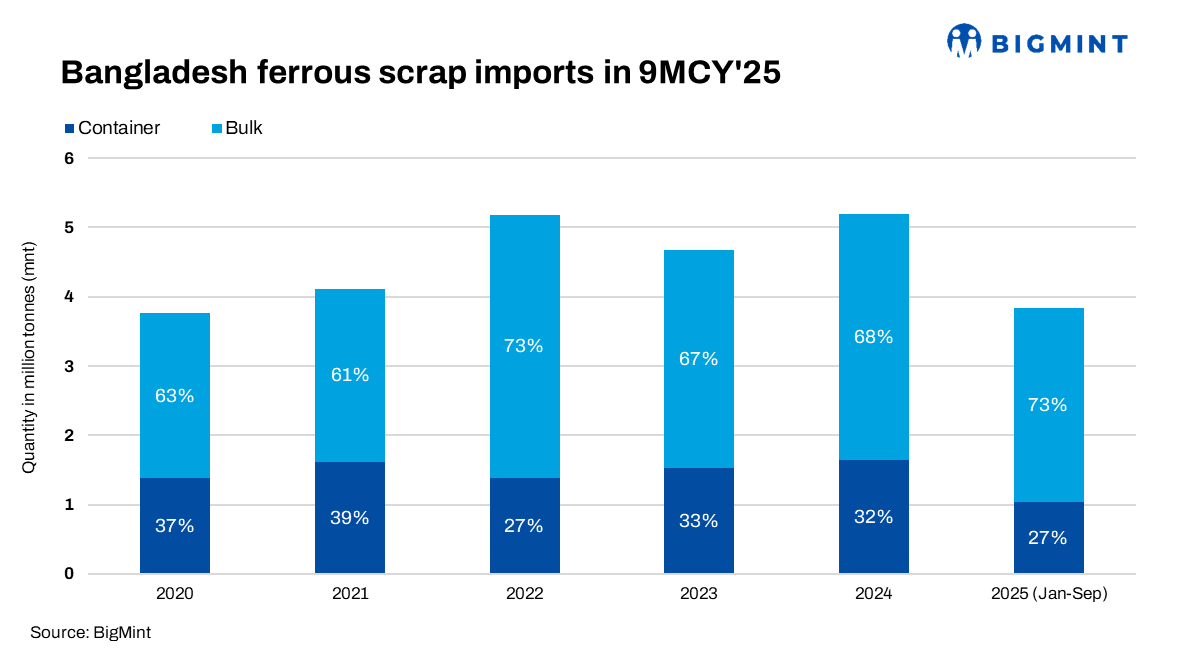

- Total scrap imports in Jan-Sep’25 reaches 3.84 mnt

- Shipments from Japan rise 203% to 0.97 mnt in 9MCY’25

Bangladesh’s total ferrous scrap imports, including bulk and containerised cargoes, reached 3.84 million tonnes (mnt) during 9MCY’25 (January-September 2025). Meanwhile, Bulk scrap imports rose 12% y-o-y to 2.81 mnt from 2.51 mnt in 9MCY’24, driven by active post-Eid bookings in June and increased arrivals from key suppliers such as Japan and the US.

However, on a monthly basis, bulk imports slipped 67% to 0.16 mnt in September from 0.49 mnt in August as monsoon disruptions dampened construction activity and end-user demand.

Factors driving scrap imports

Import volumes rose sharply mid-year as mills resumed bookings after Eid, supported by improved bulk arrivals and competitive international offers.

Japan emerged as a stronger source of supply, while attractive US-origin offers prompted mills to secure cargoes in anticipation of price increases.

However, persistent heavy rains and sluggish construction demand limited fresh deals, with most mills adopting a cautious approach. Some opted to build inventories ahead of a potential post-monsoon recovery, relying on credit-based purchases to manage liquidity constraints.

Price trends

Average bulk and containerised scrap offers fell year-on-year across origins:

- US-origin bulk HMS 80:20 declined by $42/t to $364/t CFR (from $406/t).

- Japan H2 scrap dropped by $49/t to $353/t CFR (from $402/t).

- European-origin HMS 80:20 decreased by $42/t to $362/t CFR (from $404/t).

- European-origin shredded fell by $42/t to $380/t CFR (from $422/t).

Currency appreciates slightly: The Bangladeshi taka weakened slightly, averaging 122/USD in 9MCY’25 compared to 114/USD in 9MCY’24.

Country-wise bulk scrap exports

The US and Japan remained the top exporters to Bangladesh, supplying the majority of bulk scrap volumes.

- Japan: Shipments from Japan climbed exponentially by 203% to 0.97 mnt in 9MCY’25 while more than doubling compared to 0.32 mnt in 9MCY’24, but decline 33% m-o-m to 0.08 mnt in Sep’25 from 0.12 mnt in Aug’25.

- US: Imports from the US decline by 13% to 1.2 mnt in 9MCY’25, from 1.05 mnt t in 9MCY’24 and also decline by 89% m-o-m to 0.03 mnt in Sep’25 from 0.27 mnt in Aug’25.

- New Zealand: Imports from New Zealand rose by 13% to 0.18 mnt in 9MCY’25, compared with 0.16 mnt in 9MCY’24. However, there were no imports recorded in Sep’25.

- Australia: Imports from Australia decline by 38% to 0.23 mnt in 9MCY’25 from 0.37 mnt in 9MCY’24. However, there were no imports recorded in Sep’25.

Ship-breaking

Ship recycling activity remained sluggish, with total demolition tonnage down marginally by 0.15% y-o-y to 680,323 LDT in 9MCY’25 from 681,342 LDT in 9MCY’24. However, the number of vessels dismantled dropped sharply by 41% to 68 units from 115 a year earlier, reflecting limited availability of workable tonnage and weak steel fundamentals.

Outlook

The market is expected to stay cautious, with mills restricting new bookings due to liquidity constraints, currency volatility, and subdued steel demand. Post-monsoon construction recovery and potential policy clarity may lend mild support, though a sharp rebound in scrap prices appears unlikely. Imports are likely to remain steady as mills cautiously replenish inventories, supported by competitive global offers, while the ship recycling sector continues to face pressure from low tonnage supply and weak finished steel margins.

Leave a Reply