- Demand weakens as mills turn to more affordable iron ore

- Production to halt at Sao Luis plant in Q3 amid maintenance

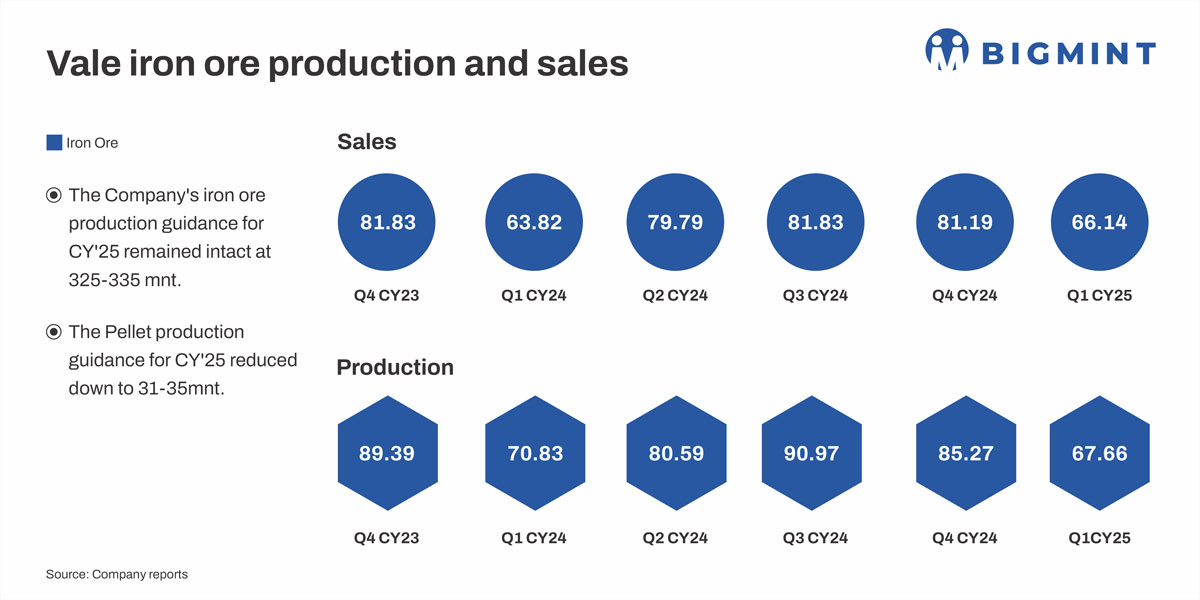

Brazilian miner Vale has reduced its 2025 production forecast for iron ore agglomerates (pellets and briquettes) to 31-35 million tonnes (mnt), from the previous range of 38-42 mnt, driven by a subdued market.

Market-driven revision

The firm’s decision to reduce its 2025 pellet production forecast was primarily driven by weaker market conditions in the pellet segment, which remains a key component of iron and steel industry demand. With steelmakers increasingly favouring lower-grade, more affordable iron ore over high-cost pellets, producers such as Vale have been adjusting their strategies by shifting focus towards fines sales to achieve cost optimisation.

Compounding the pressure is the ramp-up in output by Samarco – a joint venture between Vale and BHP – which is set to add approximately 8 mnt of pellets to the market, further intensifying supply-side competition. As per reports, Vale’s revised forecast marks a 7 mnt cut, equivalent to around 6% of the global seaborne pellet supply, which could potentially support pricing for other producers such as Rio Tinto.

Operational tactics: Pre-emptive maintenance

Vale is undertaking preventive maintenance at its Sao Luis pelletising plant, resulting in a planned production halt in the third quarter – one of the key factors contributing to the overall reduction in output. The timing of this maintenance aligns with current market softness in the pellet segment, allowing the company to limit financial impact while ensuring operational reliability.

Broader context: Vale’s strategy, market tailwinds

Vale continues to highlight its portfolio flexibility, leveraging its ability to shift between different product types – such as agglomerates and standard iron ores – depending on prevailing market dynamics. The strategy of prioritising margins over volume is being reinforced through an adaptable product approach, with the recent output adjustment seen as a move to sustain profitability amid volatile market conditions.

Outlook:

In the short term, the reduction in pellet supply is expected to tighten market premiums and lend temporary support to agglomerate prices. However, as Vale completes planned maintenance activities in the third quarter, a rebound in pellet output is likely in Q4, which could ease some of the supply-side pressure. Looking ahead, major producers such as Vale, Rio Tinto, and BHP are expected to remain vigilant amid ongoing shifts in the pellet market, including signs of oversupply, demand fragility, and price volatility. As per reports, the recalibration of supply and demand dynamics could lead to improved pellet premiums for producers.

Leave a Reply