- Stainless steel makers planning to lift output in Feb

- FeCr production declines in Jan, easing oversupply

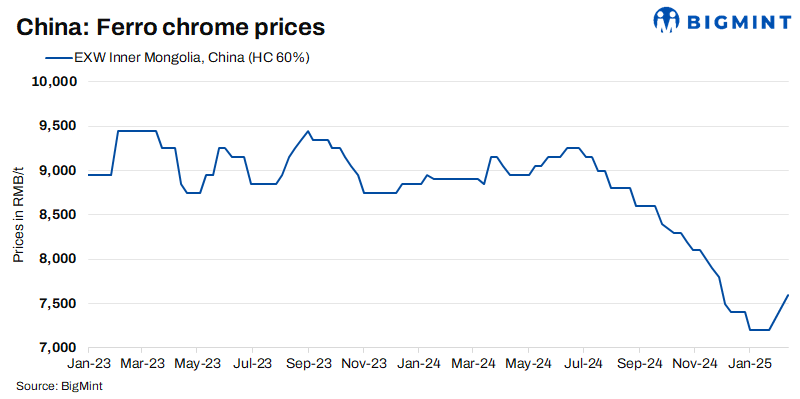

Mysteel Global: After steadily declining for more than six months, China’s ferro chrome market is showing signs of improvement following the end of the Chinese New Year (CNY) holiday last week. The rebound marks a change after a prolonged period of pressure, with global chrome ore traders leading the price hikes, sources noted.

On 12 February, Mysteel assessed spot prices of high-carbon ferro chrome with 55% chromium content in North China’s Inner Mongolia at RMB 7,500/tonne (t) ($1,028.9/t) exw, including tax, higher by a sizeable RMB 400/t from just one month earlier.

The sharp rise in ferro chrome prices was largely driven by stronger chrome ore tags this month. Mysteel’s assessment indicates that, as of 12 February, CIF prices of 40-42% chrome concentrate shipped from South Africa to Tianjin Port had rebounded to $240/dry metric tonne (dmt), up by $40/dmt in the space of a week and representing the first significant rebound after the prolonged decline since last August.

Meanwhile, portside prices of chrome concentrate also strengthened markedly over the past week, with Mysteel assessing 40-42% chrome concentrate at Tianjin Port on 12 February at RMB 51/dry metric tonne unit (dmtu), an increase of RMB 6.5/dmtu from 13 January.

However, this gain was slightly smaller than that seen in seaborne cargoes, primarily due to the climb in port stocks during the CNY holiday as a result of low buying activity among ferro alloy smelters, insiders observed.

As of 7 February, chrome ore stocks at Chinese ports monitored by Mysteel stood at 3.14 million tonnes (mnt), a three-year high and representing a 13.6% increase from 31 January.

The accumulation of chrome ore stocks was mainly due to the slow buying activity, stemming from reduced production by domestic stainless steelmakers in January. According to Mysteel’s latest survey of 43 producers nationwide, China’s crude stainless steel output fell significantly last month, dropping by 580,800 t or 16.9% m-o-m, to 2.86 mnt.

Despite the high stocks of chrome concs at ports, market sentiment among ferro alloy smelters has so far not been heavily impacted, as stainless steel producers have shown a keen interest in ramping up production this month. This suggests that demand for ferro chrome products should turn robust in the near term, sources noted.

This month, crude stainless steel production among the mills monitored by Mysteel is expected to increase by 9.9% from January to 3.15 mnt. In addition to the anticipated gradual recovery in demand now that the CNY holidays are over, some domestic mills are scheduled to resume production after completing regular maintenance.

China’s ferro chrome output continued to decline in January, alleviating the oversupply conditions seen in the second half of 2024, according to a Wuxi-based analyst.

Mysteel’s survey of ferro chrome smelters hosting 95% of domestic capacity revealed that the total output of high-carbon ferro chrome decreased further in January by 2.2% m-o-m to 635,100 t.

While the ferro chrome market has performed strongly recently, analysts caution that if output rebounds this month, the increased supply could put downward pressure on prices.

Additionally, the recent uptick in nickel pig iron (NPI) prices – another material key to stainless steel production along with ferro chrome – may limit further hikes, as stainless steelmakers face budget constraints.

As of 12 February, prices of 8-10% grade NPI in East China’s Jiangsu province under Mysteel’s assessment were at RMB 970/t, including delivery and the 13% VAT, higher by RMB 20/mtu from that on 10 January.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply