- China, DRC account for 56% of global refined copper output

- India witnesses steady growth post Adani refinery ramp-up

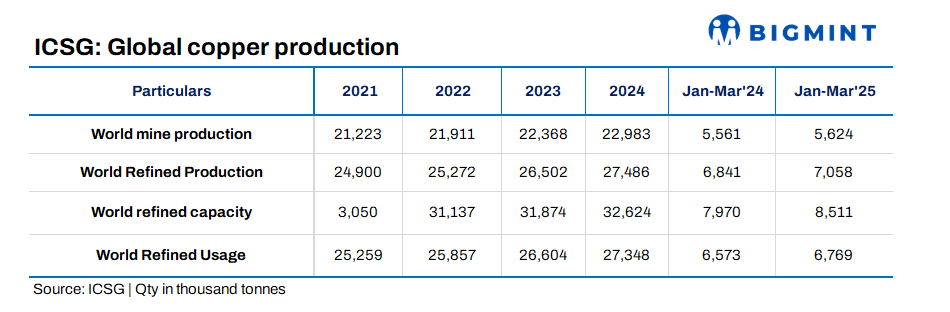

The International Copper Study Group (ICSG) has released preliminary data for the first quarter of 2025, showing that global refined copper production increased by about 3% y-o-y. This included a 3% rise in primary production (from ores via electrolytic and electrowinning processes) and a 3.5% increase in secondary production (from scrap).

The growth was largely driven by improved production in China and the Democratic Republic of Congo (DRC), which together accounted for around 56% of global refined copper output during the period. China’s refined copper production rose by approximately 4.3% y-o-y, supported by ongoing capacity expansions, while the DRC also posted a 4.3% increase, mainly due to the ramp-up of the Kamoa mine and improved operational efficiencies.

Consequently, the market surplus also widened by 7.8% y-o-y to 289,000 t in Q1CY’25.

Regional trends in refined copper production

Chile’s refined copper production declined by 11% y-o-y in the first quarter of 2025, with electrolytic output down by 22% due to smelter maintenance and SX-EW output falling by 5.5%.

In Asia (excluding China), output increased by 5.5%, with India showing steady growth following the ramp-up of Adani’s refinery, which has strengthened the country’s position in the regional copper supply landscape. However, Japan’s production fell by 5%. Additionally, Indonesia’s new smelter projects also experienced delays, with major start-ups now expected later in the year.

Refined copper usage trends, market balance

Global apparent copper usage rose by 3% in Q1CY’25, with China’s demand increasing by 4.5%. Outside China, usage rose modestly, supported by strength in Asia and MENA, although demand remained weak in the EU, Japan, and the US.

The global refined copper market recorded a surplus of 289,000 t, rising to 327,000 t after adjusting for bonded warehouse stocks in China.

Copper market posts surplus; inventories surge across exchanges

The preliminary world refined copper balance indicated an apparent surplus of about 289,000 t in the first three months of 2025, compared to a surplus of about 268,000 t in the same period last year. When adjusted for estimated changes in Chinese bonded stocks, the surplus rises to 327,000 t. China’s bonded stocks increased by approximately 38,000 t during the quarter.

As of end-April 2025, total copper stocks at the LME, COMEX, and SHFE stood at 419,955 t, down 2.4% from December 2024, with declines at the LME and increases at COMEX and SHFE.

Copper prices

The average LME cash price for April was $9,100.08/t, down 6.5% from the March average of $9,731.67/t. The highest price so far in 2025 was $9,982/t on 25 March, while the lowest was $8,539/t on 9 April. The year-to-date average stands at $9,336.19/t, which is 2.1% higher than the 2024 annual average.

Leave a Reply