- Ship-breaking imports decline 35% y-o-y in 4MCY’26

- Prices remain largely stable y-o-y, encouraging bookings

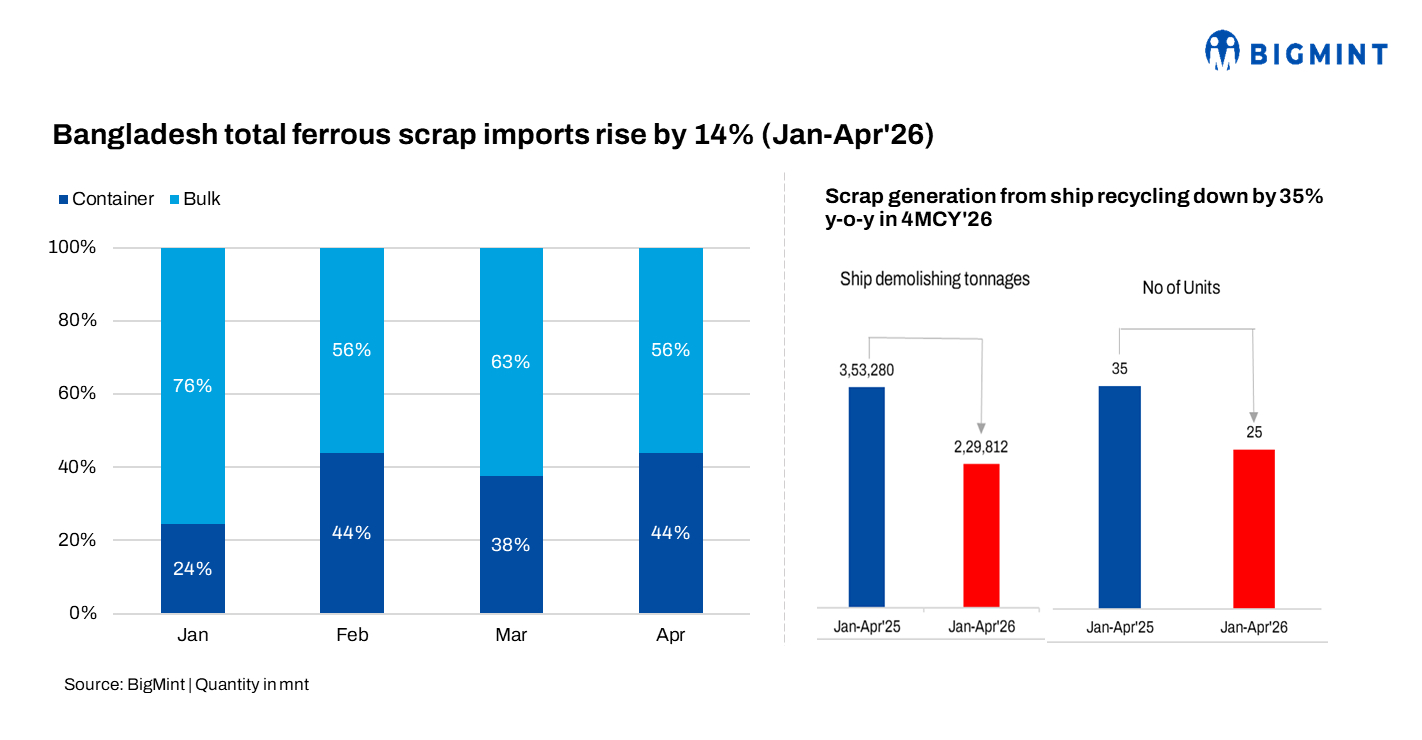

Bangladesh’s bulk ferrous scrap imports increased by 11% y-o-y during January-April 2026 (4MCY’26) to around 1.02 million tonnes (mnt), compared with 0.92 mnt in the corresponding period last year.

Meanwhile, total scrap imports, including both bulk and containerised cargoes, rose by 14% y-o-y to 1.66 mnt in 4MCY’26 from 1.46 mnt a year earlier.

On a monthly basis, Bangladesh imported around 0.31 mnt of scrap in January, which declined sharply by 42% to 0.18 mnt in February due to tighter import financing conditions and weaker industrial demand. Market participants noted, “Several banks continued maintaining strict controls on opening letters of credit (LCs) due to liquidity constraints and ongoing US dollar shortages.”

Subsequently, imports recovered to 0.25 mnt in March, nearly 39% m-o-m, and imports further improved to around 0.28 mnt in April, indicating renewed booking activity and easier opening of letters of credit. A shortage in scrap inventories at large steel mills and a lack of alternative raw materials strengthened demand for scrap imports, as mills intended to resume production activities.

The y-o-y increase in January-April was mainly supported by improved bulk scrap bookings from Japan, Singapore, and Australia, relatively stable scrap prices during the period, and steady infrastructure and construction-related steel demand in Bangladesh. Lower dependence on domestic ship-breaking scrap amid reduced vessel arrivals also encouraged mills to increase imported scrap purchases.

Country-wise imports

Among suppliers, Japan emerged as the largest exporter to Bangladesh during January-April 2026, with shipments increasing 29% y-o-y to around 0.40 mnt, compared with 0.31 mnt in the year-ago period. Strong preference for Japanese bulk cargoes, particularly H2 and mixed-grade scrap, supported the increase.

Singapore recorded the sharpest growth among major suppliers, with exports rising 111% y-o-y to around 0.19 mnt during the period against 0.09 mnt a year earlier. Australia-origin scrap imports also improved by 13% to around 0.17 mnt.

In contrast, US-origin scrap shipments declined significantly by 56% y-o-y to around 0.14 mnt in January-April 2026, compared with 0.32 mnt in the corresponding period last year, reflecting reduced competitiveness of US bulk cargoes amid higher freight costs and stronger preference for Asian-origin material. Imports from New Zealand increased by 17% to around 0.07 mnt.

Price summary

- Price trends remained mixed across major grades and origins during January-April 2026. Average prices of containerised shredded scrap (UK origin) remained largely stable at around $387/t CFR Chattogram, while containerised HMS 80:20 (Europe origin) declined by 1% y-o-y to around $365/t CFR.

- Meanwhile, Japanese H2 bulk scrap prices remained comparatively firm, averaging around $369/t CFR during January-April 2026, up 3% y-o-y. US-origin HMS 80:20 bulk prices also increased by 4% to around $383/t CFR Chattogram, supported by freight-related costs and tighter availability of deep-sea cargoes.

Ship-breaking activity slows

Ship-breaking activity remained under pressure during the quarter. Bangladesh imported around 229,812 light displacement tonnes (LDT) of ships for recycling during January-April 2026, down 35% y-o-y compared with 353,280 LDT in January-April 2025. The number of vessels imported for recycling also declined by 31% y-o-y to 25 units from 36 units a year earlier.

Market participants noted that mills continued to procure cautiously amid pressure on finished steel demand and margins. However, steady infrastructure activity and expectations of gradual improvement in construction demand supported selective bulk scrap buying during the latter part of the quarter.

Outlook

Bangladesh’s ferrous scrap imports are expected to remain stable m-o-m at around 0.3 mnt next month, supported by continued bulk buying interest and preference for Asian-origin cargoes. Japanese and Singapore-origin scrap is likely to remain competitive, while US-origin bulk cargoes may continue facing pressure from higher freight costs and weaker buying appetite.

However, import activity may remain sensitive to LC restrictions, dollar liquidity conditions, export-sector performance, and domestic steel demand trends. Mills are expected to continue cautious procurement strategies while closely monitoring global scrap prices, trade financing conditions, and macroeconomic developments.

Leave a Reply