- Import prices rise on supply constraints, freight costs

- Buying interest subdued amid cautious steel demand

- Export concentration risks persist in the steel sector

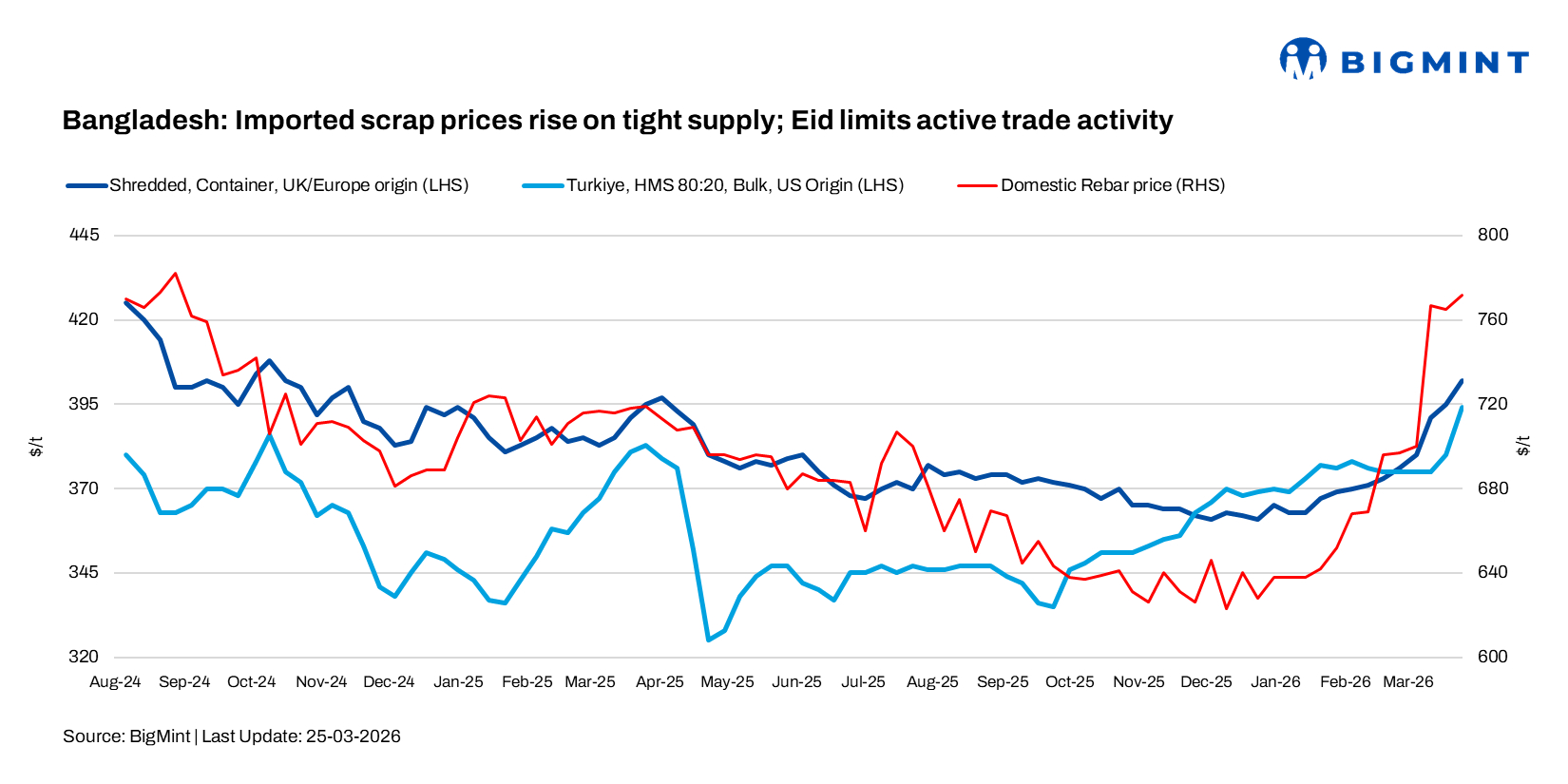

Bangladesh’s imported ferrous scrap market remained firm during the week, with prices increasing by around $15-20/t since early March, supported by higher freight costs and constrained supply from key exporting regions. However, trading activity stayed limited as mills largely refrained from aggressive bookings during the Eid holiday period, opting instead for a wait-and-watch approach.

BigMint’s weekly assessments

- European-origin containerised HMS (80:20): $377/t, up $2/t w-o-w

- European-origin shredded (containerised): $402/t, up $7/t w-o-w

- Japanese-origin H2 (bulk): $389/t, inched up $1/t w-o-w

- US-origin HMS (80:20) bulk: $395/t, rise by $5/t w-o-w

Market trends

Indicative imported scrap prices from Oceania and East Asia origin held firm at elevated levels, with HMS (80:20) at $380/t, HMS 1 at $390/t, shredded at $400/t, and plate and structure (PNS) at $410-415/t CFR Chattogram.

Some buyers continued to pay a premium for cargoes from Oceania and East Asia amid tight availability. Market participants reported limited spot offers, with only a small Australian cargo of busheling bundles (300-500 t loading) available at $410/t CFR.

Market chatter also indicated possible bookings at elevated levels near $430-440/t for shredded CFR Chattogram; however, these remained unconfirmed, with limited clarity on deal specifics and volumes.

A UK-origin shredded cargo was booked at $400/t CFR (1,000 t) ahead of Eid, while deals for Australian-origin PNS and HMS 1 were heard at $400/t (1,000 t). Additionally, a Hong Kong-origin PNS cargo was concluded at $413/t (1,500 t) on a CFR Chattogram basis.

Demand and sentiment

Buying interest remained selective, as mills closely monitored domestic finished steel price trends before committing to high-cost imports. Weak downstream demand and margin pressures kept procurement largely need-based. A trader noted that “mills are hesitant to chase rising offers without clear improvement in finished steel offtake.”

A Chattogram-based trader source informed that rebar prices in Dhaka and Chattogram are currently hovering at BDT 90,000-95,000/t ($734-774/t) exw, while billet levels remain largely stable w-o-w at BDT 76,000-78,000/t ($619-635/t) exw. Local ship scrap prices in Chattogram were reported at BDT 56,000-58,000-59,000/t ($456-481/t) exy Chattogram.

Bangladesh’s steel exports have remained volatile over the past five fiscal years, reflecting structural gaps in market diversification. Export earnings rose sharply from $7.2 million in FY20-21 to $19.2 million in FY21-22 but declined to $12.6 million in FY22-23 and $11.9 million in FY23-24, before a modest recovery to $13.9 million in FY24-25, indicating only partial improvement amid weak external demand.

Market participants attribute this trend to shifting regional demand, pricing pressures, and rising input costs, including raw materials and energy. Export performance has also been constrained by limited product diversification and heavy reliance on a single market.

India continues to dominate Bangladesh’s steel export ecosystem, particularly the northeastern region, highlighting significant market concentration. While Thailand and China briefly emerged as alternative destinations, volumes have not been sustained.

A few major producers–BSRM, GPH Ispat, KSRM, and Abul Khair Steel—account for a large share of exports, even as expanding domestic capacity remains underutilised. Industry stakeholders emphasise the need for policy support and improved market access to diversify into new geographies and stabilise export growth.

Outlook

Imported scrap prices are expected to remain firm in the near term on tight global supply and elevated freight costs. However, weak finished steel demand and cautious mill buying may limit further upside, with a clearer direction likely post-holidays.

Meanwhile, Bangladeshi mills are gradually exploring steel export markets beyond India, particularly Southeast Asia, though inconsistent volumes and demand uncertainty continue to cap momentum.

Leave a Reply