- Payment hurdles, weak finished steel demand limit trade

- Buyers to continue preferring short-term, small-lot deals

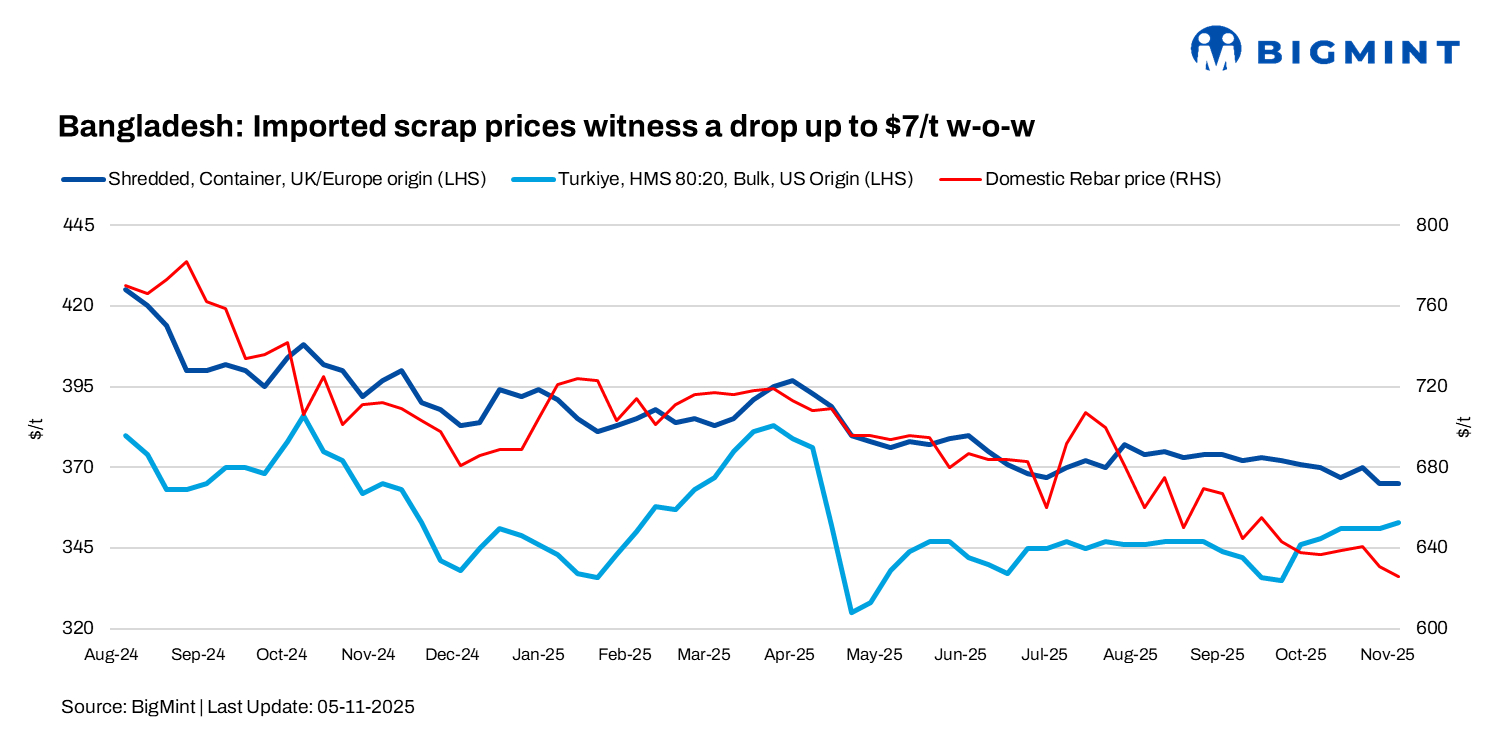

Bangladesh’s imported scrap market declined by up to $7/tonne (t) w-o-w across major grades, particularly in bulk scrap, as weak finished steel demand kept mills cautious and limited fresh bookings. Persistent hurdles in opening letters of credit (LC) and payment delays continued to constrain trade activity.

BigMint’s weekly assessments

- European-origin HMS (80:20) prices inched down by $1/t w-o-w to $345/t.

- European-origin containerised shredded was steady w-o-w at $365/t.

- Japanese-origin H2 bulk prices stood at $341/t, decreasing by $7/t w-o-w.

- US-sourced HMS (80:20) bulk prices inched up by $2/t w-o-w to $352/t.

As per market insiders, scrap offers from Australia and New Zealand remained limited, with Hong Kong-origin PNS heard at $365-368/t and HMS 70:30 from South America at $330-335/t. Notably, cargoes from Chile and Brazil rarely reach Bangladesh — unless prices and payment terms align — while most such material is typically diverted to the Indian market.

Domestic market

Domestic scrap prices stood at BDT 46,000-47,000/t ($377-385/t) exw Chattogram, while rebar traded at BDT 76,000-78,000/t ($624-640/t) in Chattogram and BDT 72,000-73,000/t ($591-599/t) in Dhaka. Billet prices were around BDT 63,000-64,000/t ($517-525/t).

Ship-recyclers make selective buys amid weak sentiment

Selective buying by a few active recyclers in Chattogram lent slight support to the ship-breaking market, as they aimed to maintain yard activity and meet LC obligations. However, overall sentiment stayed weak, with steel prices down by $3/t w-o-w to $530/t. Political uncertainty ahead of the 2026 elections and rising inflation weighed on confidence, even as 21 HKC-certified yards enhanced the country’s compliant recycling capacity.

Outlook

The imported scrap market is likely to remain under pressure in the near term as mills continue to face LC constraints and slow finished steel demand. Buying activity may stay selective — limited to small lots for immediate requirements — with prices expected to hover around current levels until domestic demand and liquidity conditions improve with post-election clarity. Weak construction demand may also limit a steel market recovery.

Leave a Reply