- LC constraints and weak steel demand continue to slow fresh bookings

- Buyers remain selective on quality; firm April bookings reduce urgency

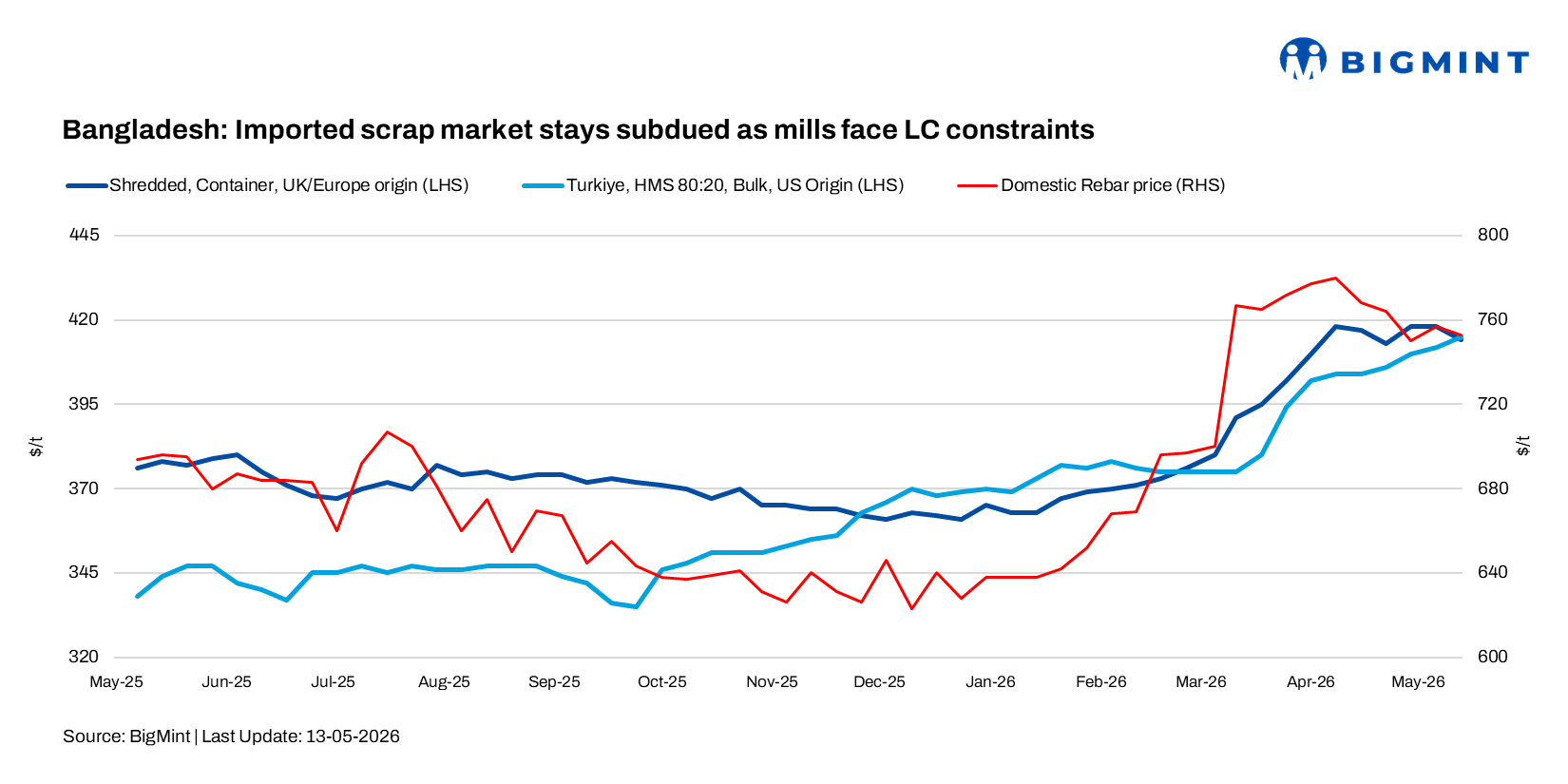

Bangladesh’s imported ferrous scrap market remained largely quiet in the week ended May 13, with most mills staying away from aggressive fresh bookings after securing sizeable volumes in April. Market participants estimated that around 80,000-90,000 t of scrap were booked last month, which has reduced immediate procurement urgency across the market.

Market participants noted that liquidity pressure, delayed payments, and ongoing LC-related constraints continued to affect fresh import activity.

Containerised offers remained available in the market, although buying interest stayed limited. Offers heard during the week included UK/EU-origin shredded scrap at around $418/t CFR Chattogram, Australia-origin HMS 1 at $412/t CFR, and Australian-origin pure PNS at around $422/t CFR. However, market participants said no active bids were heard against these offers.

BigMint’s weekly assessments CFR Chattogram

- European-origin containerised HMS (80:20): $390/t, stable w-o-w

- European-origin containerised shredded: $414/t, down $4/t w-o-w

- Japanese-origin bulk H2: $407/t, inched down by $1/t w-o-w

- US-origin bulk HMS (80:20): $410/t, dropped by $2/t w-o-w

Market comments

A Hong Kong-based trader commented: “Most mills are already carrying April-booked inventories, while overall steel demand remains slow. Buyers are cautious because financing conditions are still tight and payment cycles have become longer.”

Market participants added that some exporters have increasingly shifted focus toward Southeast Asian destinations such as Indonesia and Taiwan, where payment visibility and overall deal execution remain comparatively smoother than in Bangladesh.

A Dhaka based scrap trader said: “Bangladesh buyers are still active, but the number of active participants has reduced significantly. Most buyers are purchasing only when pricing becomes highly workable.”

A Chattogram-based importer commented: “Buyers here generally prefer hand-loaded material from the US, Brazil, or Africa. There is still hesitation toward UK/EU-origin HMS cargoes unless pricing becomes very competitive.”

Australian-origin shredded scrap offers were largely heard around $410-415/t CFR, while HMS 80:20 offers were indicated near $395/t CFR. Australia-origin bushelling was heard at $425-430/t CFR. Meanwhile, offers for HMS 1 and PNS from Hong Kong were reported at around $410-425/t CFR, although market participants said deal activity remained slow. Separately, Malaysia-origin GI bundles were reportedly sold around $448/t CFR Chattogram, while HMS bundles from Malaysia were heard near $390/t CFR.

On the bulk side, market participants reported that around 8,000 t of Australia-origin bulk scrap cargo comprising GI bundles, HMS 90:10, and shredded scrap is expected to arrive in Bangladesh shortly.

Domestic rebar prices were largely heard around BDT 92,000-93,000/t ($750-758/t) in Chattogram, while Dhaka rebar prices were indicated at BDT 86,000-88,000/t ($701-717/t), reflecting relatively weak downstream steel demand conditions.

Outlook

Bangladesh’s imported scrap market is expected to remain cautious in the coming days, with mills likely to continue booking selectively amid weak finished steel demand, tight liquidity, and ongoing LC-related challenges. While freight costs and limited container availability may continue to support offer levels, sizeable April bookings and comfortable inventories could keep fresh buying activity relatively subdued.

Leave a Reply