- Bulk bookings limited; containerised lots preferred

- Infrastructure hopes yet to materialise in the market price

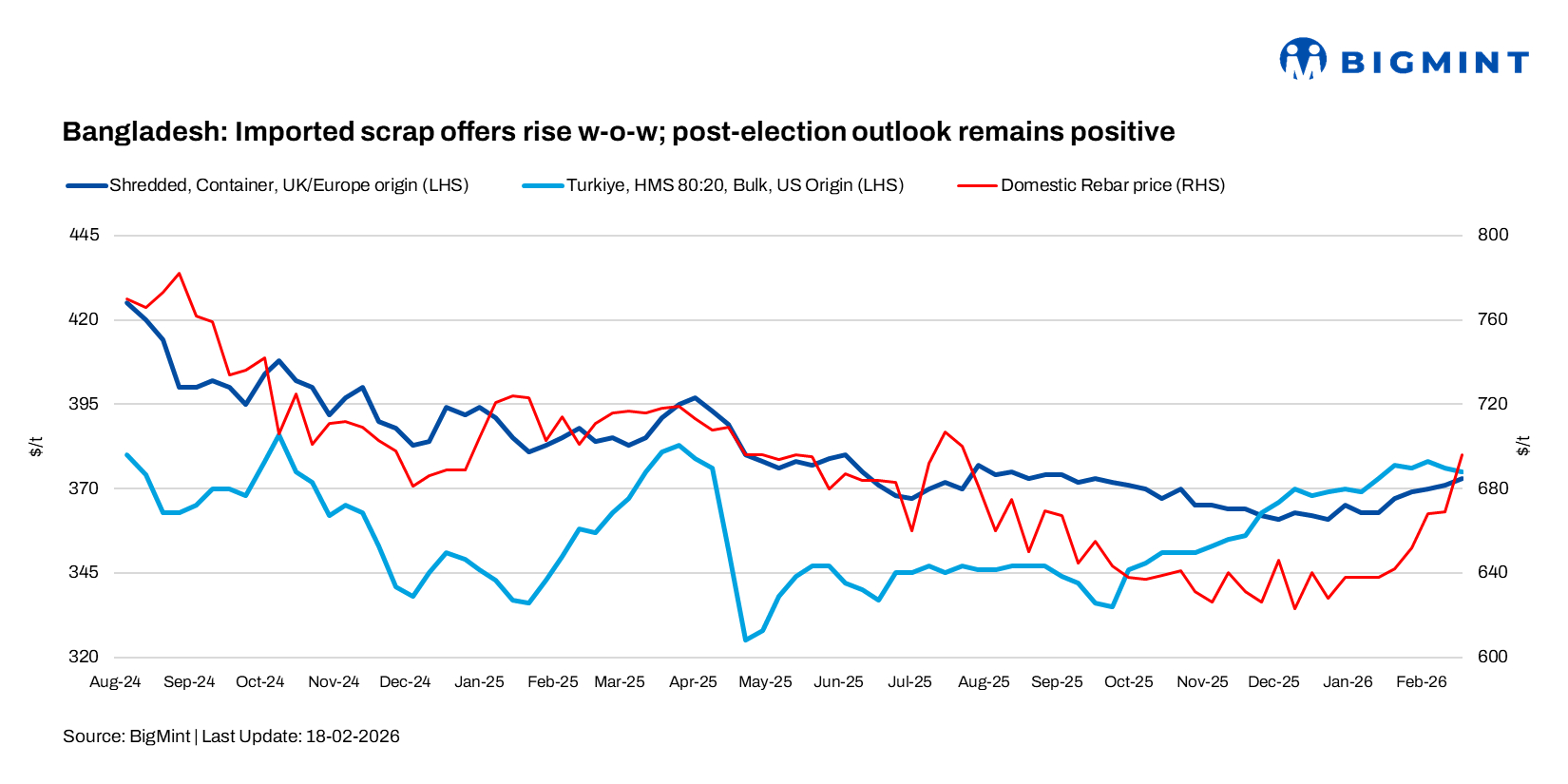

Imported ferrous scrap prices in Bangladesh showed a mixed trend in the week ended 18 February, supported by firmer containerised offers globally and tightening scrap availability. While bulk market sentiment remained cautious, selective bookings continued in containerised scrap.

Market sentiment in major regions improved following the decisive election victory of the Bangladesh Nationalist Party (BNP), raising expectations of renewed progress in stalled infrastructure projects and a gradual recovery in domestic steel consumption.

However, trading activity already remains subdued due to the Ramadan week, and overall market movement continues to stay slow.

BigMint’s weekly assessments

- European-origin HMS (80:20) assessed at $352/t, up by $1/t w-o-w.

- European-origin containerised shredded increased by $2/t w-o-w to $373/t.

- Japanese-origin H2 bulk down by $4/t w-o-w to $351/t.

- US-origin HMS (80:20) bulk rose by $2/t w-o-w at $375/t.

Market comments

An Australia-based trader indicated that the Bangladesh scrap market remains stable, with indicative CFR levels (as of 18 February) at HMS (80:20) $360/t, HMS 1 at $370/t, shredded at $380-382/t (bids at $372-375/t), and PNS at $380-385/t.

A Dhaka-based steel mill representative reported rebar prices at BDT 80,000-82,000/t ($655-671/t), with Chattogram levels about BDT 5,000/t higher at BDT 85,000/t ($696/t). Billet was heard at BDT 67,000-70,000/t ($548-573/t), while local scrap traded at BDT 51,000-54,000/t ($417-442/t). Sentiment improved around the election week on expectations of new project demand and the gradual resumption of steel production across major mills.

Although a direct translation into sustained price gains may take a few weeks, this week’s uptick was largely sentiment-driven.

Ship recycling: The adoption of the IRRC framework in line with Hong Kong Convention standards strengthened regulatory credibility.

However, fundamentals remain mixed. The Taka weakened to BDT 122.25/$, and local steel plate prices stayed flat at around $494/t for the third week. Despite this, recyclers secured several small vessels and a 24,000 LDT unit, reflecting selective buying interest.

Outlook

The market is likely to stay steady in the coming days, with post-election optimism offering some support. At the same time, pressure from the weaker currency and soft finished steel demand may prevent any sharp rise. With Ramadan underway, activity is expected to remain slow, and prices will largely depend on need-based buying rather than aggressive restocking.

Leave a Reply