- Containerised trades anchor price levels

- Seasonal slowdown tempers buying activity

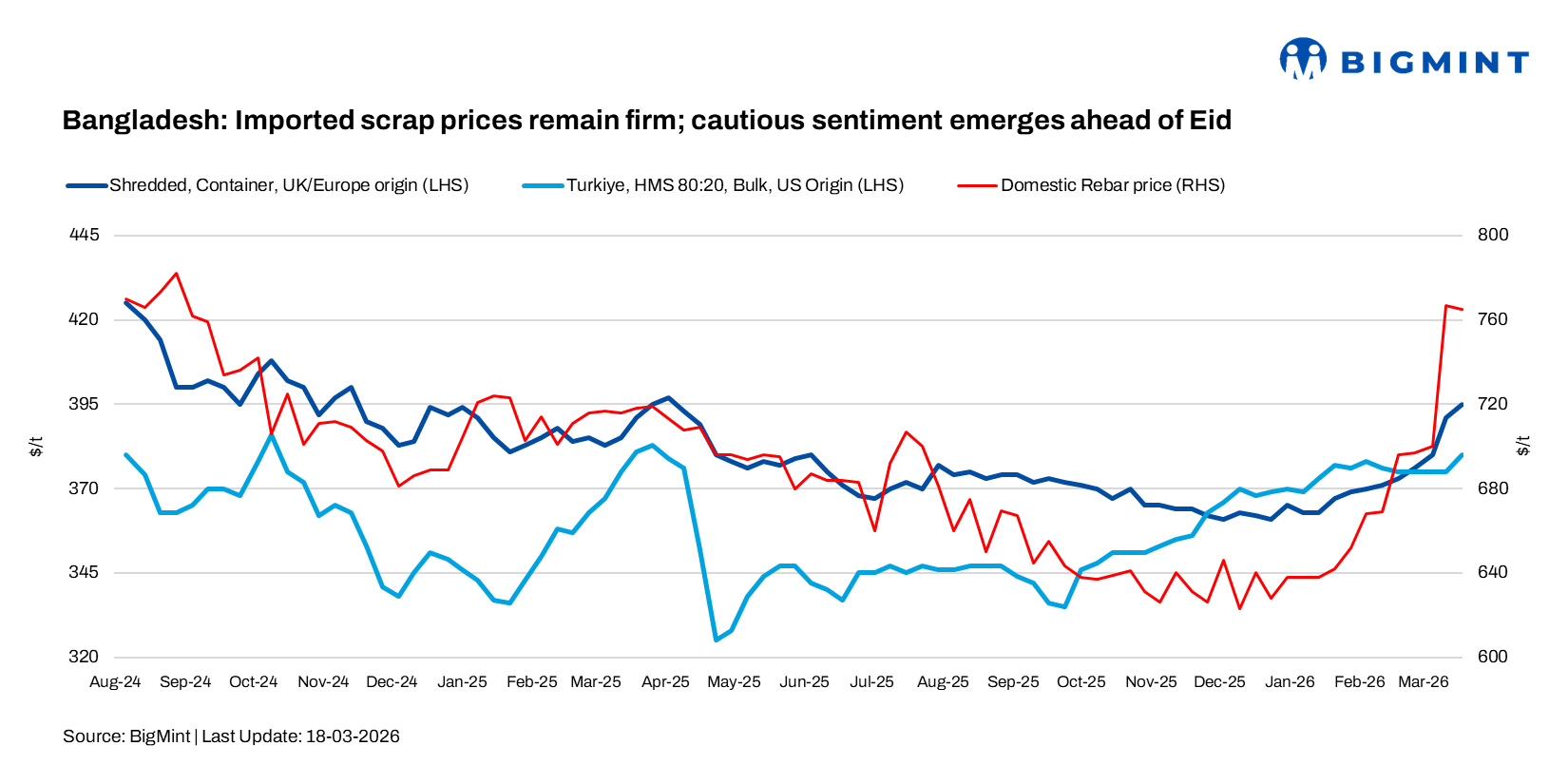

Bangladesh’s imported ferrous scrap market remained firm in mid-March, supported by tight global supply, and rising freight costs, although buying turned cautious ahead of the Eid holidays.

Recent containerised transactions indicate stable-to-firm price levels across key grades, with Hong Kong-origin PNS deals concluded at $405-410/t CFR Chattogram and Singapore-origin material at similar levels, while Philippines-origin GI bundles were booked lower at $335/t CFR. Brazil-origin HMS (90:10) was heard at $370/t CFR.

BigMint’s weekly assessments

- European-origin HMS (80:20): $375/t, up $5/t w-o-w

- European-origin shredded (containerised): $395/t, up $4/t w-o-w

- Japanese-origin H2 (bulk): $388/t, stable w-o-w

- US-origin HMS (80:20) bulk: $390/t, inched up $1/t w-o-w

Market comments

A Dhaka-based trading house noted that rebar prices in Dhaka and Chattogram are currently hovering at BDT 88,000-93,000/t ($716-757/t) exw while billet levels remain largely stable at BDT 75,000-76,000/t ($611-619/t) exw. Local ship scrap prices in Chattogram were reported at BDT 56,000-58,000/t ($456-472/t) exy Chattogram.

The trader highlighted that most mills are keeping their offers open due to ongoing uncertainty in freight rates, particularly from Australia, Hong Kong, and Singapore, where prices remain firm. This has increased cost pressure on buyers, especially as finished steel demand is only sufficient to sustain basic margins, limiting aggressive procurement.

A Japan-origin bulk scrap supplier stated that most Japanese traders are currently prioritising Bangladesh as a key destination, but due to ongoing uncertainty in freight rates, which has limited the ability of many participants to secure workable deals.

The supplier added that the market is in a wait-and-watch phase, with traders open to negotiations but refraining from issuing firm offers until freight levels stabilise and clearer cost visibility emerges.

An Australia-based scrap trader indicated that export offers to Bangladesh remained firm, with Australia/New Zealand HMS (80:20) heard at $375-380/t CFR Chattogram, HMS 1 at $385-390/t, shredded at $395-400/t, and PNS at $415-420/t.

Recent trades

- Hong Kong-origin PNS: 500 t at $405/t CFR Chattogram

- Hong Kong-origin PNS (with rebar bundles): 500 t at $410/t CFR Chattogram

- Philippines-origin GI bundles: 500 t at $335/t CFR Chattogram

- Singapore-origin PNS: 500 t at $405/t CFR Chattogram

- Brazil-origin HMS (90:10): 500 t at $370/t CFR Chattogram

- Singapore-origin rerolling (plate cutting scrap): 500 t at $425/t CFR Chattogram

- Hong Kong-origin PNS (with rebar bundles): 1,000 t at $407/t CFR Chattogram

Ship-recycling: Bangladesh remained the most active ship recycling market during the week, with Chattogram yards securing multiple vessel deals, including three LNG carriers of around 28,800 LDT each and several handymax bulkers of about 8,000 LDT. Strong buying kept the country ahead of competing destinations.

However, recyclers faced margin pressure as the Bangladeshi taka weakened against the US dollar and local steel plate prices declined by around $4/t to $502/t. Operational challenges, including fuel rationing and electricity shortages, also disrupted yard activity and slowed overall processing.

Outlook: Over the next week, scrap prices in Bangladesh are expected to remain firm, supported by tight supply and elevated freight costs. However, buying activity is likely to stay slow ahead of Eid, with market sentiment gradually turning cautious as participants anticipate a temporary slowdown in procurement. Mills are expected to focus largely on need-based purchases, avoiding aggressive bookings amid uncertainty. Overall, the market is entering a quieter phase, and clearer direction is likely to emerge once trading activity resumes after the holiday period.

Leave a Reply