- Mild rebound likely by mid-Apr as operations resume

- HKC deadline uncertainty weighs on ship scrap pricing

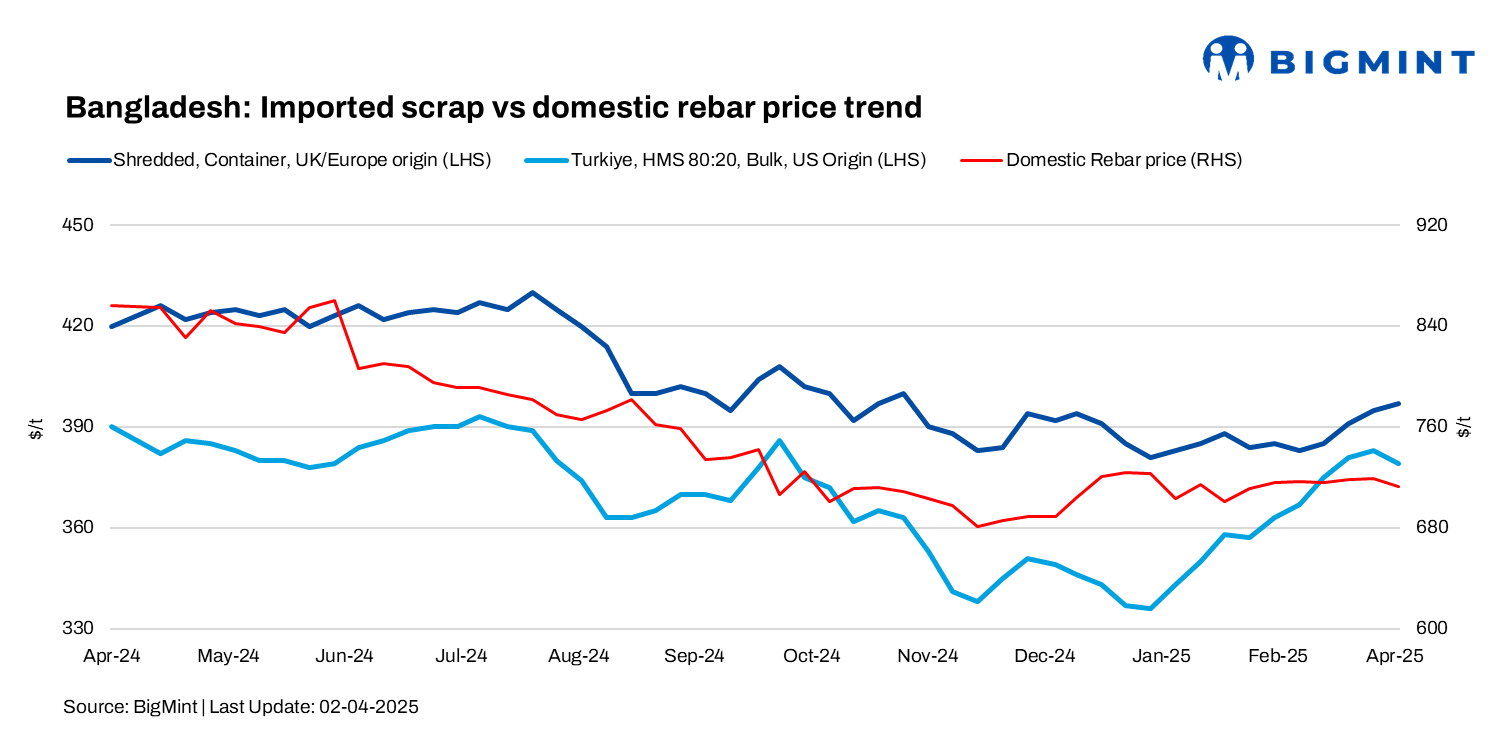

Bangladesh’s imported scrap market remained slow amid the Eid holidays, with mills operating at low capacity utilisation amid reduced steel consumption from end-users. Scrap prices were largely stable w-o-w amid limited market activity.

BigMint’s weekly assessments

- European-origin HMS (80:20) was stable w-o-w at $375/t.

- US-sourced HMS (80:20) bulk prices stood at $384/t, steady w-o-w.

- Japanese-origin H2 bulk prices stood at $372/t CFR Chattogram, unchanged w-o-w.

- European-origin containerised shredded inched up by $2/t w-o-w to $397/t.

Market commentary

A Chattogram-based trader noted that the market remains closed until 5 April, with buyers expected to return by 6-7 April. Last heard offers included HK PNS at $395-400/t CFR, Australian HMS 80:20 at $370-375/t, shredded at $390-392/t, Malaysian busheling at $400/t, and Singapore PNS at $396-400/t.

A Bangladeshi importer noted that market activity was slow amid the Eid holidays, with reopening expected on 6 April. Domestic ship scrap was at BDT 57,000-58,000/t ($471-480/t) ex-yard, Dhaka rebars at BDT 82,000-83,000/t ($679-687/t) exw, and Chattogram rebars at BDT 85,500-86,000/t ($707-712/t) exw.

A scrap importer reported containerised offers: Australian HMS at $370/t, shredded at $390/t, and busheling at $400/t CFR. In bulk, USWC HMS was offered at $382-385/t, while Singapore HMS stood at $374-378/t CFR. Another trader noted Malaysia PNS at $398-400/t CFR Chattogram but said rising prices are limiting inquiries.

Recent imported deals

- 1,000 t of oversized PNS from Hong Kong were booked at $393/t CFR Chattogram.

- 4,000 t of HMS 80:20 from Australia were sold at $360-365/t CFR Chattogram.

- 3,000 t of shredded from Australia were traded at $385/t CFR Chattogram.

Bangladesh’s ship-breaking market

Bangladesh maintained strong pricing in the ship-recycling market, with premiums for preferred vessels ahead of the 31 March yard upgrade deadline. Notably, recyclers failing to upgrade will be barred from importing ships after Eid, with further restrictions looming for yards not compliant with the Hong Kong Convention (HKC) by June.

A very large crude carrier (VLCC), listed by the Office of Foreign Assets Control (OFAC), is set to depart for India, while another remains stranded due to the absence of a resale deal and NOC. Meanwhile, Chattogram Port received 61,859 light displacement tonnage (LDT), a sharp drop from 103,617 LDT the previous week. Despite some interest in prompt delivery units, steel prices remained flat w-o-w at $529/t, and the Bangladeshi taka showed minimal movement. Concerns over the Myanmar earthquake could impact operations in Chattogram.

Outlook

Market activity is set to remain stagnant over the next 10 days due to the ongoing Eid holidays, delaying trade flow and consumption. A gradual recovery is expected from mid-April as operations resume, but a sharp rebound is unlikely due to weak end-user demand. Industry participants remain cautious, expecting only a limited post-holiday revival in prices and demand.

Leave a Reply