- Bangladesh’s ship recycling market shows early stabilisation

- Overall market waits for Feb poll clarity and demand pickup

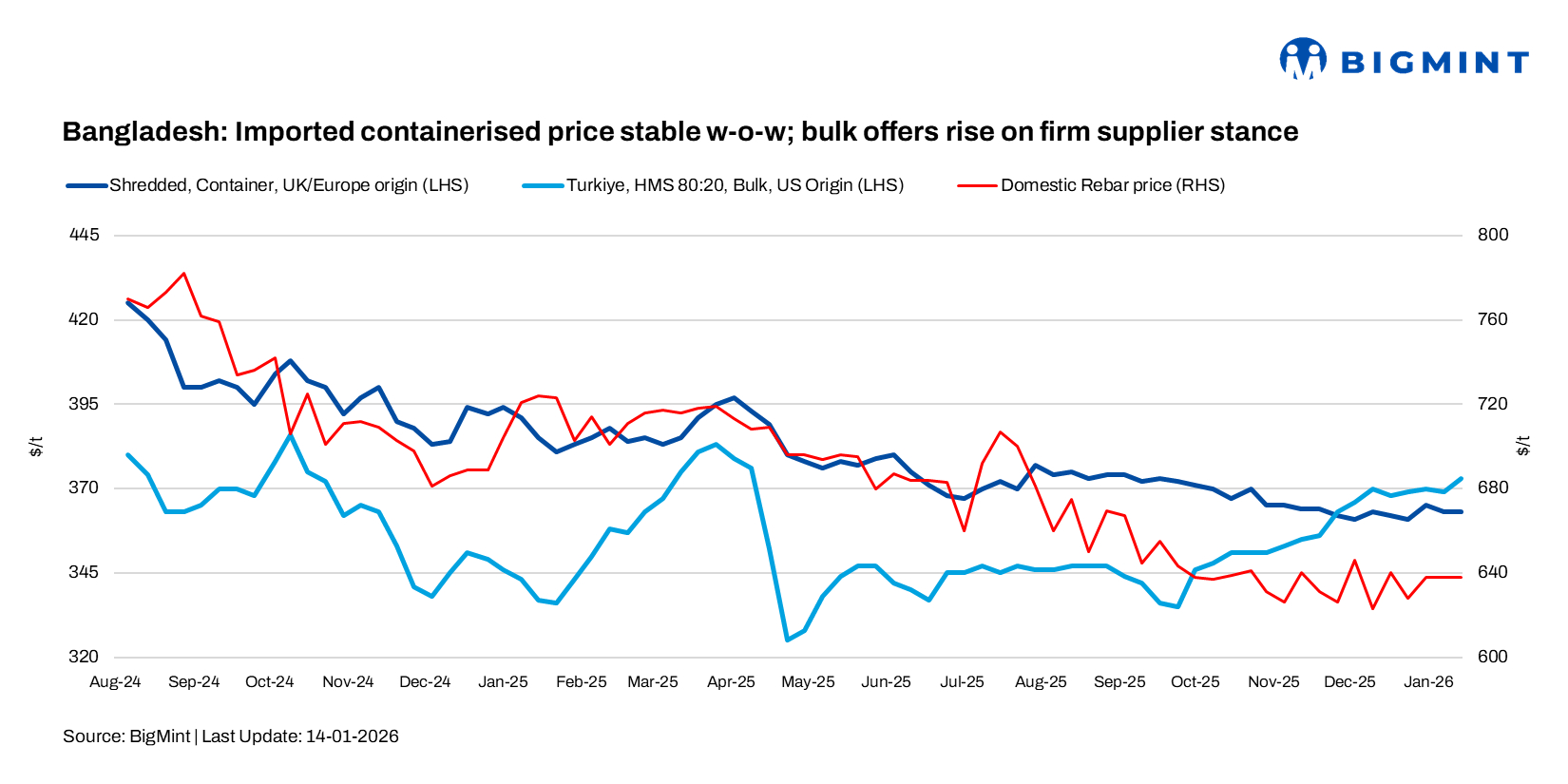

Bangladesh’s imported ferrous scrap prices were mixed week on week as of 14 January 2026, with containerised cargoes largely stable amid thin buying interest in Chattogram, while US- and Japan-origin bulk sellers held a firmer stance, tabling fresh offers $6-10 per tonne above currently workable levels.

BigMint’s weekly assessments

- European-origin HMS (80:20) was at $343/t, unchanged w-o-w.

- European-origin containerised shredded stable w-o-w to $363/t.

- Japanese-origin H2 bulk rose by $3/t w-o-w at $345/t.

- US-origin HMS (80:20) bulk increased by $3/t w-o-w to $365/t.

As per a Chattogram-based scrap trader, Australia-origin offers remain limited across origins. Australia Shredded was heard offered at $360-365/t (workable $356-358/t), while HMS 80:20 traded at $340-345/t (bids $335/t). HK PNS quoted $365-370/t (-$5/t enquiries), Malaysia Busheling at $368-372/t (bids $362-365/t), Chile HMS at $345-350/t (last traded at $347/t).

Bulk scrap indications for Japanese H2 were heard at $345-348/t (near last Kanto CFR levels), and US-origin HMS bulk was heard at $368-375/t (limited enquiries). Several mills have secured volumes and stay sidelined until Feb-Mar, capping buying momentum.

Recent deals

- 1,000 t of Hong-Kong PNS sold at 370/t CFR Chattogram

- 1,000 t of Singapore PNS sold at 375/t CFR Chattogram

- 1,000 t Hong Kong PNS (oversize) sold at $380/t CFR Chattogram

- 1,000 t UAE HMS sold at $350/t CFR Chattogram

Domestic market

As per a Chattogram-based mill official, domestic rebar prices have remained largely stable, with levels hovering around BDT 78,000/t ($638/t) in Chattogram and BDT 74,000-75,000/t ($605-614/t) in Dhaka, which continues to limit mills’ ability to push through higher prices amid weak demand.

Market participants noted that while global ferrous scrap prices have rebounded–raising replacement costs for local re-rolling mills–retail rebar prices in both Dhaka and Chattogram stayed broadly unchanged through the week. A trader in Chattogram said most mainstream rebar brands were trading in the BDT 76,000-80,000/t range, adding that no formal price hike has been announced so far, although mills have informally signalled potential increases in the near term.

Overall, weak domestic demand, persistent overcapacity, and rising input costs are keeping rebar prices under pressure, with mills moving cautiously despite higher raw material prices.

Bangladesh Ship Recycling: After sharp end-2025 price declines, Bangladesh’s ship recycling market shows early stabilisation signs this week, with demand firming despite election uncertainty. Supply remains weak–only one vessel delivered and Chattogram anchorage empty–while central bank LC processing delays curb activity. Steel plate prices resumed trading around $500/t, but fragile fundamentals keep recyclers cautious pending political clarity.

Outlook

Imported bulk scrap offers are likely to stay firm at $350-375/t amid US/Japan tightness; on the other hand, the upcoming election in February risks intensify financial constraints across major steel sectors with a halt in investments and likely capping volumes. Post-election infrastructure restart could unlock demand; expect cautious Jan restocking ahead of poll clarity.

Leave a Reply