- Improved margins support northern production

- Seasonal power constraints limit southern supply

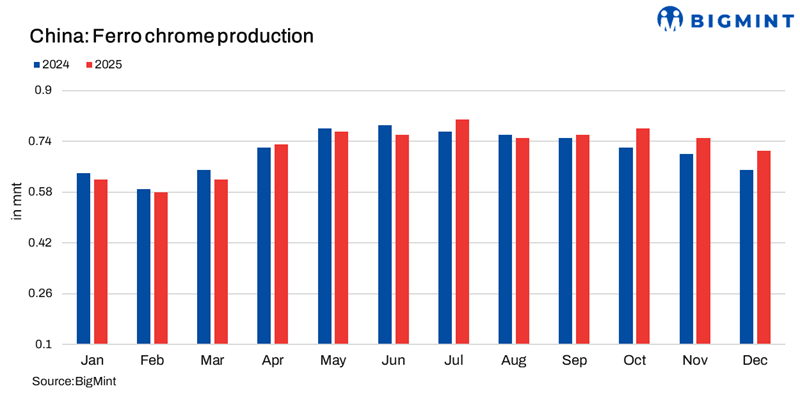

Mysteel Global: China’s production of high-carbon (HC) ferro chrome, a key ingredient in stainless steel, continued expanding during December, with strong production among smelters in northern China offsetting seasonal declines in the south, according to Mysteel’s latest survey covering 178 domestic smelters.

The survey results show that nationwide HC ferro chrome output reached 887,200 tonnes (t) last month, marking a modest m-o-m increase of 0.7% and yet a significant y-o-y surge of 36.5%. This brought the cumulative total for the full year of 2025 to 9.04 million tonnes (mnt), representing a 2.1% rise compared to 2024.

The growth in December output was largely concentrated in China’s main ferro chrome production region of Inner Mongolia, where output climbed up by 3.7% to 682,200 t from November 2025. This growth, however, was tempered by weaker performance in the south and, so, limited the overall national gain, according to the survey.

In North China, most smelters, operating mainly to fulfil long-term contracts, sustained normal production schedules. Smelter profitability improved despite a slight dip in monthly contract prices from mills, Mysteel Global observed, as retail prices continued to edge higher.

At the end of December, Mysteel’s assessment showed that the price of 55% high-carbon ferro chrome in Inner Mongolia, the key reference price in the domestic ferro chrome market, had surged to RMB 8,100/t ($1,161/t), Cr:50%, ex-works including VAT, up RMB 100/t ($14/t) from a month earlier.

Mysteel’s latest assessments suggest that by 31 December, the average profit margin for producing HC ferro chrome among plants in Inner Mongolia using the semi-closed submerged arc furnace-electric furnace route had risen to around 6%. This is significantly higher than the previous month’s 3.9% average margin.

This favourable margin environment, combined with the ramp-up of new capacity, supported the clear output increase in the north, Mysteel Global noted.

Conversely, smelters in South China faced mounting pressure as the dry season set in, limiting the availability of hydroelectricity which forced utilities to sharply raise electricity charges, a market source noted.

Coupled with lower long-term contract prices agreed by mills, profit margins on ferro chrome were squeezed. This pressure, felt particularly acutely in Sichuan province, dampened production enthusiasm and led to a noticeable supply decline in South China.

Analysts noted that the tight spot-market supply of the ferro alloy, combined with the smelters’ healthy order books, is likely to extend the production increase into this month.

Smelters in North China are expected to maintain normal operating rates, partially to meet stronger demand from extended mill restocking for production in winter, a Shanghai-based analyst said.

“The ramp-up of new smelting projects will also contribute to the output increase,” she added.

A key development for January is the pricing benchmark set by Tsingshan Group, China’s largest stainless steel producer. Tsingshan has reduced its bid price for HC ferro chrome for January delivery by RMB 200/t ($29), nominating this at RMB 8,195/t ($1,175/t) (50% Cr basis), or $1,166/t, including tax, the company announced in late December.

Industry views suggest this settled price is better than earlier market expectations and could potentially provide a floor for market sentiment.

While some high-cost smelters in the south may continue to curb production, the impact of any reductions on the national output total is projected to be limited.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply