- Market pressured by HKC delays, currency, steel prices

- Japanese bulk scrap tags rise after Kanto tender

Bangladesh’s imported scrap market remained largely subdued this week, with overall trading volumes staying minimal amid weak steel demand, persistent rains, and sluggish construction activity. Although a few spot deals were heard, buyers continued to resist higher offers as market sentiment remained bearish.

BigMint’s weekly assessments

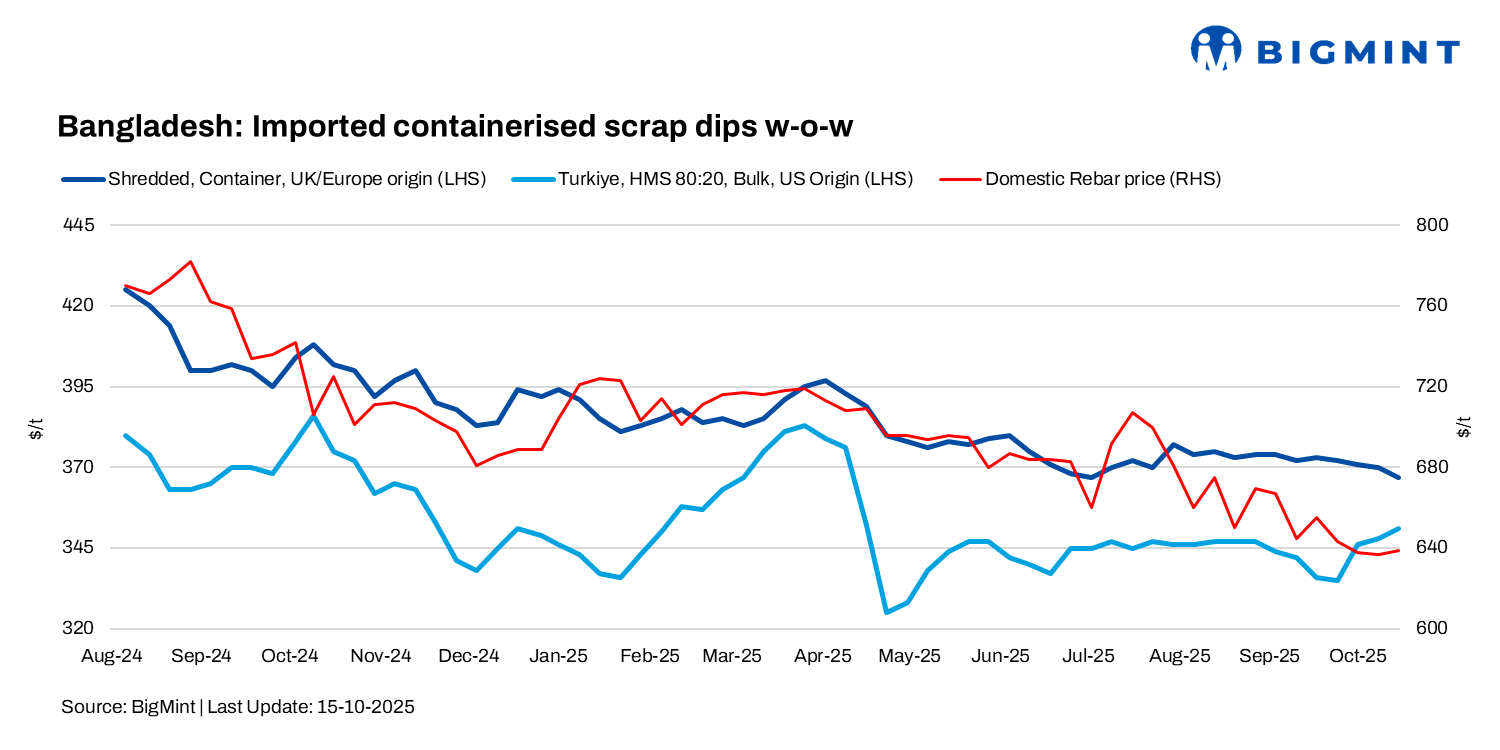

- European-origin HMS (80:20) prices inched down by $1/t w-o-w to $348/t.

- European-origin containerised shredded inched down by $3/t w-o-w to $367/t.

- Japanese-origin H2 bulk prices stood at $346/t, increasing by $5/t w-o-w.

- US-sourced HMS (80:20) bulk prices stable w-o-w at $349/t.

As per market insiders, a Hong Kong-origin PNS cargo of 1,000 t was sold at $373/t CFR Chattogram, while workable levels for Singapore-origin PNS were reported near $375/t. Offers for Australian HMS 80:20 were around $345/t CFR, and shredded scrap from the same origin stood at $364/t CFR.

As per a Dhaka-based supplier, the scrap market remains subdued due to ongoing rains and weak finished steel demand. Some optimism is emerging post-election, but activity is minimal, with no deals reported and buyers largely out of the market.

As per a Japan-based exporter, H2 scrap is priced at $300-305/t FOB Japan. With freight at $45-50/t, the CFR Chattogram cost comes to around $345-350/t, aligning with post-Kanto October tender levels. While a softer JPY has spurred some buying interest, overall market activity remains muted amid regional holidays.

Domestic market

Domestic scrap prices hovered at BDT 47,000-49,000/t ex-yards ($386-403/t). Rebar prices were reported at BDT 78,000-80,000/t exw in Chattogram ($641-657/t) and BDT 73,000-74,000/t exw in Dhaka ($600-608/t), while billet traded at BDT 64,000-65,000/t exw ($526-534/t).

Bangladesh Ship Recycling

The market remained largely inactive in September due to HKC delays, political instability, and weak economic conditions. Some revival emerged as attractive Capesize deals drew buyers, though flat steel prices and currency weakness kept sentiment cautious. Only 36,993 LDT was recycled, down 16% from August’s 43,830 LDT, with just two ships processed amid rising inventories and competition from India and Pakistan.

Outlook

In the near term, Bangladesh’s scrap market is expected to remain sluggish. Persistent delays in construction projects keep end-user steel demand weak, while mills remain cautious in purchasing imported and domestic scrap. Domestic prices are likely to stay stable, and imported scrap/CFR deals may see limited activity. Any meaningful recovery hinges on faster resumption of infrastructure projects and post-election economic confidence.

Leave a Reply