- Scrap surge led by US and Japan

- Eid lull ends with sharp import rebound

Bangladesh’s total ferrous scrap imports, including bulk and containerised cargoes, rose sharply to 0.63 million tonnes (mnt) in May 2025, a 50% increase from 0.42 mnt in April.

Bulk scrap volumes alone surged to 389,143 tonnes (t), reflecting a 55% m-o-m rise from 250,290 t in April and an 85% y-o-y jump from 210,010 t in May 2024, signalling a strong rebound in demand over both the short and long terms.

The rise in imported scrap was driven by mills resuming active bookings post-Eid, supported by a sharp increase in bulk arrivals from key suppliers.

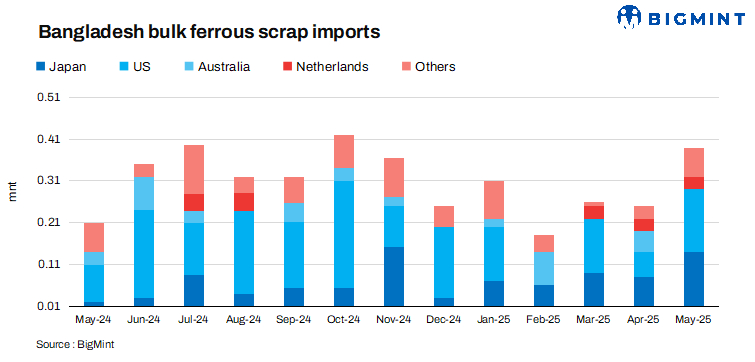

Country-wise exports

Shipments from the US more than doubled, while Japan saw an over sixfold growth y-o-y, reflecting a rebound in procurement activity and opportunistic buying amid stable global prices.

United States: Exports to Bangladesh more than doubled month-on-month in May to 153,201 t in May from 61,986 t in April. This also marked a 66% y-o-y increase from 92,524 t in May 2024.

Japan: Shipments jumped 78% m-o-m to 140,290 t in May from 78,900 t in April, and over six times higher y-o-y from 22,046 t a year ago.

Singapore: Volumes rose sharply to 56,415 t in May from 18,914 t in April, though there were no imports from Singapore in May 2024.

Australia: Export volume remains nill in May compare to 52,833 t in April and 26,887 t in May last year.

Factor driving scrap imports

Post-Eid restocking: Scrap market remained slow in April amid the Eid holidays, with mills operating at low capacity utilisation amid reduced steel consumption from end-users, A Chattogram-based trader noted that the market remains closed until 5 April.

Bulk price movements

- Bulk HMS 80:20 scrap offers from US eased slightly to $373/t CFR in May from $375/t in April.

- Japan’s H2 scrap offers edged down to $360/t CFR in May, from $364/t in April.

Currency update: Currency depreciation added pressure, with the BDT weakening 1% m-o-m to average BDT 122.2/USD in May, compared to 121.5/USD in April.

Outlook

Sluggish construction activity is likely to continue weighing on demand. With fewer mills in operation, a significant recovery appears unlikely given the dull buying appetite from regional players.

Leave a Reply