- Subdued demand drags down BF, IF rebar prices

- Labour shortages, liquidity crunch impact HRC tags

- Monsoon-led demand lull to keep near term bearish

Morning Brief: Indian steel prices weakened across the board last week, with the onset of the southwest monsoon curtailing demand from key sectors such as construction.

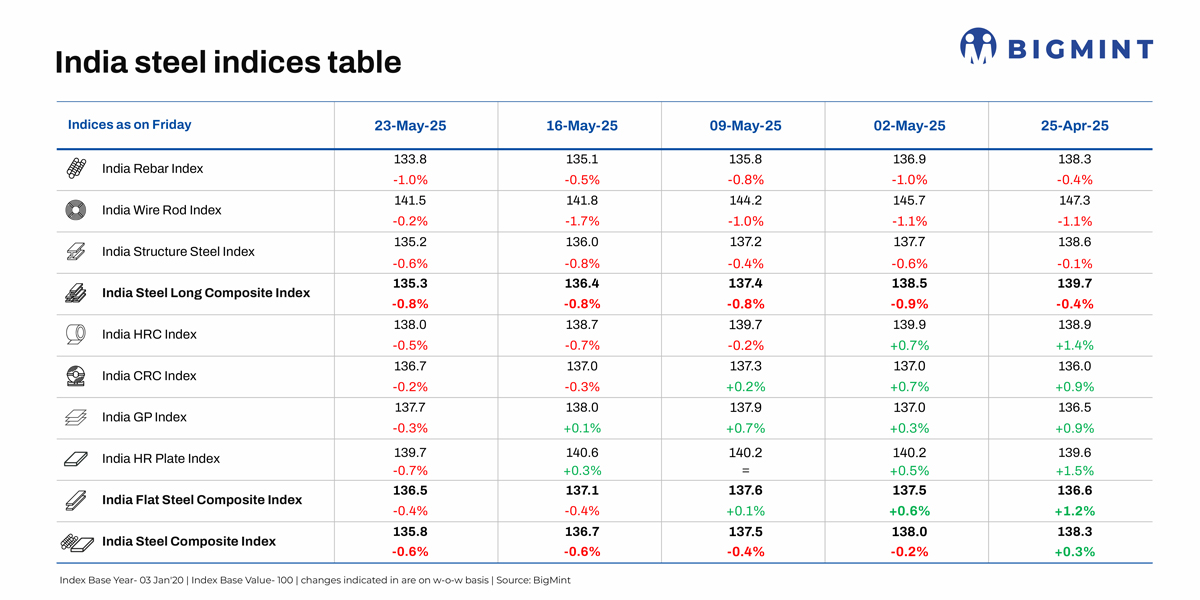

In tandem, BigMint’s India Steel Composite Index dropped 0.6% w-o-w to 135.8 points on 23 May 2025, the fourth consecutive week of decline. All the sub-indices fell w-o-w, with the steepest fall of 1% w-o-w recorded in the rebar segment. Overall, longs was down by 0.8%, while flats prices eroded 0.4% w-o-w.

Factors impacting index last week

BF rebar prices drop w-o-w: Trade-level blast furnace (BF) rebar prices declined w-o-w across markets, with benchmark tags down by INR 400/tonne (t) ($5/t) w-o-w to INR 56,000/t ($567/t) exy-Mumbai, excluding GST, on 23 May.

Pre-monsoon showers hindered construction activity in several regions, leading to dull demand and cautious trading sentiment. Lower raw material costs and uncertainty regarding future pricing trends also led to a drop in BF rebar tags.

The projects segment mirrored these conditions, with prices falling w-o-w to around INR 54,000-55,000/t ($633-645/t) FOR Mumbai amid need-based trade activities.

IF rebar trade prices decline w-o-w: Induction furnace (IF) rebar trade prices declined w-o-w, with Mumbai recording a drop of INR 400/t ($5/t) w-o-w to INR 47,500/t ($557/t) exw on 23 May.

Prices were weighed down by need-based trade, limited inquiries, and high inventory pressure, with the average holding time at around 10-12 days.

HRC prices edge down w-o-w: Trade prices of hot-rolled coils (HRCs) fell w-o-w, with benchmark values down by INR 200/t ($2/t) to INR 51,800/t ($608/t) on 23 May exy-Mumbai, excluding 18% GST.

Cold-rolled coil (CRC) tags fluctuated across key clusters, but they were down by INR 300/t ($4/t) w-o-w in Mumbai to INR 58,500/t ($687t) exy, excluding 18% GST.

Demand softened due to the approaching monsoon, with CRC suppliers under increased pressure to offload inventory in expectation of the storage and logistical challenges that generally occur due to the monsoon. Other factors that weighed on trade sentiment were labour shortages (due to many workers shifting to agricultural activities), liquidity constraints, and market participants’ hopes of more favourable pricing in the coming days.

On the imports front, the arrival of bulk HRCs and plates touched 171,834 t as of 19 May, based on vessel line-up data from BigMint. Around 24,238 t of additional cargo are expected by May-end. In comparison, imports totalled 306,260 t in April and 408,762 t in March.

HRC export offers decline: India’s HRC export offers to the EU dropped by $10/t w-o-w to $630-635/t CFR Antwerp, amid muted trade activity and competitive offers from Southeast Asian mills. Expectations are that the bearish sentiment will remain, with European buyers continuing to prefer domestic HRCs due to faster delivery timelines.

Indian steelmakers remained focused on the domestic market, where they are securing better price realisations. Offers to the Middle East continued to be on pause.

Outlook

The steel market’s bearish tendencies are expected to persist, given that the monsoon has arrived – eight days ahead of schedule, in fact.

While heavy rainfall and labour shortages will slow down construction activity, liquidity issues are expected to persist, due to which trading activity may continue to lose steam. Buyers expect further price corrections or support from mills, and until tags fall to a favourable level, demand may remain subdued.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply