- Bulk offers scarce; buyers remain conservative

- Stagnant rebar prices weigh on import scrap prices

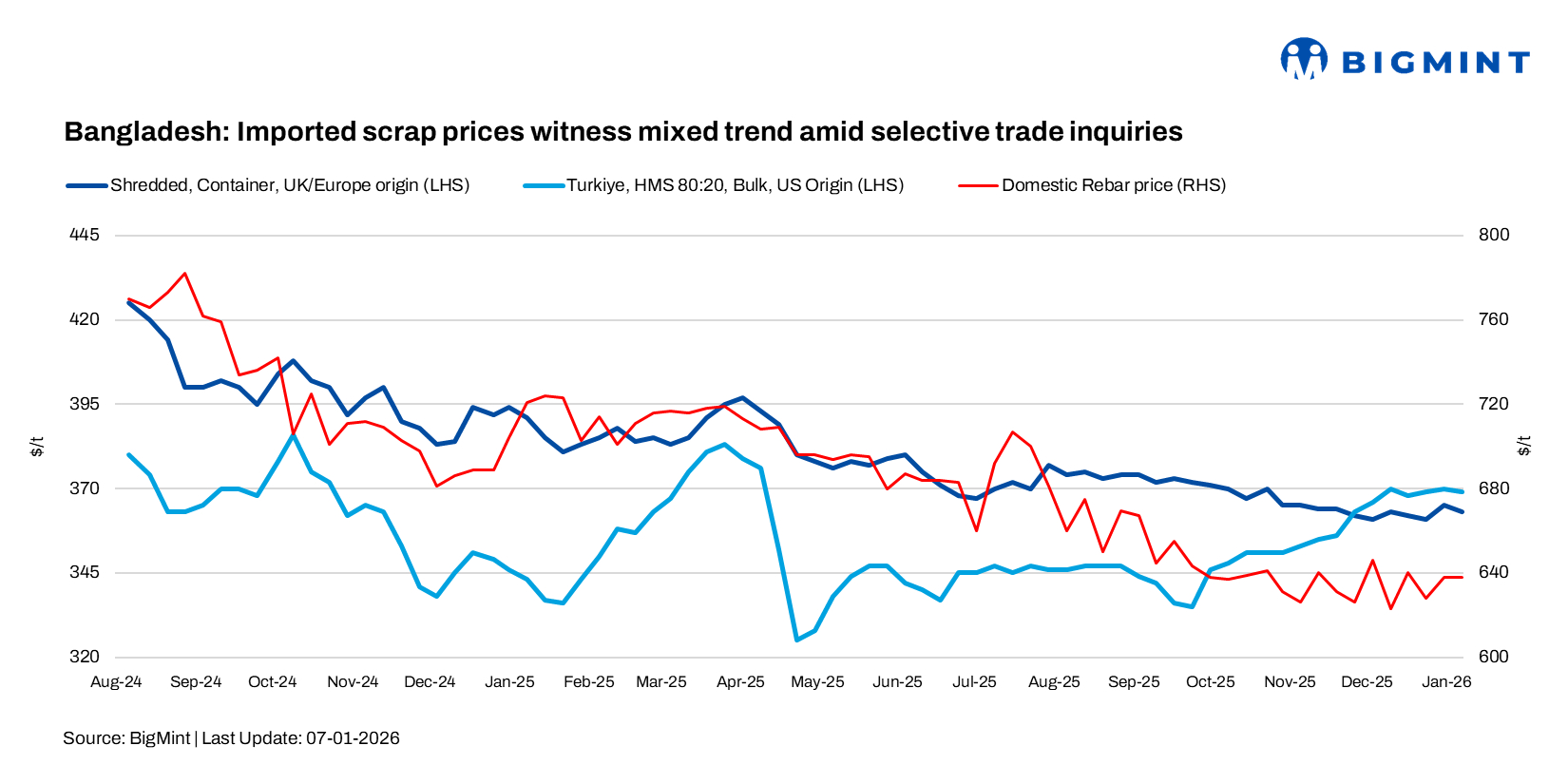

Bangladesh’s imported scrap prices showed a mixed trend w-o-w, as assessed on 7 January 2025. Australian shredded was assessed at $360-365/t CFR, while Australian HMS 80:20 stood at $345-350/t. Hong Kong-origin PNS was heard at around $365/t, Malaysian busheling at $370/t, and Brazilian HMS at $340-345/t.

Bulk sellers from Singapore and Australia continued to ask close to $360/t for mixed cargoes, while buyers largely targeted around $350/t.

BigMint’s weekly assessments

- European-origin HMS (80:20) was at $343/t, unchanged w-o-w.

- European-origin containerised shredded dropped by $2/t w-o-w to $363/t.

- Japanese-origin H2 bulk was stable w-o-w at $342/t.

- US-origin HMS (80:20) bulk increased by $1/t w-o-w to $362/t.

As per a Dhaka-based scrap buyer, Australian-origin indicatives were at around $365-370/t CFR Chattogram for PNS/busheling, while HMS 90:10 and shredded were in the $350-360/t range. For Bangladesh, HMS 80:20 was indicated at $325-330/t and HMS 1 at $335-340/t CFR.

As per a Chattogram-based bulk scrap trader, bulk offers remain limited from across origins. US-origin HMS was heard offered at $360-365/t and above against bids at $355/t, while Japanese H2 and HS are quoted in the $345-375/t range, with bids at $338-368/t. Singapore PNS is being offered at $365-370/t, though buying interest was seen at around $356-360/t. A few bulk-buying mills have already met their requirements and are now out of the market until February-March, which is putting further pressure on buying activity.

HMS 80:20 (bulk) cargo of around 10,000 t from Singapore was offered at $355/t CFR Chattogram, with buyers attempting to close at around $350-352/t. Japanese HS was quoted at $378/t, while H1/H2 (30:70) at around $350/t and H2 at $345/t.

Recent deals

- Around 3,000 t of HMS 1 (90:10) from Chile sold at $347/t CFR Chattogram.

- About 2,000 t HMS 1 (90:10) of Australian origin booked at $350/t CFR.

- Around 1,000 t of Australian-origin HMS (80:20) booked at $345/t CFR.

Domestic market

As per a Chattogram-based mill official, domestic rebar prices remain largely unchanged at around BDT 78,000/t ($638/t) in Chattogram and BDT 73,000-74,000/t ($597-605/t) in Dhaka, which continues to cap mills’ appetite for higher prices.

Bangladesh’s ship recycling market remains under pressure following the tonnage glut in November last, with prices down nearly $50/LDT from Q4 highs. Chattogram recyclers have turned largely uncompetitive, weakening demand and sentiment, while political uncertainty ahead of the February elections and recent unrest continue to weigh on confidence. Despite being the subcontinent’s only market with arrivals this week, volatile steel plate prices, a weaker taka at BDT 122.30/$, and limited buyer appetite point to a fragile outlook, increasing the risk of tonnage shifting to alternative destinations.

Outlook

Near-term sentiment in Bangladesh’s scrap market is expected to remain cautious, with prices likely to remain range-bound due to weak steel demand and selective mill buying. Buying is expected to stay muted through January, with a gradual pickup likely after February as mills return to the market and availability improves, though downside risks persist given the fragile ship-recycling environment and broader political and economic uncertainties.

Leave a Reply