- Oversupply, high inventory weigh on HRC prices

- Revised GST on auto, construction to augment steel demand

- Export duty on iron ore may pressure steel prices further

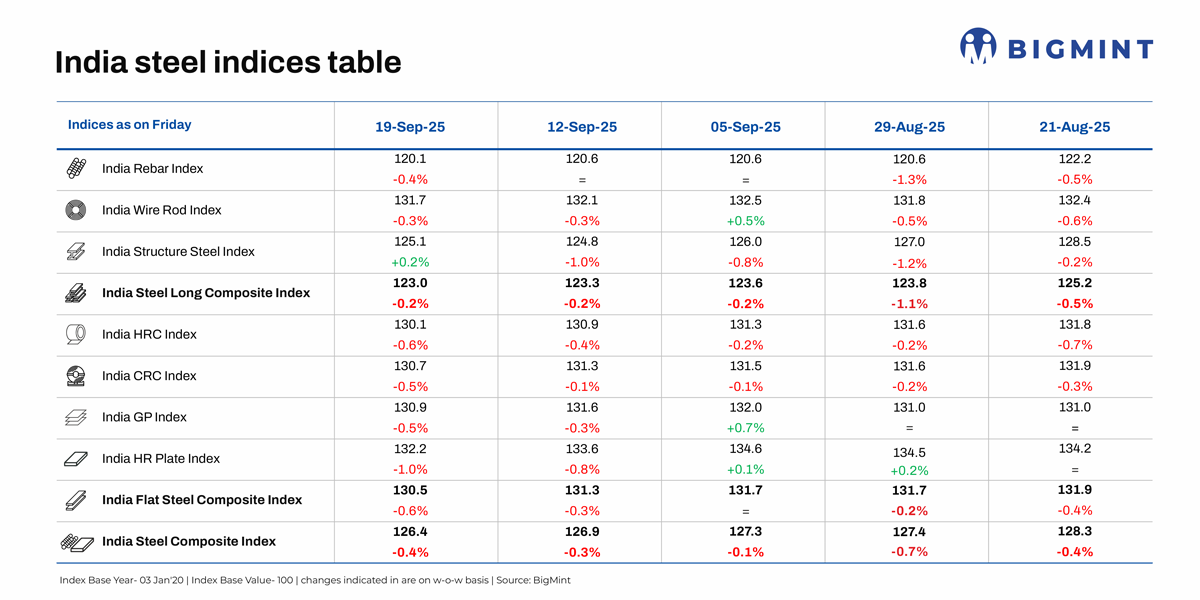

Morning Brief: BigMint’s India steel composite index, a barometer of the domestic steel market, continued to hover at multi-year lows in mid-September 2025 due to several factors, but mainly an extended monsoon and its impact on economic activities, particularly construction and infrastructure, and weak global sentiments even in China’s ‘peak’ construction season. However, domestic iron ore prices have been firm leading to erosion in steel mill margins.

Notably, in a trend reversal of sorts, the flats composite index declined a sharper 0.6% w-o-w compared with the 0.2% drop in the longs index. That this is despite the sharp decline in steel imports in August goes to show that internal demand-supply pressure is weighing on domestic flat steel prices.

Highlights of price movements

HRC, CRC prices drop: BigMint’s benchmark assessment for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) decreased by INR 300/t ($3/t) w-o-w to INR 49,200/t ($559/t) on 16 September 2025 against INR 49,500/t ($562/t) on 9 September. Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices declined by INR 400/t ($5/t) w-o-w to INR 56,100/t ($637/t) against INR 56,500/t ($642/t) a week ago. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

HRC market sentiment stayed muted as sluggish demand, oversupply and ample inventories pressured prices. Market participants informed that high stocks and thin margins kept trading slow, while the expected pre-festive pickup in demand has not yet materialised, leaving overall sentiment quite uncertain.

“Market participants anticipated a demand uptick ahead of the festive season and potential GST reduction. However, this has not played out, with buyers resisting price hikes. Persistent rainfall and flood-like conditions across several regions have disrupted construction activity, further weighing on demand. The market now remains cautious, awaiting clearer signals on how conditions will evolve,” a market participant said.

HRC export index edges down: BigMint’s India hot-rolled coil (HRC, S275 for Europe) export index dropped by $5/t w-o-w to $545/t (FOB main port) amid cautious market sentiments. While domestic demand in the EU continues to face challenges, Indian mills are pushing to complete their export quotas ahead of CBAM implementation in January 2026.

BF rebar prices see marginal decline: Trade-level BF rebar prices edged down by INR 200/t ($2/t) w-o-w to INR 47,000/t ($533/t) exy-Mumbai, as per BigMint’s assessment on 19 September. Prices are exclusive of GST at 18%. Heavy seasonal downpours in different regions and liquidity crunch affected market sentiments.

India’s induction furnace (IF) rebar prices showed mixed trends w-o-w, with buying activity largely confined to immediate requirements varying by region. In the latter half of the week, manufacturers raised prices and secured moderate bookings. Sellers continued to adjust trade discounts based on prior bookings and payment terms. Given the current market conditions, prices are expected to remain rangebound in the near term.

Outlook

Indian steel prices will most likely remain rangebound in the near term, with a slight rebound expected during the festive season. Flat steel export offers are expected to stay under pressure in the short term, driven by cautious market sentiment and the approaching CBAM. This will be a drag on domestic prices, too. However, GST rate rationalisation, which kicks in from today, especially in key downstream sectors is expected to boost steel demand.

Longs prices, on the other hand, have been weighed down by need-based buying in the market amid monsoon disruption. The potential export duty on iron ore may lead to a correction in raw material prices and offer some relief to domestic steel producers. But any such duty is likely to pile further pressure on domestic steel prices.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply