- Rebar prices fall on muted demand, lower mill offers

- Tight liquidity, price resistance drag down HRC tags

- Indian importers procure Russian HRCs after long gap

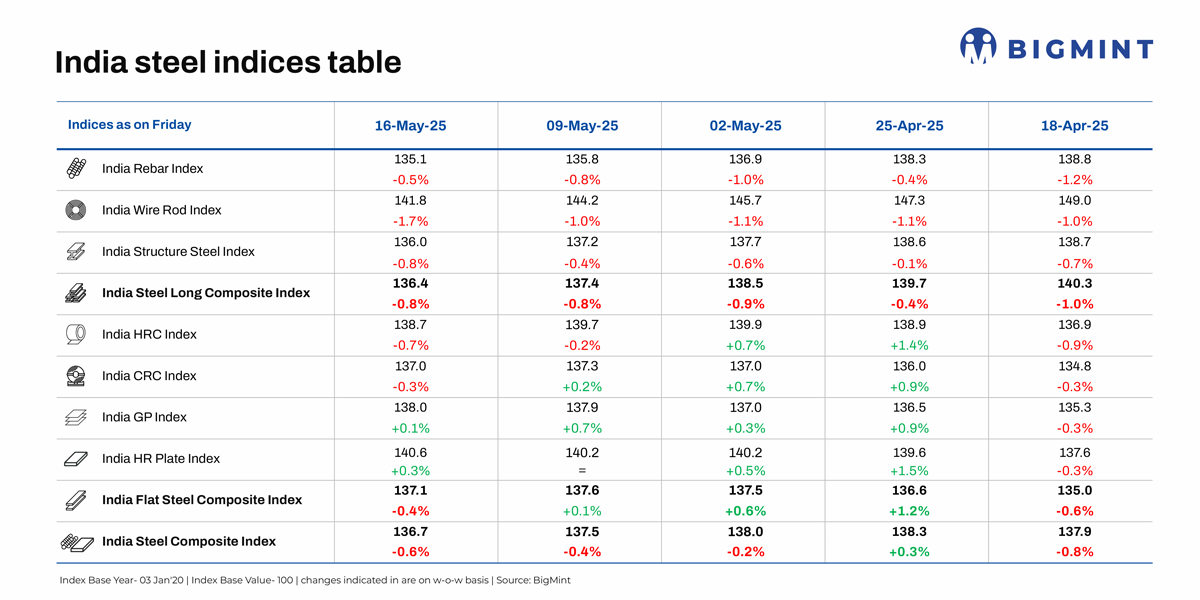

Morning Brief: BigMint’s India Steel Composite Index declined for the third consecutive week on 16 May 2025, as bearish demand continued. The index dipped by 0.6% w-o-w to settle at 136.7 points, a two-month low.

The longs index dropped 0.8% w-o-w, while flats fell a more modest 0.4%, buoyed by slight hikes in HR plates and galvanised plain (GP) coils. Among longs, the wire rod index witnessed the sharpest drop of 1.7%.

Factors impacting index last week

BF rebar drops on muted demand, list price cuts: Trade-level BF rebar prices declined across markets, with Mumbai witnessing a drop of INR 300/tonne (t) ($4/t) w-o-w to INR 56,400/t ($659/t) exy, excluding 18% GST, on 16 May 2025.

The drop in trade prices was prompted by two factors: First, there was subdued demand, with most buyers staying on the sidelines amid market uncertainty. Second, some leading steelmakers reduced their list prices to INR 55,500-56,000/t ($648-654/t) on landed basis, as per sources.

Projects prices also dropped w-o-w to INR 54,500-55,500/t ($637-648/t) FOR Mumbai amid bid-offer disparities and need-based buying amid expectations of further price drops.

Sluggish trades pull down IF rebar prices: Induction furnace (IF) rebar trade prices fell w-o-w amid need-based buying and limited inquiries. In Mumbai, prices dropped by INR 100/t ($1/t) w-o-w to INR 47,900/t ($560/t) exw on 16 May 2025.

In addition to weak demand, two other factors led to lower prices: First, inventory pressure on mills increased, with holding time at around 10-12 days. Secondly, manufacturers reduced their offers to stimulate trade. However, amid uncertainty over future trends, retailers remained cautious and avoided bulk bookings.

HRC prices decline due to tepid demand, tight liquidity: Trade-level prices of hot-rolled coils (HRCs) fell across markets amid lacklustre demand and tight liquidity conditions. BigMint assessed HRCs at INR 52,000/t ($607/t) ex-Mumbai, excluding 18% GST, down by INR 400/t ($5/t) w-o-w on 16 May 2025.

Additionally, cold-rolled coil (CRC) prices fell by INR 800/t ($9/t) w-o-w to INR 58,800/t ($688/t) ex-Mumbai, excluding 18% GST.

Buyers continued to resist prevailing prices, deeming them too high and procuring only enough to fulfil immediate needs.

Additionally, with a liquidity crunch prevailing, most new sales were on credit, and payment recovery remained slow.

However, reduced supply, due to production cuts at leading steelmakers and lower imports, helped limit a larger price drop.

Concerns emerge about HRC imports: India’s bulk imports of HRCs and plates for this month totalled 70,025 t on 12 May, based on vessel line-up data from BigMint. The same stood at 306,260 t in April and 408,762 t in March.

While HRC/plate imports have continued to fall in recent months, some concerns have emerged recently, given that current domestic prices are higher than imported tags. Recently, some importers booked 35,000-40,000 t of HRCs from Russia at $460-470/t CFR for June shipment, sources informed BigMint.

Considering the customs duty, a 12% safeguard duty, along with port handling and miscellaneous charges, the landed cost of Russian HRCs would be at around INR 50,500-51,000/t ($590-596/t), slightly lower than the current trade prices of INR 52,000/t ($607/t) ex-Mumbai assessed on 16 May. Moreover, leading steel mills’ list prices of HRCs (2.5-8 mm, IS2062, Gr E250, Br.) were at INR 53,000-54,000/t ($619-631/t) ex-Mumbai.

Notably, this marks the re-entry of Russian exporters into the Indian market after a sizeable gap. Russian offers were also lower than Chinese ones, which were priced at around $480-485/t CFR India

The Russian mills in question, as per sources, also possess the required Bureau of Indian Standards (BIS) certifications to export steel to India.

HRC export offers to EU drop amid muted sentiments: Indian HRC export offers to the EU dropped by $5/t w-o-w to $640-645/t CFR Antwerp, amid sluggish trade activities as domestic mills quoted lower prices. Additionally, Indian steel mills did not actively offer to the Middle East market, amid competitive offers from China.

Notably, Indian steel mills are focused on the domestic market, where they are achieving higher realisations.

Outlook

While optimism around the safeguard duty had led to a spike in steel prices, it is evident that the bullish momentum has dissipated, and steel prices will continue to be subdued. Buyers remain cautious about current pricing, and there are no signs of a strong rebound in demand. Notably, the monsoon will arrive next month, so demand may soften even further.

However, the near term is unlikely to see a sharp drop, with supply constraints continuing due to maintenance shutdowns at two leading steelmakers. Overall, price movements may be limited to a narrow range in the days ahead.

Leave a Reply