- Weak steel sales to cap scrap price recovery

- Year-end outlook quiet with low booking interest

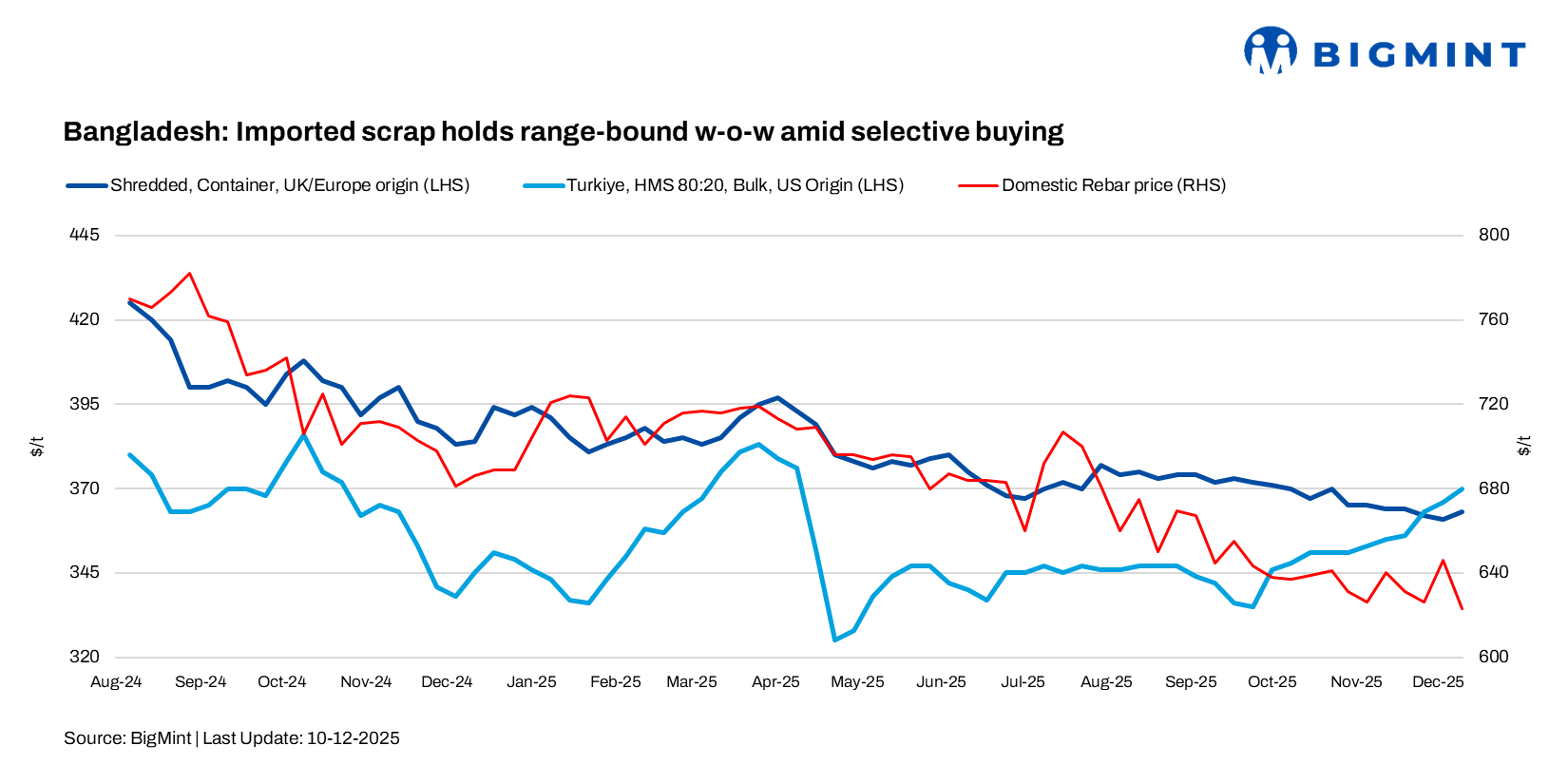

Bangladesh’s imported scrap market remained subdued, with buying interest constrained by a wide gap between bids and offers. Australian HMS and shredded mostly hovered within the $340-365/t range, though actual transactions were scarce. Singapore-origin PNS was offered at around $380/t CFR, while buyers capped bids around $365/t, limiting deal possibilities.

Bulk cargo indications included US-origin HMS 80:20 at $360/t and above CFR versus bids of $350/t. Japanese H2 was at $345-346/t CFR against bids of $338-340/t, and Chile/Brazil HMS offered at around $335/t CFR, with buyer interest around $330/t.

BigMint’s weekly assessments

- European-origin HMS (80:20) held at $341/t

- European-origin containerised shredded inched up by $2/t w-o-w to $363/t.

- Japanese-origin H2 bulk inched up by $1/t w-o-w to $342/t.

- US-origin HMS (80:20) bulk inched up $1/t w-o-w to $356/t.

Brazil HMS is at around $330/t CFR, Malaysian hollow bundles $325/t CFR, and Philippine GI bundles are at $305/t CFR, with some indications at $305-310/t before sellers paused sales.

One buyer based in Dhaka commented that suppliers were unwilling to close deals at these levels even as buyers remained active around the following indications: PNS at $355/t, shredded at $350/t, HMS 90:10 at $335/t, and HMS 80:20 at $325–330/t CFR Chattogram for Australia, New Zealand, and Singapore origins.

Domestic market

In the domestic market, billet prices were heard at BDT 63,000/t ($516/t), while rebar traded at BDT 72,000-76,000/t ($589-622/t) in Dhaka and Chattogram. Local scrap was assessed at BDT 45,000-46,000/t ($368-376/t).

As per market insiders, private-sector activity fell sharply, dropping to 40% of capacity, which significantly curtailed steel demand and made it difficult for companies to absorb overhead costs.

Chattogram’s ship-recycling market softened this week following heavy November tonnage arrivals on weaker buying interest. A declining BDT, lower steel plate prices, and the absence of new vessel arrivals further tempered sentiment. HKC-certified yards are now processing recently arrived large LDT LNG vessels, but with limited supply and cautious buying amid inflation and policy uncertainty, the market looks set for a subdued Christmas season.

Outlook

Bangladesh’s short-term outlook stays soft. Mills are buying only what they need, bids remain well below offers, and weak steel demand is keeping operations slow. Unless the BDT stabilises and local steel sales improve, scrap bookings will stay low, and the market is likely to remain quiet throughout December.

Leave a Reply