- Trade-level TMT prices drop on high inventories

- Flat steel market under pressure on domestic supply glut

- Global overcapacity, dumping risk to weigh on prices in Q4CY’25

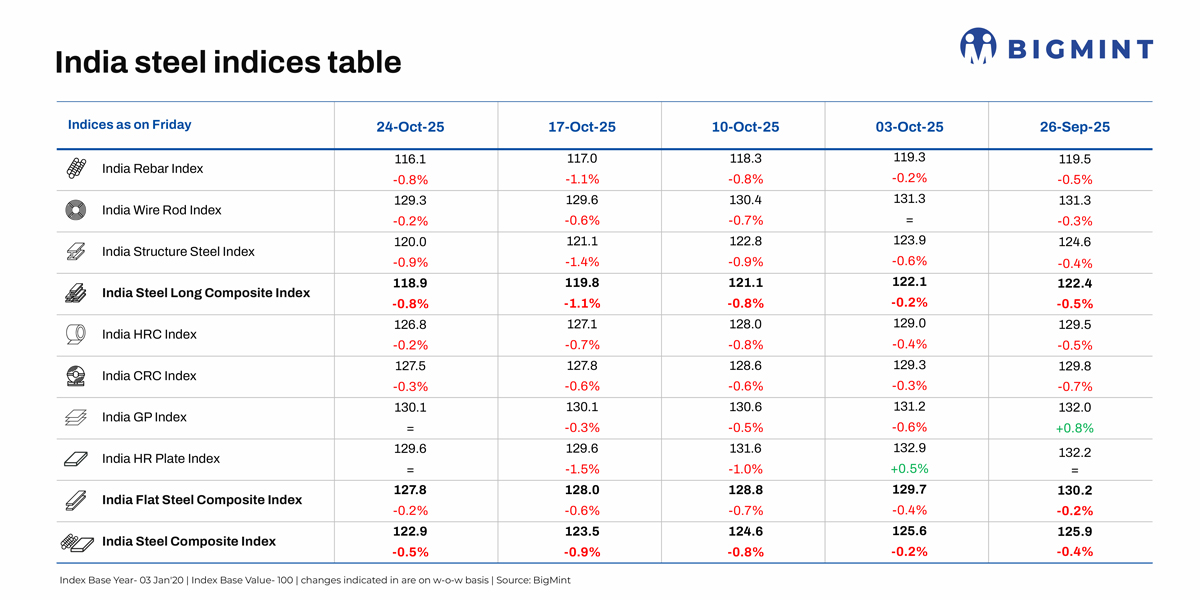

Morning Brief: BigMint’s flagship India steel composite index, a barometer of the domestic steel market, edged down by 0.5% w-o-w, as assessed on 24 October 2025. The continued downtrend, with steel prices dropping to 5-year lows, points to the combined impact of festive slowdown and inventory pressure in the domestic market.

While the finished flat steel index fell by 0.2% w-o-w, the longs index declined more sharply by 0.8% w-o-w after declining by 1.1% the previous week. In fact, the slowdown in the steel market showed no signs of abating in October, with the composite index declining by nearly 3 percentage points since the first week.

Highlights of price movements

Rebar prices edge down: Trade-level blast furnace (BF) rebar prices declined w-o-w across markets. The major primary mills either offered discounts or reduced list prices the week before Diwali due to subdued sentiment. Buying activity was weak across regions during the holiday period.

Trade-level BF rebar prices edged down by INR 100/tonne (t) w-o-w to INR 46,800/t exy-Mumbai on 24 October. Prices are exclusive of GST at 18%.

On the other hand, IF rebar prices remained stable in some major markets and declined marginally in others as trading hit a standstill during Diwali. Cautious buying and need-based purchases resulted in subdued market sentiment. Industry participants are expecting market sentiment to turn slightly positive post-Diwali, supported by the resumption of construction projects and an expected recovery in buying interest.

Flat steel price downtrend lingers: Trade-level prices of hot-rolled coils (HRCs) and cold-rolled coils in India showed a downtrend w-o-w, although the benchmark assessments remained suspended due to the Diwali holidays. However, bi-weekly assessments show that prices declined in the key markets of Kolkata, Bangalore and Hyderabad on 24 October. HRC (IS2062, Gr E250, 2.5-8 mm/CTL) had decreased by INR 300/t ($3/t) w-o-w to INR 48,000/t ($541/t) on 14 October against INR 48,300/t ($544/t) on 7 October.

CRC (IS513, Gr O, 0.9 mm/CTL) prices had inched down by INR 200/t ($2/t) to INR 55,500/t ($625/t) the week prior. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Notably, the leading manufacturers had decreased HRC and CRC prices by INR 750-1,500/t ($8-17/t) in early October as compared to the list prices of early-September. However, from the net sales prices of end-September, prices were raised by INR 500/t ($6/t) for October.

Steel distributor sources informed about low demand and few inquiries weighed on prices during the holiday period. Trade was slow because of festive season slowdown. Market participants believe activity will pick up after the festival.

Outlook

The expected pre-festive demand recovery in early October had been sluggish, with buyers remaining cautious due to high inventory levels and muted trading sentiment. The hike in construction steel prices by the Tier-1 mills failed to extend much support to the trade market. Despite over 8% growth in consumption, rapid expansion in production and capacity is weighing on prices.

The domestic market is waiting for a trend reversal after the Diwali and Chhath Puja holidays, with expectations that a rebound in demand after the festive season will prop up steel prices. However, any sharp uptick appears unlikely amid global overcapacity and dumping risks, high domestic capacity and inventories, as well as soft demand.

Leave a Reply