- BF rebar trade prices drop INR 500/t w-o-w

- Need-based buying across markets weighs on prices

- HRC market under pressure despite safeguard support

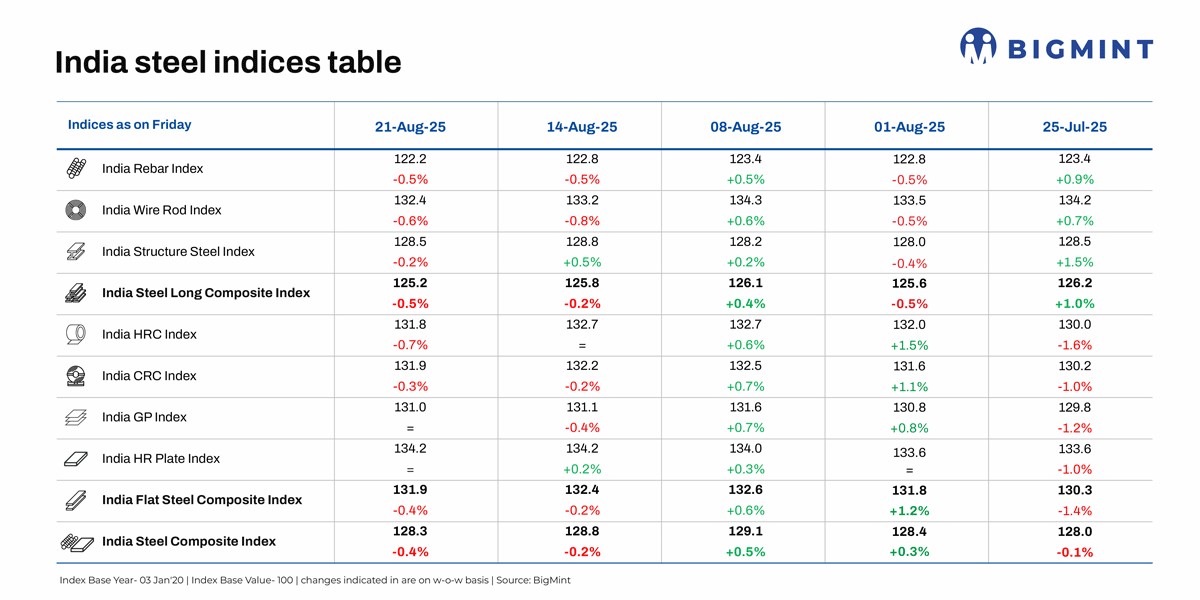

Morning Brief: BigMint’s flagship India steel composite index, which mirrors price movements in the domestic market, continued to edge lower w-o-w on 21 August 2025, dropping by 0.4% w-o-w, as per the latest assessment. Steel prices continued to weaken as vast swathes of the country battled monsoon blues and trade sentiment remained muted.

Both long and flat steel prices softened. While the longs composite index dropped by 0.5% w-o-w, the flats index fell 0.4%. Prices of semis and metallics, too, inched down w-o-w. This bearish scenario prevails even as global steel production and demand show persistent weakness.

Steel price movements

BF rebar prices edge down: Trade-level blast furnace (BF) rebar prices declined w-o-w across major markets amid demand slowdown due to rains which dampened sentiments. Trade-level BF rebar prices dropped by INR 500/t ($6/t) w-o-w to INR 47,900/t ($548/t) exy-Mumbai on 22 August. Prices are exclusive of GST at 18%.

In the projects segment, prices fell w-o-w to INR 46,500-47,500/t ($532-543/t) FOR Mumbai as buying remained entirely need-based. Heavy rains in many parts of the country led to logistical bottlenecks and supply chain disruptions.

Some primary mills reduced rebar list prices by INR 1,000/t ($12/t), while the others offered discounts due to slow lifting of material. Rebar inventories with primary mills dropped slightly to 0.47-0.48 mnt, as per sources.

IF rebar prices drop in most markets: India’s IF route finished steel market activity remained subdued last week, as weak market sentiment and a decline in inquiries led to sluggish order bookings. To liquidate inventories, manufacturers were pressured to reduce offers. Inventory levels were reportedly at 10-12 days, and market players expect prices to remain under pressure in the near term due to muted construction activity during monsoon.

On a weekly basis, rebar prices dropped in the range of INR 100-1,000/t across regions except in Raipur where prices edged up by INR 200/t w-o-w, as per BigMint assessment.

HRC market under pressure: Domestic HRC prices remained stable this week although trading activity continued to be affected by monsoon rains in key markets. Demand was moderate but slightly weaker than last week, with buyers largely restricting purchases to immediate requirements.

A market participant informed that distributors were focused on maintaining sales momentum and preferred closing deals rather than risking loss of customers. According to another participant, “Demand recovery is still awaited, with activity yet to show clear signs of improvement”.

Many buyers are beginning to recognise that trade remedial measures such as safeguard and anti-dumping duties could shape pricing dynamics in the mid to long term.

Safeguard duty: The DGTR has recommended staggered duties of 11-12% on imports of alloy and non-alloy flat steel products for three years. The investigation, initiated in 2024, established that rising imports were causing serious injury to domestic producers and safeguard duties were required to provide relief.

India’s imports of bulk HRCs have witnessed a sharp decline since mid-July and are expected to drop further as protective trade measures take effect.

Outlook

Domestic steel prices are likely to remain rangebound as monsoon continues to weigh on trade activity. Demand is yet to show signs of recovery but could improve from early September if weather-related disruptions ease. The usual surge in economic activity and construction demand ahead of the Navratri festive season beginning late-September this year is expected to boost steel market sentiment.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply