- Mills roll over HRC list prices despite surging coking coal prices

- Tier-1 mills reduce BF rebar prices, IF prices touch 4-month low

- Price gap with landed HRC imports from China at over INR 7,000/t

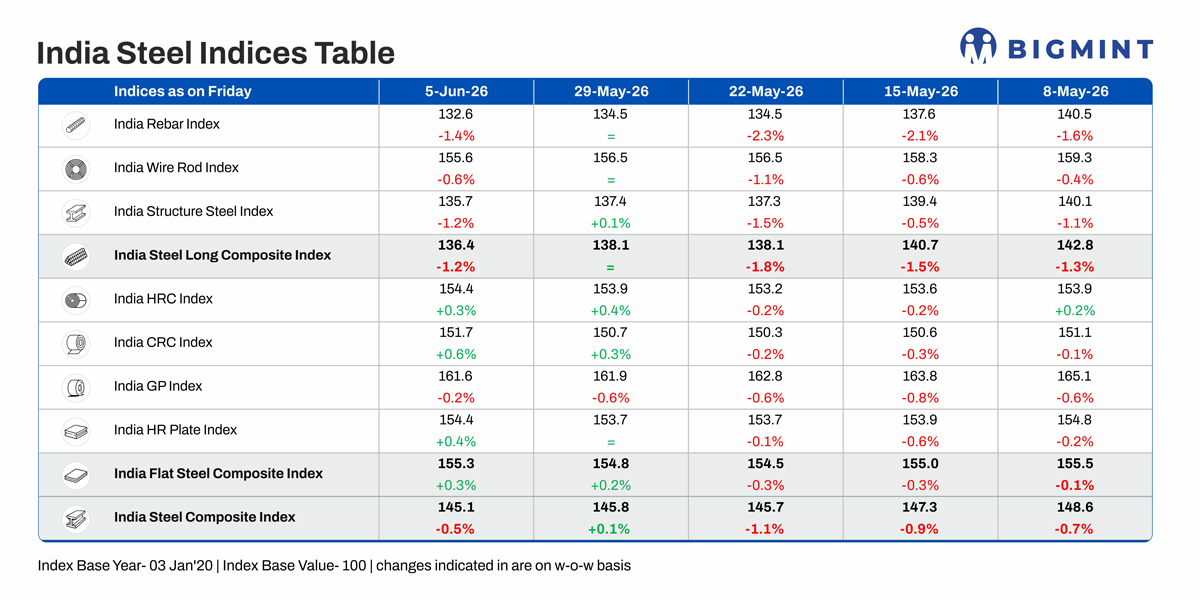

Morning Brief: BigMint’s flagship India steel composite index reversed minor gains recorded the week before to continue its downtrend last week, dropping 0.5%, as assessed on 5 June. Domestic steel prices seem to have lost steam after geopolitical problems in the Middle East and fiscal yearend demand surge in March and early April slowly tapered off.

While production and consumption levels have remained strong, demand has softened of late due to elevated prices (thanks to the rally in March and early April), while ongoing heatwaves in many parts of the country, labour shortages and high prices have cumulatively affected construction sentiment leading to loss of demand from this key segment.

Solid manufacturing fundamentals and fresh export bookings have provided support to HRC prices, but long steel continues to decline fast on weak construction sentiment. The flats index last week rose modestly by 0.3% while the longs index fell by 1.2% w-o-w.

Highlights of price movements

HRC, CRC remain largely stable: BigMint’s benchmark assessment for HRC (IS2062, Gr E250, 2.58 mm/CTL) inched down by INR 200/t ($2/t) w-o-w to INR 58,300/t ($612/t) on 5 June against INR 58,500/t ($614/t) last week after showing mixed trends during the assessment on 2 June. However, CRC (IS513, Gr O, 0.9 mm/CTL) remained stable w-o-w at INR 65,200/t ($684/t) on 5 June. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

The leading steel mills rolled over HRC, CRC list prices for June on soft trade-level sentiment and surging imports. In north India last week, distributors attempted to raise offers to offset higher procurement costs and protect margins, supported by limited availability of certain thicknesses, which led to local supply tightness. However, other regions continued to witness adequate availability, keeping prices rangebound.

Sentiment in the market has remained guarded, as prevailing demand conditions are being seen as insufficient to support further price hikes.

Imports surge: Bulk HRC imports into India in May were 423,925 t, an increase of 21.5% m-o-m from 348,901 t in April, as per vessel line-up data. This was due to demand from pipe and tube manufacturers amid surging demand in the Middle East for pipe products following the sharp rise in global crude oil prices in the backdrop of the Iran conflict. Therefore, the over 20% monthly surge in imports can be accounted for by the fact that the domestic mills were eager to capitalise on the opportunity of channelling fresh exports to the Middle East.

Although export bookings boosted domestic HRC prices and the surge in imports forced the tier-1 mills to roll over June prices, imports hardly constitute a threat when it comes to dumping and distortion of domestic prices, thanks to the 11.5% safeguard duty in place.

While a minor drop in the duty since April encouraged importers, the price spread with landed HRC from China is assessed at around INR 7,300/t. The price differential between domestic HRC and imports from FTA countries is around INR 5,700/t.

Coking coal prices rise: BigMint’s coking coal index continued to edge up w-o-w amid supply tightness and strong coke market sentiments in China after a massive mine accident in Shanxi earlier in May threatened to curtail supplies.

Global prices are rising steadily, and a severe shortage is expected in the market. Coking coal production at the mines has declined significantly, while vessels are facing prolonged waiting times for berthing, further tightening supply. This is supporting prices and raising costs for the integrated producers in India.

IF rebar market down, primary mills cut prices: IF-route rebar prices declined by INR 1,800-4,200/t m-o-m in May on subdued market activity, weak demand, and limited order bookings. Prices fell to a four-month low. Buyers remained reluctant to accept higher offer prices and largely continued with need-based procurement. Market sentiment remained cautious, while mill inventory levels were reported at around 12-15 days.

Meanwhile, BF-route rebar steel producers reduced list prices for June deliveries. Current list prices of IS 1786 Fe 500/550D size 12-32 mm rebars at the mill-to-distributor level are in the range of INR 55,250-57,700/t exy Mumbai, reflecting a price correction in the range INR 1,000-4,000/t ($10-$42/t) compared with early May.

The price reduction was a result of weak enquiries, limited order bookings by distributors, mounting inventory pressure across the supply chain, and a widening price gap of nearly INR 10,000/t between BF-route and IF-route rebar during May.

Subdued market fundamentals, primarily slower construction activity due to the extreme heatwave, adversely impacted sentiment. Rebar inventories at primary mills increased around 35% m-o-m in May.

Outlook

NMDC has hiked iron ore prices for June while coking coal sentiment remains firm. Therefore, strong raw material prices are expected to keep steel prices rangebound this week. Moreover, mills are negotiating a firm cost environment due to increasing freight and fuel costs triggered by geopolitical conflict. The commencement of quota-based imports in the EU from July will certainly weigh on flat steel prices.

Despite soft demand at elevated price levels, pre-monsoon restocking demand is expected to prop up prices. However, fundamental weakness in construction sector demand is expected to last the entire monsoon period.

Leave a Reply