- Financing constraints continue impacting mill purchases

- Higher electricity costs pressure steelmakers’ margins

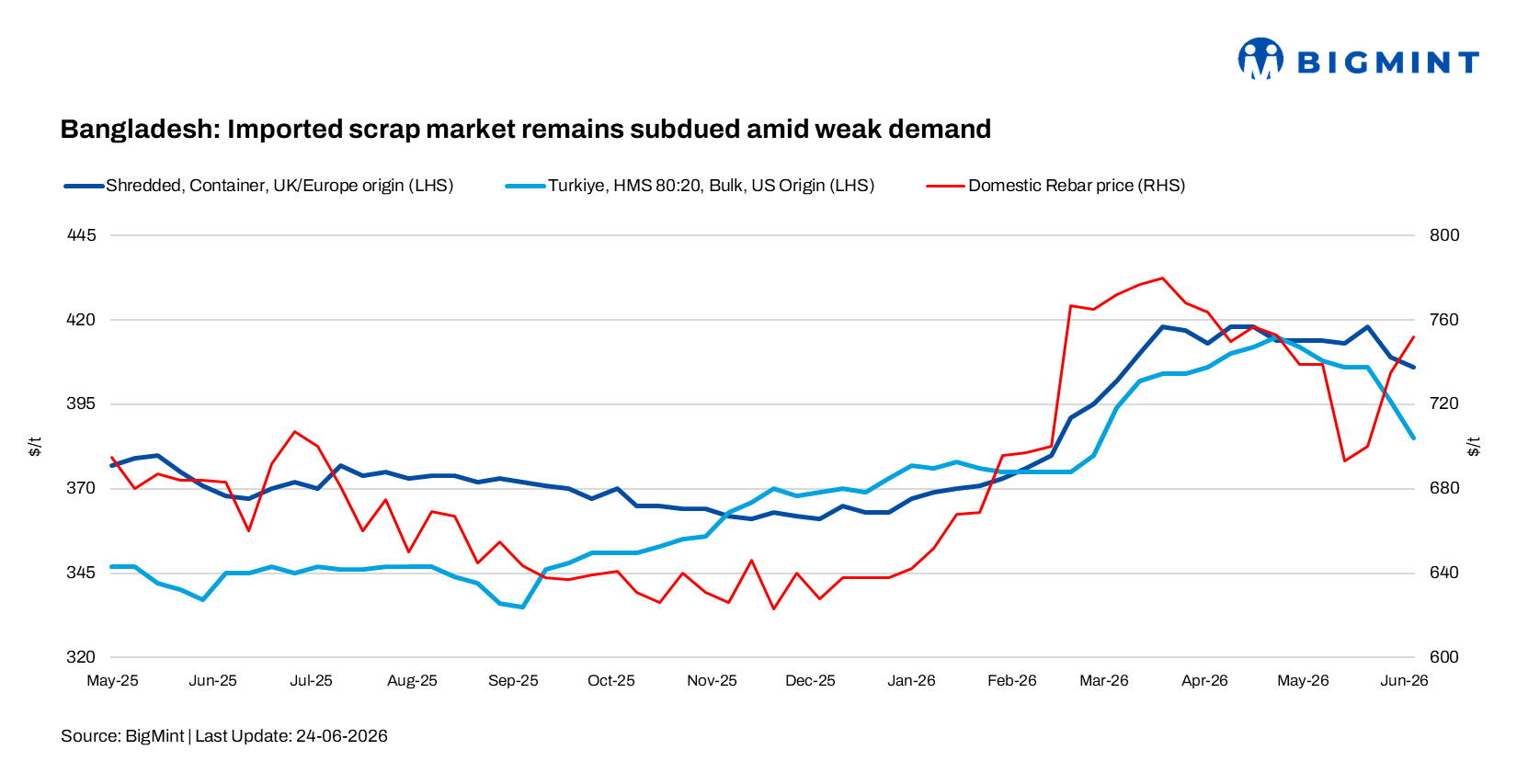

Bangladesh’s imported ferrous scrap market remained quiet during the week ended 24 June, with limited buying interest as weak steel demand, financing challenges, and uncertainty surrounding the recently announced national budget continued to weigh on sentiment. Most mills remained cautious and refrained from booking fresh cargoes, anticipating softer price levels after Muharram. UK-origin HMS 80:20 was heard around $375/t CFR. UK-origin shredded scrap was offered at approximately $405-406/t CFR.

Australian-origin HMS 80:20 was indicated at $380/t CFR against bids at $365/t CFR. Australian-origin shredded scrap was offered around $410/t CFR, although market participants suggested workable levels could move closer to $390/t CFR. Singapore-origin PNS, carrying a premium over HMS grades, was heard to be offered at $420/t CFR. GI bundles from Southeast Asian origins were offered around $340/t CFR.

BigMint’s weekly assessments, CFR Chattogram

- European-origin containerised HMS (80:20): $375/t down $3/t w-o-w

- European-origin containerised shredded: $406/t, down by $3/t w-o-w

- Japanese-origin bulk H2: $394/t, down by $4/t w-o-w

- US-origin bulk HMS (80:20): $399/t, down by $6/t w-o-w

US-origin HM (80:20) bulk scrap offers were reported at $400/t CFR Chattogram, while Japanese H2 scrap was indicated near $394-396/t CFR, though no firm offers or transactions were reported following the latest Kanto tender results. Buyers continued targeting lower workable levels, reflecting weak confidence in near-term steel demand.

Market comments

A Chattogram-based trader said, “The market is very soft, and buyers are not entertaining offers at current levels. Most participants are waiting for clearer demand signals after Muharram.”

Another South East Asian supplier noted, “Following the latest Kanto Tender results, no fresh bookings for Japanese scrap were reported in Bangladesh despite indications that material sold through the tender was destined for the country.”

Market participants noted that buying activity remained extremely slow, with both Bangladeshi and Pakistani buyers largely absent from the market. Limited access to trade financing and concerns over proposed tax and duty increases in the FY 2026-27 budget continued to discourage procurement activity.

Domestic market

Domestic scrap prices were heard at BDT 52,000-55,000/t ($423-447/t), while broader market indications remained around BDT 54,000/t depending on grade and location. Rebar prices were assessed at BDT 86,000-88,000/t ($699-716/t) ex-Dhaka, while rebar in Chattogram was heard at BDT 92,000-94,000/t ($748-764/t) ex-works. Billet prices were reported at BDT 71,500-72,000/t ($581-585/t).

The Bangladesh Steel Manufacturers Association (BSMA) continued to oppose proposed increases in VAT and import duties outlined in the national budget, warning that higher taxes could further increase steel production costs. The association also reiterated concerns regarding recent electricity tariff hikes of around 17%, citing additional pressure on mills already operating below 50% capacity.

Domestic steelmakers remain challenged by rising energy, transportation, port, and logistics costs, limiting their ability to absorb higher raw material prices.

Outlook

Bangladesh’s imported scrap market is expected to remain sluggish in the upcoming days. Weak steel demand, restricted financing availability, and budget-related uncertainty are likely to keep buyers cautious. Market participants expect trading activity to improve gradually after Muharram, although buyers will continue to target lower workable levels amid soft regional sentiment.

Leave a Reply