- Mills reduce BF-rebar prices by INR 1,000-3,000/t, IF steel prices weaken too

- Tier-1 steelmakers cut HRC list prices by INR 1,000/t for Jul’26, trade prices soften

- Bulk HRC imports fall sharply in June but finished steel imports rise marginally

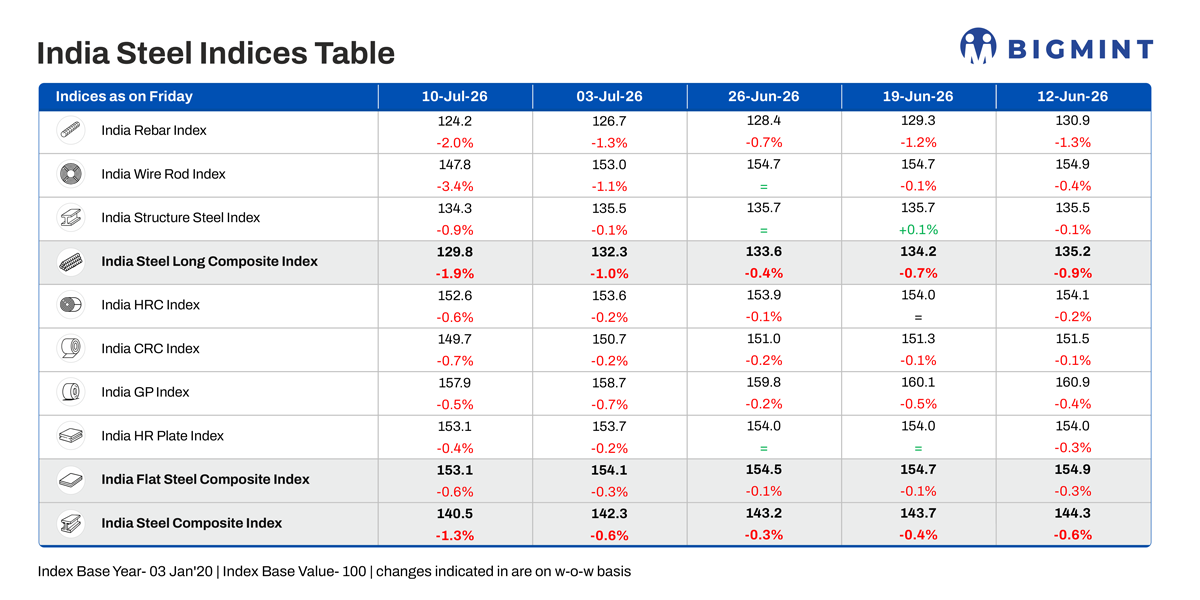

Morning Brief: BigMint’s India steel composite index, a barometer of the domestic market, edged down by 1.3% w-o-w, as assessed on the week ended 10 July 2026, with domestic prices deteriorating further with the onset of monsoon in different parts of the country, inevitable disruptions in infrastructure and construction activities, and fast-accumulating inventories at mills and at the distributor level.

Notably, long steel prices corrected sharply, while flats showed a slower pace of decline: over the past month the rebar index dropped around 6.5 percentage points compared with 1.1 percentage points for HRC. W-o-w, the rebar index slipped 2% while HRC dropped 0.6%. The composite index declined to the lowest level in six months last week as the major domestic mills announced a reduction in list prices of both long and flat products.

Highlights of price movements

Tier-1 mills trim BF-rebar list prices: BigMint’s benchmark assessment for rebar (IS 1786 Fe 550D, 12–32 mm, BF route) stood at INR 49,000/t as of 10 July, down by INR 800/t from INR 49,800/t recorded on 3 July. Prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

India’s tier-1 blast furnace (BF) steel producers reduced rebar list prices for July deliveries by INR 1,000-3,000/t m-o-m as weak buying enquiries, rising inventories, and slow construction activity weighed on market sentiment. The price correction followed sluggish procurement by distributors, limited project bookings, and increasing inventories across the supply chain.

Rebar inventories at primary mills increased by around 20% m-o-m as fresh order bookings weakened. With most previously secured project-linked orders have already been executed, mills were left with thinner order books and reduced backlog visibility heading into July. Some mills offered higher discounts to liquidate inventory, which intensified price competition in the BF-route rebar segment.

IF rebar records weekly decline: IF-route rebar prices declined by INR 100-1,900/t w-o-w on moderate demand and weaker billet and sponge iron prices. Trading remained need-based, with mills reducing prices in the latter half of June to stimulate enquiries. Consequently, mill inventory levels declined to around 12 days from nearly 15 earlier in June. The price differential between BF-route and IF-route rebars narrowed to around INR 4,000/t during June, reducing the pricing premium enjoyed by primary producers.

HRC, CRC prices weaken: BigMint’s benchmark assessment for HRC (IS 2062, Gr E250, 2.5–8 mm/CTL) stood at INR 57,900/t on 10 July, down by INR 300/t from INR 58,200/t recorded on 26 June. The benchmark assessment for CRC (IS 513, Gr O, 0.9 mm/CTL) stood at INR 65,000/t, down INR 200/t from INR 65,200/t during the same period. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

The leading steelmakers reduced their flat steel list prices by INR 1,000/t for July deliveries, reducing both HRC and CRC prices amid subdued market activity and cautious buying sentiment. India’s manufacturing purchasing managers’ index eased to 54.2 in June 2026, reflecting slower expansion, with weaker growth in both new orders and output.

The onset of monsoons further impacted consumption by slowing construction and infrastructure activity. In addition, distributors entered July with comfortable inventory levels following earlier restocking, reducing the urgency for fresh procurement. Collectively, these factors outweighed cost-side support and prompted mills to reduce list prices.

In addition to this NMDC reduced prices on 10 July. Prices of DR CLO (10-40 mm, Fe 67%) were at INR 5,850/t ($61/t) and of iron ore fines (-10 mm, Fe 64%) at INR 4,700/t ($49/t). Prices of all grades were reduced in the range of INR 150-500/t for July.

HRC imports drop in June: Bulk HRC imports declined sharply to 247,754 t in June, down 42% m-o-m from 423,925 t in May, reducing competitive pressure from overseas material. This was despite the fact that finished steel imports increased by 1% m-o-m in June to 0.696 mnt.

The sustained inflow of imports was supported by competitively priced cargoes booked earlier and continued arrivals under long-term contractual arrangements. Demand from export-oriented downstream manufacturers also contributed to imports.

However, the DGTR’s anti-dumping investigation into HRC imports from China, Japan, and Russia is expected to reshape India’s import market in the coming months. The initiation of the probe, along with the possibility of retrospective anti-dumping duties sought by domestic steelmakers, has made importers increasingly cautious about placing fresh orders. This comes at a time when imported HRC is already significantly more expensive than domestic material due to the existing 11.5% safeguard duty and higher landed costs, reducing the commercial attractiveness of imports.

HRC export prices soften further: Bulk HRC exports stood at 235,773 t in June, up 71% y-o-y, driven by higher shipments to Vietnam on strong manufacturing demand, competitive pricing, and increased trade restrictions on Chinese steel. Weak domestic demand in India also prompted mills to divert higher volumes to export markets, although shipments to the EU remained constrained by safeguard quota limits.

Cautious buying sentiment in key export destinations continued to weigh on trading activity. HRC export offers to the EU declined by $10/t w-o-w to around $590/t FOB amid lack of buying interest from European buyers, with no fresh bookings reported during the assessment period. While the introduction of country-wise quota allocations has removed much of the previous uncertainty, it has not translated into a meaningful improvement in market sentiment, sources said.

Likewise, offers to the Middle East and Vietnam also dropped $5-15/t w-o-w on declining Chinese offers and softening buying interest.

Outlook

India’s crude steel production remained flat in June while finished steel production fell marginally. However, consumption increased by over 7% on the year on sound infra and construction fundamentals. The underlying momentum in the steel market is supported by healthy consumption trends. Additionally, India awarded as many as 60 infrastructure projects in June which will commence operations post weather-related disruptions. Therefore, the fundamentals remain strong.

The cyclical downturn is due to seasonal factors, increased inventories, and eroding cost support amid stabilisation in freight and fuel prices, although renewed geopolitical unrest in the Middle East might reverse the situation anytime. BigMint notes that steel prices are likely to trend lower in July on monsoon blues and inventory pressure.

Leave a Reply