- Production costs surge for ferro chrome manufacturers

- Oman’s new chrome ore export policy may alter global supply chains

CBC: The ferro chrome market remained largely steady overall, but underlying structural differences in supply and demand shaped varied performances across segments. Seasonal factors, policy changes, and fluctuating exchange rates all contributed to a cautious market atmosphere.

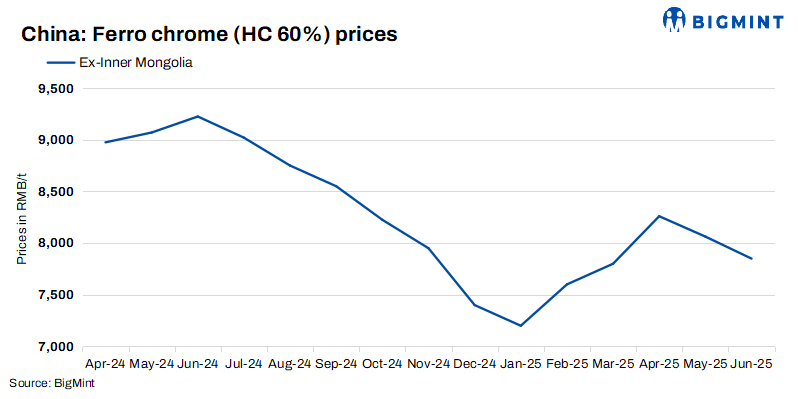

High-carbon ferro chrome prices saw slight decline by RMB 100/t ($14/t) w-o-w to RMB 7,440-7,850/t ($1,037 – $1,095 /t) exw, including taxes.

However, medium-carbon ferro chrome prices rose by RMB 300/t ($42/t) w-o-w at RMB 12,800-13,000/t ($1,785-1,813/t) exw, including taxes.

Market recap

High-carbon ferro chrome under pressure, low-carbon up on new energy demand: High-carbon ferro chrome is experienced downward pressure due to the stainless steel industry’s seasonal downturn and reduced bidding activity from major steel mills. In contrast, medium-carbon ferro chrome continue to receive support from the growing demand in new energy sectors such as wind turbines and industrial motors. This demand shift allows for price resilience in these segments, even as the broader market adopts a more conservative posture.

Policy and cost pressures influence supply strategy: The ongoing removal of preferential electricity pricing in Inner Mongolia is a key development that’s increasing production costs for ferro chrome producers. However, these costs haven’t yet fully translated into terminal prices. To cope, some manufacturers opted for production maintenance to manage inventory pressure. The cautious attitude among traders, influenced by exchange rate volatility, further contributes to reduced liquidity and risk-averse operations in the current market landscape.

Raw material trends and international impacts shape future outlook: Chrome ore prices remained volatile, with loose South African quotes weighed down by port inventories, while Turkish high-grade ores hold firm due to elevated mining costs. A noteworthy factor is Oman’s new chrome ore export policy, which could significantly alter global supply chains in the long run. Currently, raw material procurement is mostly driven by immediate replenishment needs, and the reluctance of traders to stockpile adds to the market’s tight liquidity.

Downstream stainless market continues to weaken: Stainless steel, the primary downstream market for ferro chrome, continues to show weak demand. A major North China steel plant’s maintenance has further reduced consumption of high-carbon ferro chrome. Overseas, European stainless buyers are winding down pre-summer orders, and Southeast Asian interest has declined amid currency volatility. End users maintain low inventories, and price reductions in steel bidding remain a dominant retail market trend.

Outlook

The ferro chrome market is poised for short-term divergence, with high-carbon grades facing downside risk amid weak stainless demand. In contrast, low-carbon varieties remain supported by industrial demand and elevated costs, while policy and supply shifts introduce further uncertainty in Q3.

Leave a Reply