Rising raw material costs, lack of electricity and gas in the facilities, coupled with other factors all posed a threat to Bangladesh’s steel industry’s ability to survive. Mills continued to be under pressure as a result of rising production costs and a shortage of finished steel demand from domestic end-users during the past week’s trade session.

Owing to limited demand and uncertainties in the market, local sellers lowered finished steel prices to make their pending payments to banks and clear their electricity bills.

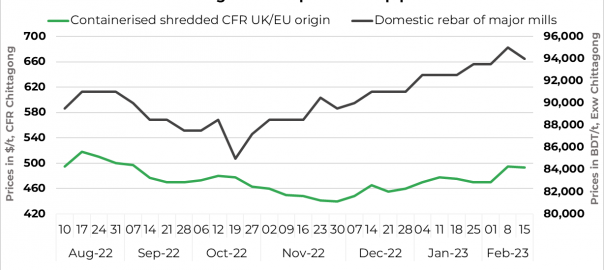

SteelMint assessed domestic rebar prices at BDT 94,000/t ($885/t) exw-Chittagong, down by BDT 1,000/t. Following it, mills in Dhaka decreased their rebar offers by BDT 2,000/t w-o-w. Fresh offers are now at BDT 88,000-90,000/t ($828-847/t).

Steel industry seeks government support: Major steel producers in Bangladesh have urgently requested government’s assistance in order to address the situation that the industry is currently facing.

Local ship-breaking scrap prices in the nation dropped by BDT 2,000-3,000/t w-o-w to BDT 65,000-70,000/t ($611-658/t) ex-yard Chittagong.

Imported scrap prices falling post-Turkish tremor, ease in LCs

Although the market for ferrous scrap in Bangladesh is quiet, LC openings are getting a little more accessible, which helps the major mills meet some urgent demands. After the abrupt calamity in the Turkish region, prices for ferrous scrap are generally moving downward.

Bulk scrap suppliers are moving towards South East Asian countries as demand from Vietnam for ferrous scrap of US origin increased.

- Fresh offers for US-origin bulk HMS are heard at $460/t CFR Chittagong , stable w-o-w.

- Containerised offers for UK-origin shredded scrap are at 490-95/t CFR, downwards with $2/t w-o-w.

“Bangladeshi buyers are not preferring materials from UK or Europe on quality concern issues. Meanwhile, they are procuring from other destinations like Singapore and Hongkong,” a buyer from Bangladesh stated.

Outlook

Due to the current volatilities in the steel industry, participants expected uncertainties in domestic and imported markets. As a result, nominal price corrections are likely in the near-term.

Leave a Reply