, sustaining stable consumption of ferro chrome, the report observes.

Demand from the domestic specialty stainless steel sector also remains steady. However, the pace of demand growth is unlikely to match the rapid expansion in ferro chrome supply, the report warns.

New capacity

More than 1 million tonnes of new ferro chrome capacity is scheduled to come online in China this year, mostly in Inner Mongolia, with the new furnaces mainly being large-scale units, Mysteel Global learns. A large portion of the new capacity is expected to be commissioned in the October-December quarter, potentially intensifying market pressure towards year-end.

Overseas, cheaper power tariffs in South Africa should see most local ferro chrome furnaces there brought back online, while capacity additions in India and Indonesia-albeit modest-will further boost global supply.

Outlook

With supply in China rising from a combination of existing domestic and new capacity, plus climbing imports from South Africa, at a time when domestic demand growth remains relatively modest, the market for high-carbon ferro chrome looks set to face significant headwinds in H2, the report concludes. A supply glut could emerge if demand fails to pick up, which would keep prices under sustained downward pressure, it says.

Note: This article has been published in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply