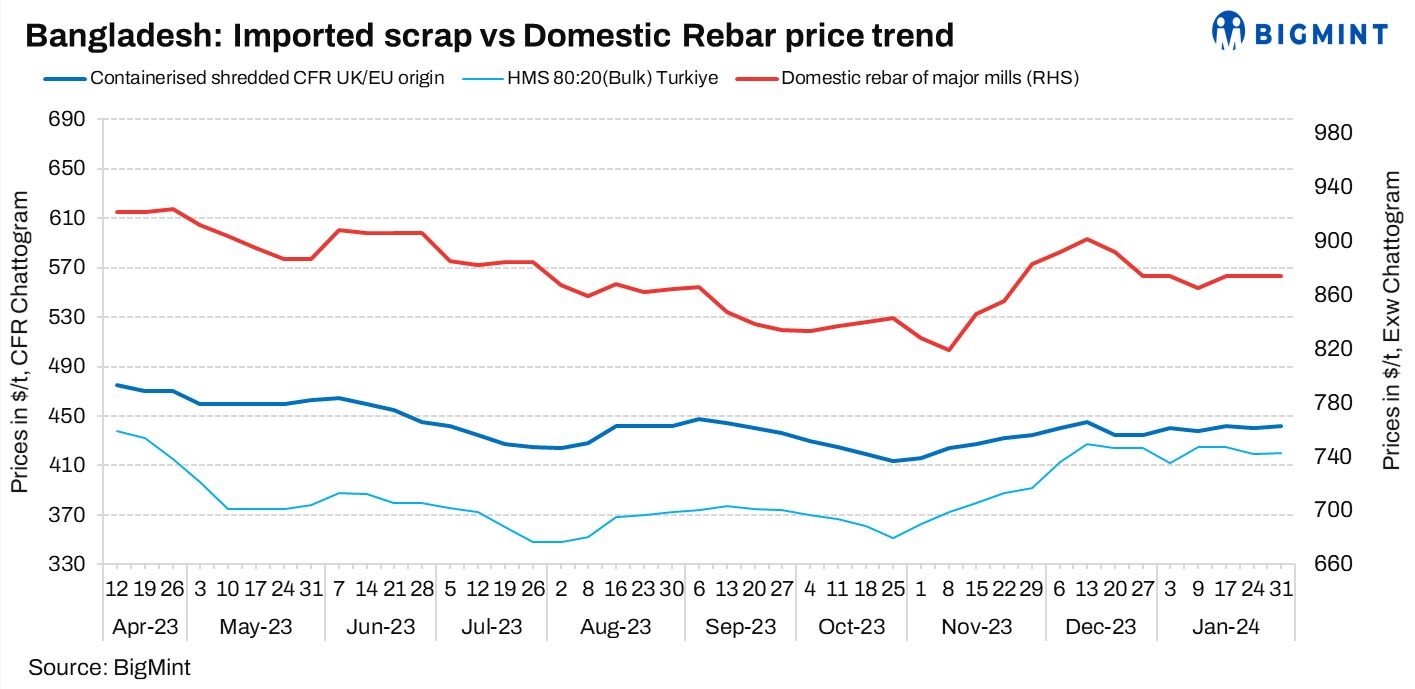

Bangladesh imported ferrous scrap market showed less activity, with a mixed price trend in containerised scrap amid weaker finished steel demand.

As per market insiders, the imported market remained sluggish as customers were in wait-and-watch mode, with expectations that the dullness will persist for yet another month till buyers liquidate their stocks which are high at present.

A representative from a trading company stated, “European shredded offers are at $440-450/tonne, depending on shipment days. Suppliers are slightly slow due to bad weather. We are exploring the Middle East and Australia.”

The Europe-origin shredded scrap (containers) assessment by BigMint rose by $2/t w-o-w to $442/t, while HMS (80:20) containers assessment dropped by $2/t to $417/t. In bulk scrap, Japan-origin H2 and US-origin HMS (80:20) assessments remained stable at $430/t for both.

Recent deals

Around 1,000 t of Singapore-origin PNS-grade scrap were sold at $445/t CFR Chhattogram.

Around 1,000 t of UAE-origin HMS 1 were sold at $425/t on CFR Chattogram basis.

A parcel of 1,000 t of HMS bundles from Brazil got sold at $394/t CFR Chattogram.

Approximately 1,000 t of HMS (90:10) from Australia were booked at $418/t on a CFR basis.

Recent offers and indicatives

Europe-origin HMS (80:20) in containers was being offered at $415-420/t CFR.

Shredded containers from Europe were being offered at $440-445/t CFR Chattogram.

Australia-origin HMS (80:20) (containers) was offered at $425-430/t CFR Chattogram.

Japan-origin H2 (bulk) scrap indicatives were heard at $425-430/t CFR.

US-origin HMS (80:20) bulk indicatives were heard at $430-435/t CFR Chattogram.

Domestic market: In the local market, shipyard scraps were being offered at BDT 63,000-64,000/t, while PNS quality scraps stood at BDT 66,000/t. Domestic rebar prices were reported at BDT 87,000-89,000/t ex-Dhaka and BDT 93,000-96,000/t ex-Chattogram.

Rebar prices rise post-election: Steel rebar prices in Bangladesh have surged by BDT 3,000-4,000/t in two weeks due to factors such as increased fuel costs, gas supply shortage, rising global raw material booking rates, and reduced imports amid a dollar crisis. The 75-grade rebar prices range from BDT 93,000-96,000/t, up from the pre-election range of BDT 91,000-92,000/t. Industry insiders attribute the hike to higher international raw material booking rates and insufficient imports due to the dollar crisis, impacting steel production costs. Despite the construction season’s start, the steel sector faces challenges like insufficient gas supply and low demand.

Overall imports drop y-o-y: In the first half of FY’24 (July 2023 to June 2024), Bangladesh’s overall imports experienced an 18% y-o-y decline to $33.68 billion amid various economic challenges. Settlement of letters of credit (LCs) stood at $33,683.51 million in July-December, compared to $41,175.28 million a year earlier. Overall import orders decreased by 5.33% y-o-y to $32,929.31 million during the same period. Bangladesh’s trade deficit for the last fiscal year dropped by 48% y-o-y to $17.16 billion. The Bangladesh Bank has implemented measures to address economic challenges, including a 25 basis point increase in the policy rate to 8% to manage demand-side pressures while supporting priority sectors, including manufacturing.

Outlook

As per market insiders, post-general election optimism surrounds the Bangladesh imported ferrous scrap market. Expectations include enhanced infrastructure spending and improved LC availability in the near term. A slower start is anticipated in the first quarter but increased momentum in the steel sector is expected by end-March.